AMINA Bank AG

AMINA Bank AG  AMINA UK

AMINA UK  AMINA Hong Kong

AMINA Hong Kong  AMINA EU

AMINA EU The Bitcoin price transition from $126,000 to $92,000 was abrupt and rewired investor behaviour, liquidity flows, and infrastructure stress. More than $1.11 billion in leveraged positions were unwound within a single week. Exchange reserves swung violently as 65,000 BTC flooded back onto exchanges. Long-term holders who have weathered years of crypto turbulence exited 815,000 BTC during the downturn. Through the turbulence, a clear pattern emerged: investors migrated rapidly from diversified, growth positioning to defense and concentrated safety.

Market cycles in crypto do far more than move prices. They alter behaviour, reshape liquidity, and redefine how different investor cohorts position themselves across exchanges, crypto protocols and custodial systems. Understanding these shifts provides clarity on how capital migrates, how leverage builds or unwinds, and how infrastructure is tested when sentiment turns sharply. This analysis draws on onchain flows, derivatives positioning, institutional allocations, and liquidity dynamics observed through 2024 and 2025, including operational lessons learned when volatility exposes the differences between platforms built for continuous availability and platforms that falter under pressure.

Bull Markets

In the first-half of 2025, the expansion pattern was unmistakable. Trading volumes totalled $9.36 trillion in 2025, compared with $8.7 trillion in H1 2024, $4.15 trillion in H1 2023 and $7.8 trillion in H1 2022. The scale of activity made H1 2025 the most liquid first half since the 2021 bull run. January 2025 alone processed $2.32 trillion, more than double the $1.1 trillion recorded in January 2024. This was a clear indication that capital was flowing into the system. Institutional allocations moved in line with rising confidence. According to a survey by Coinbase Institutional and EY-Parthenon, more than 75% of institutions planned to increase their digital asset exposure and close to 60% expected to allocate over 5% of their assets under management to crypto-related products. Regulated spot Bitcoin ETFs attracted nearly $15 billion in net inflows during the first half of 2025, pushing exchange reserves to their lowest level in five years as substantial volumes moved into longer-term custodial structures.

Onchain data showed a coordinated accumulation across investor groups. Large holders increased their balances, while smaller wallets grew at their fastest pace since late 2024. This alignment across cohorts is rare and typically occurs only during strong expansions. At the same time, behavioural shifts emerged around local peaks. On 6 October 2025, when Bitcoin reached $126,000, more than 63,000 BTC moved from long-term holders to short-

term holders. Historically, such patterns appear around market tops, where experienced holders choose to distribute into rising demand. Sentiment indicators confirmed the mood. The Crypto Fear and Greed Index stayed above 70 from early February through late March 2025, reflecting a prolonged period of elevated optimism and persistent risk appetite.

Rising prices encouraged investors to treat every dip as an opportunity. Portfolio construction became more active. Rebalancing across diversified crypto baskets often outperformed simple holding. Daily rebalancing models in particular generated stronger gains during steep upward moves.

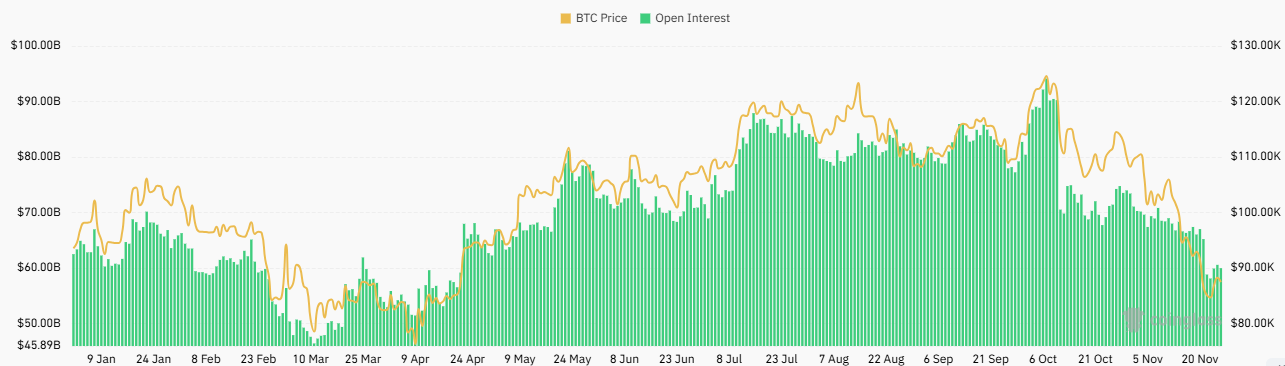

Leverage expanded accordingly. Borrowing on decentralised lending protocols increased by almost one thousand percent from the 2022 low to the end of 2024. Much of this borrowing was speculative, aimed at amplifying directional exposure. Futures open interest regularly exceeded $45 billion. Market makers remained highly active, spreads narrowed and liquidity conditions strengthened across venues.

Figure 1: Year to Date Exchange BTC Futures Open Interest

Source: Coinglass (25th November 2025)

Bear Markets

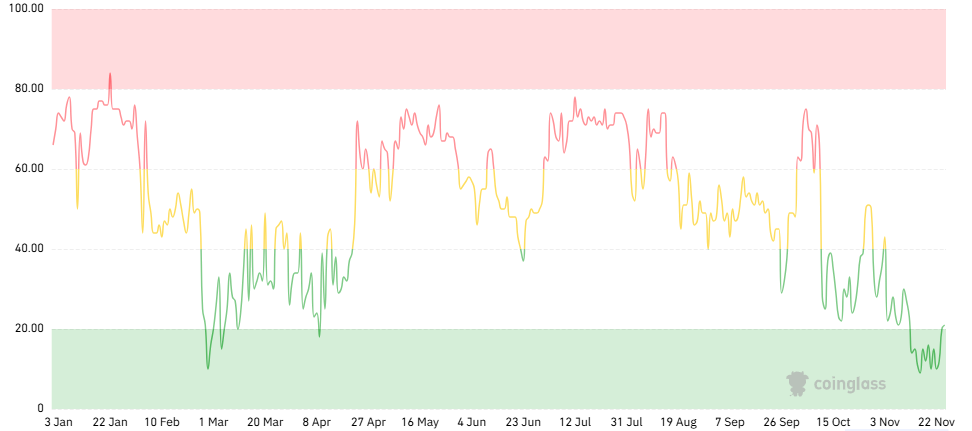

When momentum breaks, fear replaces optimism and the focus shifts from seeking upside to protecting capital. Between mid-October and mid-November 2025, Bitcoin declined from $126,000 to below $92,000. The Fear and Greed Index collapsed to 10 in a matter of weeks.

Figure 2: Year to Date Crypto Fear & Greed Index (as of 25th November 2025)

Source: Coinglass

Liquidations intensified. More than $1.11 billion in leveraged positions unwound within a single week, with a twenty-four hour period in mid-November seeing $700 million in forced liquidations affecting nearly 150,000 traders. These cascades are typical during deleveraging phases, as margin calls trigger automated selling and further price deterioration.

Altcoins absorbed disproportionate damage. Ethereum fell by more than 20%, Solana declined sharply and many high-beta assets experienced declines exceeding the broader market. Automated liquidation engines unwound more than $19 billion in leveraged positions during the October correction. Liquidity thinned across venues as market makers withdrew to protect capital, widening execution gaps and distorting price discovery.

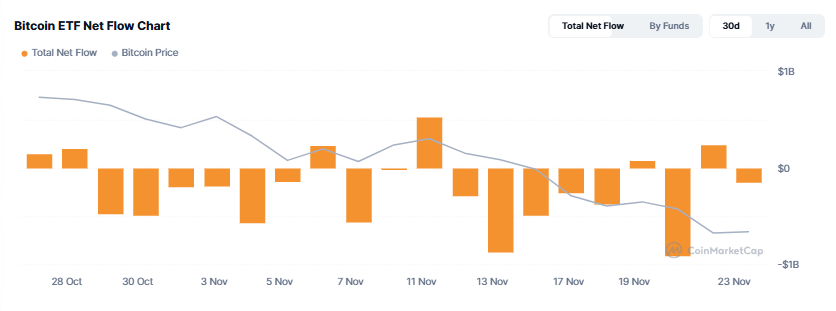

Exchange flows reversed direction. Rather than moving coins off exchanges into long-term custody, investors moved assets back onto exchanges in preparation for selling. More than 65,000 BTC flowed into exchanges during this period. Long-term holders, typically resilient through volatility, began distributing as well. Approximately 815,000 BTC held for more than a year were sold during the downturn. One long-term holder who had held coins since 2011 exited more than $1.3 billion in positions on a single day. Spot ETFs recorded more than $622 million in net outflows over the last three weeks in November 2025.

Figure 3: Bitcoin ETF Net Flow Chart

Source: CoinMarketCap (28th October 2025 to 24th November 2025)

Retail behaviour became reactionary. Herding intensified as fear spread quickly across social channels, with negative sentiment reinforcing further selling. Short-term holders capitulated earlier and at greater losses, attempting to avoid deeper drawdowns. Long-term holders displayed loss aversion, often delaying exits despite mounting pressure. Price discovery fragmented as exchanges faced latency issues, pricing feeds diverged and liquidity became uneven across venues. Certain synthetic assets and stablecoins temporarily deviated from their pegs before stabilising. For example, Ethena’s USDe USD-pegged stablecoin depegged to 65 cents before going back to its $1 peg.

Infrastructure came under severe pressure. Trading engines, APIs, oracle networks and settlement rails faced their most demanding moments when volatility peaked. Some platforms experienced delays or piricing dislocations. AMINA maintained 100% uptime across trading and custody operations throughout the cascade throughout October and November, providing clients with continuous access to execution and settlement at the moments when reliability mattered most.

Where Investors Move in Each Cycle

Investor movement shifts dramatically between market conditions. In bull phases, capital spreads outward across the entire crypto ecosystem. Investors seek liquidity, higher transaction velocity and new sources of return, operating across exchanges, decentralised protocols, OTC venues and structured product desks. Leverage rises, yield opportunities attract inflows and portfolios broaden into larger baskets of assets. Self-custody grows alongside these trends as long-term positions are set aside while traders operate with more flexible capital.

During these expansion phases, structured products become particularly valuable for investors seeking participation without full directional exposure. Capital-protected notes, yield-enhancing overlays and hedging structures such as put spreads or risk reversals create a more controlled return profile in markets where outright positions carry considerable variance. The same instruments can be configured to enhance participation through call spreads, leveraged reversals or combinations that trade limited premium for convexity during acceleration phases. These instruments only function as intended when they are designed, priced and executed within a controlled environment. This is why sophisticated investors increasingly turn to regulated managers and teams for implementation.

In bear phases, the pattern reverses. Investors move inward toward stability. They consolidate capital into assets they trust, particularly Bitcoin and fully collateralised stablecoins. Trading activity narrows to the most liquid markets. Many participants step back from active trading altogether, choosing to wait for calmer conditions rather than risk further losses. Exchange inflows increase as investors prepare to reduce exposure. Onchain metrics focused on capitulation, such as long-term holder selling and realised loss levels, become reference points for those monitoring market structure. The emphasis shifts from expansion to defence.

During acute stress events like the 10 October 2025 liquidation cascade, the migration becomes even more pronounced. Investors concentrate their activity on platforms capable of operating normally despite volatility. Systems designed for continuous uptime see heavier use, not because investors are adding risk, but because these platforms remain functional when others struggle. Price gaps between venues, delayed settlement times and inconsistent oracle data make reliability the critical factor. The decision is no longer about finding opportunity, but ensuring that existing positions can be adjusted or closed without disruption.

Cohort behaviour also diverges during these cycles. Short-term holders typically exit first, often at losses. Long-term holders initially remain firm, but once losses deepen sufficiently, their onchain movements become visible as coins move from cold storage to exchanges. This shift often marks the late stages of capitulation. Once selling pressure exhausts, investors gradually begin reallocating from defensive positions to cautiously opportunistic ones, typically beginning with Bitcoin and other highly liquid assets before considering higher risk alternatives.

Across both cycles, the direction of movement is unmistakable. Bull markets push investors outward, bear markets draw them inward. The rhythm of these migrations defines

the structure of each phase and leaves clear fingerprints across onchain datasets, liquidity curves and exchange order flow.

Infrastructure and Risk Management

Regardless of market direction, uninterrupted market access remains the constant requirement. During bull markets, infrastructure must absorb higher trading volumes, deeper liquidity routing and a surge in settlement traffic. During bear markets, it must withstand fragmentation, latency spikes and elevated redemption flows.

Systems with redundant connectivity across exchanges, OTC desks and settlement partners typically demonstrate stronger stability when conditions deteriorate. During the October cascade, AMINA’s architecture — built for continuous operation across volatile market conditions — allowed the platform to maintain access when other venues experience disruption becomes one of the clearest differentiators during stress. Access to proper risk management, validated pricing models and secure settlement is the difference between capturing an opportunity and being structurally prevented from doing acting until windows have closed.

Market dislocations often open windows where volatility is mispriced and directional structures become unusually attractive. Investors without regulated counterparts, or without access to OTC execution desks, are often unable to act until the opportunity has already passed. Through both bull and bear cycles, infrastructure that prioritises continuity, accurate settlement and professional risk engineering supports clients most effectively. It performs predictably in periods of strength and remains accessible during periods of pressure.

Conclusion

Bull markets draw capital into the system, deepen liquidity and encourage leverage. Bear markets unravel leverage, expose structural weaknesses and concentrate liquidity in assets perceived as safest. Retail behaviour amplifies peaks, institutional flows often define the floor, and exchange flows remain one of the clearest indicators of regime shifts.

Across market conditions, resilience and continuity in trading and custody infrastructure anchor the investor experience. Crypto operates continuously with no pause in price formation, and systems must be engineered to mirror that continuity.

Disclaimer – Research and Educational Content

This document has been prepared by AMINA Bank AG (“AMINA”) in Switzerland. AMINA is a Swiss licensed bank and securities dealer with its head office and legal domicile in Switzerland. It is authorized and regulated by the Swiss Financial Market Supervisory Authority (“FINMA”).

This document is published solely for educational purposes; it is not an advertisement nor a solicitation or an offer to buy or sell any financial investment or to participate in any particular investment strategy. This document is for publication only on AMINA website, blog, and AMINA social media accounts as permitted by applicable law. It is not directed to, or intended for distribution to or use by, any person or entity who is a citizen or resident of or located in any locality, state, country or other jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation or would subject AMINA to any registration or licensing requirement within such jurisdiction.

Research will initiate, update and cease coverage solely at the discretion of AMINA. This document is based on various sources, incl. AMINA ones, and was generated using artificial intelligence (“AI”). No representation or warranty, either express or implied, is provided in relation to the accuracy, completeness or reliability of the information contained in this document, except with respect to information concerning AMINA. The information is not intended to be a complete statement or summary of the subjects alluded to in the document, whereas general information, financial investments, markets or developments. AMINA does not undertake to update or keep current information. Any statements contained in this document attributed to a third party represent AMINA’s interpretation of the data, information and/or opinions provided by that third party either publicly or through a subscription service, and such use and interpretation have not been reviewed by the third party.

Any formulas, equations, or prices stated in this document are for informational or explanatory purposes only and do not represent valuations for individual investments. There is no representation that any transaction can or could have been affected at those formulas, equations, or prices, and any formula(s), equation(s), or price(s) do not necessarily reflect AMINA’s internal books and records or theoretical model-based valuations and may be based on certain assumptions. Different assumptions by AMINA or any other source may yield substantially different results.

Nothing in this document constitutes a representation that any investment strategy or investment is suitable or appropriate to an investor’s individual circumstances or otherwise constitutes a personal recommendation. Investments involve risks, and investors should exercise prudence and their own judgment in making their investment decisions. Financial investments described in the document may not be eligible for sale in all jurisdictions or to certain categories of investors. Certain services and products are subject to legal restrictions and cannot be offered on an

unrestricted basis to certain investors. Recipients are therefore asked to consult the restrictions relating to investments, products or services for further information. Furthermore, recipients may consult their legal/tax advisors should they require any clarifications.

At any time, investment decisions (including, among others, deposit, buy, sell or hold investments) made by AMINA and its employees may differ from or be contrary to the opinions expressed in AMINA research publications.

This document may not be reproduced, or copies circulated without prior authority of AMINA. Unless otherwise agreed in writing, AMINA expressly prohibits the distribution and transfer of this document to third parties for any reason. AMINA accepts no liability whatsoever for any claims or lawsuits from any third parties arising from the use or distribution of this document.

©AMINA, Kolinplatz 15, 6300 Zug