AMINA Bank AG

AMINA Bank AG  AMINA UK

AMINA UK  AMINA Hong Kong

AMINA Hong Kong  AMINA EU

AMINA EU By Werner Broennimann, Investment Manager, and Sonali Gupta, Research Lead, AMINA Bank

The US strikes on three Iranian nuclear sites over the weekend, the Iranian retaliation on Monday, the announcement of a ceasefire by US President Donald Trump, and the subsequent attack on Tehran by Israel raise the question of how the crypto markets react in general to such geopolitical events.

For investors who are not just buying and holding crypto for the long term on an unleveraged basis, getting a better grasp of the return drivers in these markets is essential.

In the popular narrative, BTC has sometimes been designated “digital gold” and is seen as a currency debasement hedge. At other times, it is described as a risky asset, much like the S&P 500 or even the Magnificent-7 tech stocks. The narrative around return drivers for ETH and other altcoins has been limited to risky assets for the most part. Let’s dive a bit deeper into this topic.

Comparative Scale of Crypto, Gold, and S&P 500 Markets

The global cryptocurrency market today stands at approximately $3.4 trillion, making it a fraction of the size of traditional asset classes. For context, the gold market is valued at around $20.8 trillion as of March 2025, while the S&P 500’s aggregate market capitalization soared to $54.5 trillion in January 2025. This stark difference underlines that, while crypto has grown rapidly, it remains a much smaller asset class compared to gold and major equity indices.

Impact of Geopolitical Events on Crypto vs. Traditional Markets

Geopolitical issues, such as wars or sanctions, typically impact traditional markets—like equities and commodities—first and most directly. In the long run, cryptocurrencies, by contrast, are generally affected predominantly when these events intersect with the digital asset ecosystem, such as the use of crypto to bypass traditional financial channels or facilitate cross-border donations.

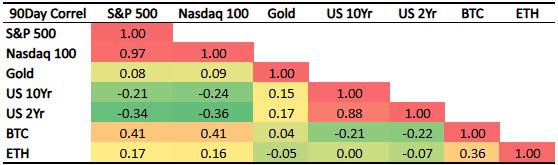

Source: AMINA BANK

For example, during the onset of the Russia-Ukraine conflict in February 2022, both global stock exchanges and crypto markets initially dropped. However, as sanctions tightened and traditional financial channels were restricted, there was a surge in crypto trading volumes—particularly in BTC/RUB and BTC/UAH pairs—as individuals sought alternatives to move and store value. Reportedly, over $136 million in crypto donations were sent to Ukraine, primarily in Bitcoin and Ethereum, with donations peaking shortly after the conflict began. This resulted in an instant 25% uptick across major cryptocurrencies. This episode demonstrates that crypto can experience short-term, event-driven rallies when it becomes a tool for financial circumvention or humanitarian aid.

Correlation with Equities and Commodities

Despite its unique characteristics, cryptocurrency as an asset class has shown a moderate correlation (typically 20–40%) with equities. This is likely because many investors treat cryptocurrencies similarly to tech stocks, responding to broader market trends and risk sentiments and a necessity to close leveraged long positions in times of market turmoil. Consequently, we have seen sharp, although short lived corrections in the prices of BTC and ETH on Trump’s tariff Liberation Day on April 2 and last weekend. In contrast, crypto’s correlation with commodities like gold remains weaker, reflecting their differing roles in portfolios—gold as a traditional safe haven, and crypto as a speculative or growth asset.

Crypto-Specific Market Drivers

Unlike traditional assets, cryptocurrencies are heavily influenced by sector-specific events, which can have outsized impacts on prices and sentiment. Key drivers include:

- Bitcoin Halving: Occurring roughly every four years, this event reduces the rate at which new bitcoins are created, often leading to increased scarcity and, historically, price appreciation if demand holds steady.

- ETF Launches: Approval of spot Bitcoin or Ethereum ETFs did bring new institutional capital and legitimacy to the market.

- Major Network Upgrades: Upgrades like Ethereum’s Merge (transition to proof-of-stake) or the recently implemented Pectra upgrade did affect both utility and investor confidence.

- DeFi and Stablecoin Growth: The expansion of decentralized finance and stablecoins has also opened new use cases and liquidity channels for cryptocurrencies.

- Regulatory Developments: Changes in regulation, whether positive (clarity, acceptance) or negative (restrictions, bans), also drive significant volatility.

Ceasefire

Besides the understanding of crypto currencies as a growth asset, the other big question for investors is whether the hostilities between Iran on the one side and Israel and the US on the other side are truly over.

On a more fundamental level, one has to ask: Did the bombing raid achieve the claimed goals and has it “obliterated” the targeted sites as Trump claimed? Are Israel or the US in a position to assess this already? Should the assessment about Iran’s nuclear programme change, would this trigger another attack by the US, and would this be the end of it?

Despite an additional bombing raid by Israel on Tehran after Trump’s announcement, it seems that the ceasefire is holding for now. So, a lasting end to the hostilities may still be in the cards.

Exposure Management

“Buying the dip” whenever the Trump administration shook up the markets with policy announcements or in this case military action, it has worked well for investors. However, high profile leaders in finance warn of an “extraordinary amount of complacency” in the markets. Even if the Trump administration is looking to limit the negative market impacts of their actions, it may not always be in their hands to fix things. The latest Israeli air raid being a case in point.

Historically, cryptocurrencies, such as BTC, have been subjected to long-term and significant drawdowns when the market turns. It may make sense to keep that in mind when increasing one’s investment exposure during corrections.

Summary

In summary, the cryptocurrency market is still dwarfed by gold and equities, and while it occasionally reacts to global geopolitical events—especially when cryptocurrencies are preferred over traditional financial channels – it remains primarily driven by sector-specific developments. Its moderate correlation with equities suggests that, for now, crypto is treated more like a risk asset than a true safe haven, with its unique market cycles and innovation-driven catalysts shaping its trajectory.

—————————————————————————————————————–

Disclaimer – Research

This document has been prepared by AMINA Bank AG (“AMINA”) in Switzerland. AMINA is a Swiss bank and securities dealer with its head office and legal domicile in Switzerland. It is authorized and regulated by the Swiss Financial Market Supervisory Authority (FINMA).

This document is published solely for educational purposes; it is not an advertisement nor is it a solicitation or an offer to buy or sell any financial investment or to participate in any particular investment strategy. This document is for distribution only under such circumstances as may be permitted by applicable law. It is not directed to, or intended for distribution to or use by, any person or entity who is a citizen or resident of or located in any locality, state, country or other jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation or would subject AMINA to any registration or licensing requirement within such jurisdiction.

No representation or warranty, either express or implied, is provided in relation to the accuracy, completeness or reliability of the information contained in this document, except with respect to information concerning AMINA. The information is not intended to be a complete statement or summary of the financial investments, markets or developments referred to in the document. AMINA does not undertake to update or keep current the information. Any statements contained in this document attributed to a third party represent AMINA’s interpretation of the data, information and/or opinions provided by that third party either publicly or through a subscription service, and such use and interpretation have not been reviewed by the third party.

Any prices stated in this document are for information purposes only and do not represent valuations for individual investments. There is no representation that any transaction can or could have been effected at those prices, and any price(s) do not necessarily reflect AMINA’s internal books and records or theoretical model-based valuations and may be based on certain assumptions. Different assumptions by AMINA or any other source may yield substantially different results.

Nothing in this document constitutes a representation that any investment strategy or investment is suitable or appropriate to an investor’s individual circumstances or otherwise constitutes a personal recommendation. Investments involve risks, and investors should exercise prudence and their own judgment in making their investment decisions. Financial investments described in the document may not be eligible for sale in all jurisdictions or to certain categories of investors. Certain services and products are subject to legal restrictions and cannot be offered on an unrestricted basis to certain investors. Recipients are therefore asked to consult the restrictions relating to investments, products or services for further information. Furthermore, recipients may consult their legal/tax advisors should they require any clarifications.

At any time, investment decisions (including whether to buy, sell or hold investments) made by AMINA and its employees may differ from or be contrary to the opinions expressed in AMINA research publications.

This document may not be reproduced, or copies circulated without prior authority of AMINA. Unless otherwise agreed in writing AMINA expressly prohibits the distribution and transfer of this document to third parties for any reason. AMINA accepts no liability whatsoever for any claims or lawsuits from any third parties arising from the use or distribution of this document.

Research will initiate, update and cease coverage solely at the discretion of AMINA. The information contained in this document is based on numerous assumptions. Different assumptions could result in materially different results. AMINA may use research input provided by analysts employed by its affiliate B&B Analytics Private Limited, Mumbai. The analyst(s) responsible for the preparation of this document may interact with trading desk personnel, sales personnel and other parties for the purpose of gathering, applying and interpreting market information. The compensation of the analyst who prepared this document is determined exclusively by AMINA.