AMINA Bank AG

AMINA Bank AG  AMINA UK

AMINA UK  AMINA Hong Kong

AMINA Hong Kong  AMINA EU

AMINA EU Executive Summary

- The overall crypto market capitalisation declined by approx. 20% last month, given the uncertainties caused by rising inflation, rate hikes, geopolitics, and Covid-19 restrictions. While good fundamentals continue to contribute to growth, the short-term outlook remains cautious, preferring blue-chip assets (BTC, ETH) over others.

- Bitcoin continues to be adopted as a mean of payment; The Central African Republic (CAR) became the second country to adopt bitcoin as legal tender. Goldman Sachs issued its first bitcoin-backed loan last week, paving the way for others. Bitcoin on-chain analytics consistently show an increase in volumes of perpetual vs. calendar future contracts, indicating a move away from short-term speculation and towards HODLer accumulation.

- The highly anticipated Ethereum network upgrade, ‘The Merge,’ has been delayed several months. Layer 2 scaling solution Optimism announced their token airdrop for early supporters, which contributed to building a growing ecosystem of decentralised applications (DApps). Yuga Labs conducted one of the biggest NFT mints on Ethereum. Higher than expected demand tested the network limits, resulting in insanely high gas fees (more than USD 10,000).

- Alternative platform blockchain assets among the AMINA offerings corrected more than BTC and ETH but showed a strong correlation, resulting in 30-day low volatility numbers. The decrease in NFT trading volume results in less on-chain activity for leading NFT blockchains (Ethereum, Solana, Flow), reducing active addresses and transaction count.

- The new user growth for the Decentralised Finance (DeFi) ecosystem projects is stagnating, potentially because of a steep learning curve and lack of innovation to retain users. The TVL for the entire DeFi ecosystem has been almost flat for the last few months. Users continue to move toward NFT and Metaverse projects similar to 2021.

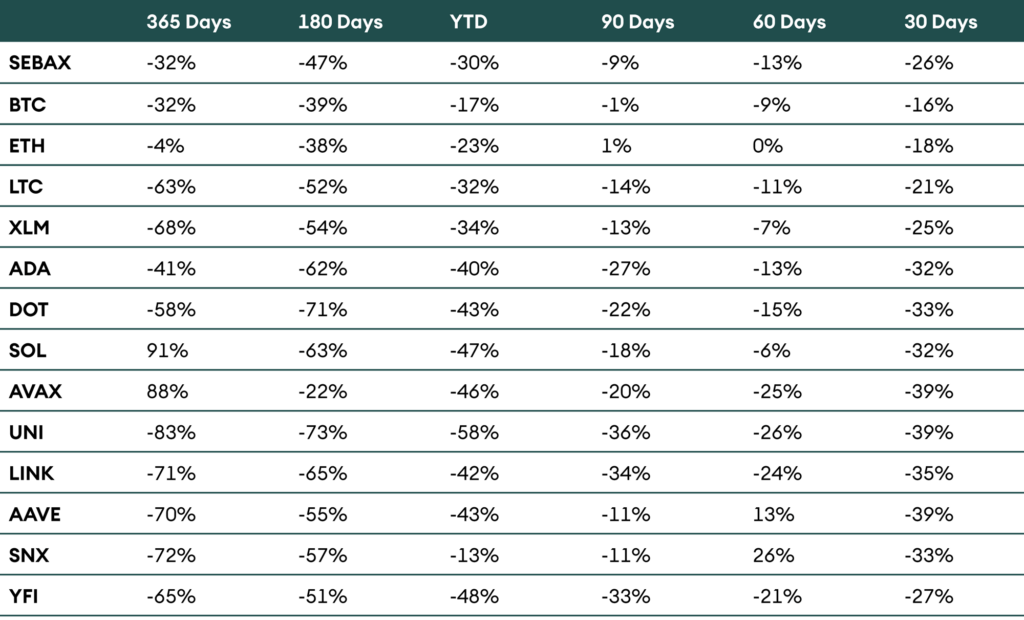

Table 1: Performance of AMINAX® and AMINA coin universe assets as of 01 May 2022

Outlook

Last month, there was no place to hide in both the traditional and the digital financial market! In the digital space, cryptocurrencies were hit badly. According to the AMINAX® Index, which consists of a selection of blue-chip coins, the market dropped by 26%. The two most famous currencies fell less than the market. Bitcoin and ether fell by 16% and 18%, respectively.

In traditional markets, asset prices fell across the board. Over the same period, The S&P 500 index fell by more than 9%, and the benchmark 10-year US Treasury yield increased by 50 basis points to almost 3%. The combined fall in US equity and government bond prices is unusual.

In our previous edition of the Digital Investor (Strong Fundamentals Enabling Growth), we drew a macroeconomic scenario in which inflation, rate hike, and geopolitics will dominate in the short term, and that is indeed what happened. We also noted that sentiment mainly drove digital assets despite strong fundamentals. This is why risky investments and cryptocurrencies moved broadly hand in hand in the past months.

We keep a cautious stance going forward. The war is not over, and there are no signs of an end in the near future. Even when corrected from volatile components such as food and energy, inflation continues to increase. With the Fed as its head, Central banks are setting the tone with aggressive rate hikes.

While growth expectations and earnings have remained broadly robust, we now expect a series of downward revisions. This movement is accentuated by the Chinese slowdown fuelled by strict COVID-19 restrictions.

Based on the scenario presented above, we expect traditional and digital asset prices to remain under pressure in the coming months and are cautious in our allocation. We have increased our cash allocation, kept our duration low, and reduced exposure to risky assets.

As far as cryptocurrencies are concerned, we have also reduced our exposure. As sentiment should remain poor, we expect the digital space to remain under pressure. Notice that we continue to prefer bitcoin and ether relative to altcoins and DeFi tokens. It is often said that real innovation happens during the bear market cycles. Money continues to flow into many crypto projects to build the next generation of the internet. Even though prices are down for the month, funding news, coupled with large financial institutions offering BTC-backed loans and several publicly traded companies holding bitcoin on their balance sheets, contribute to strengthening the confidence in the fundamentals of the technology.

In the following sections, we will look at bitcoin key fundamentals and explore the NFT and DeFi ecosystems of the leading blockchains. The new user growth for DeFi projects on Ethereum has slowed down as the DeFi space is saturated with near-identical projects, with key differentiators mostly being higher APYs. In the NFT space, there was also a slowdown in trading volume and market cap in the last month.

Bitcoin

Bitcoin price has fallen from USD 46,000 to USD 38,000 during the month. Much of the altcoins followed, some with more considerable losses, attributed to the global uncertainty and strong correlation with the high growth tech equities. However, key fundamental parameters for BTC continue to get stronger, creating strong support for the price.

At the start of the month, Miami hosted Bitcoin 2022 conference, attended by 30,000+ people worldwide with several notable speakers. One of the most important announcements from that event was the USD 70 million fundraise by the Lightning Labs (entity developing the Lightning Network) and the development of a new protocol called Taro to enable asset issuing on bitcoin. Merchants and payment service providers increasingly use the Lightning Network for fast and cheap Bitcoin transactions.

After El Salvador made bitcoin a legal tender in 2021, The Central African Republic (CAR) became the second country to adopt bitcoin as legal tender in April 2022. Citizens can now use it to do regular commerce and pay taxes. In another good news around regulations, Panama has approved a bill regulating the use of bitcoin and other crypto assets, hoping to convert Panama into a technology hub in Latin America.

Financial services giant, Goldman Sachs, issued its first bitcoin-backed loan last week. The move is expected to be adopted by other entities, generating more adoption. On 27 April, Australia’s first bitcoin spot exchange-traded fund (ETF) was expected to launch. But, the listing was halted for multiple reasons, one of them being a delay in standard checks and balances.

From the on-chain analysis of the bitcoin network, we see the dominance for perpetual futures contracts increasing and calendar futures volume decreasing, indicating a move away from short-term speculation. Further, low exchange transfer volume (32% of total transacted volume) also shifts towards fundamental demand drivers, such as OTC transactions and HODLer accumulation.

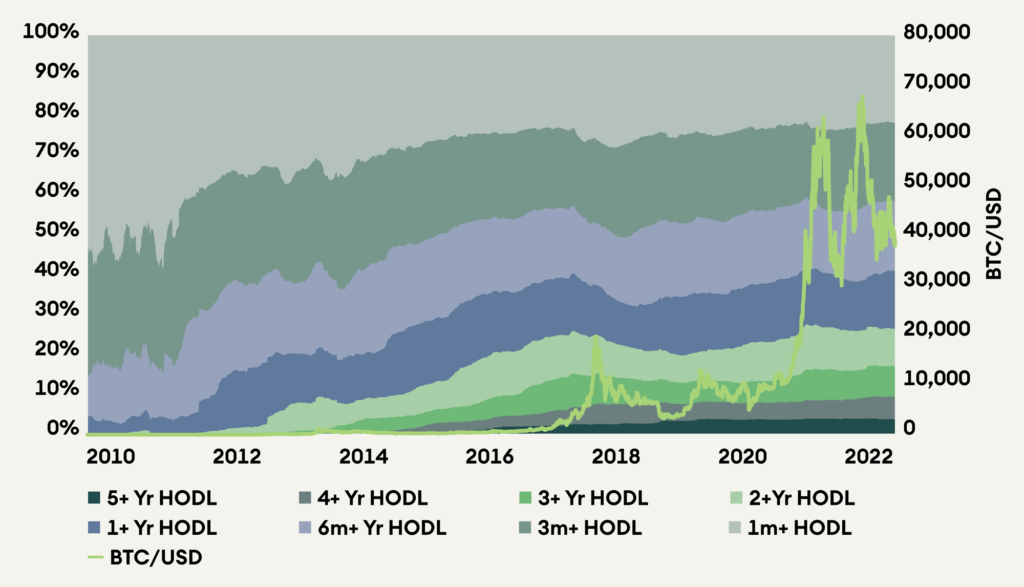

The HODL wave indicates the number of addresses holding their asset for more than a given time. As we have seen in the past, the same pattern repeats; new users get filtered during a correction after the bull run, and long-term holders start accumulating. Accounts holding for less than three months are reducing, and accounts holding for more than one year are increasing their holding.

Figure 1: Bitcoin HODL Wave

Ethereum

The second-largest cryptocurrency by market cap dropped about 18% last month, less than the broader market, from USD 3,500 levels to USD 2,800. Ethereum continues to be the most active and the biggest smart contract platform. The highly anticipated network upgrade ‘The Merge,’ initially scheduled for June 2022, is now delayed several months.

Two key events occurred last month for Ethereum. First, an Optimistic Rollup solution for layer 2 scaling, Optimism, announced their token airdrop (OP) for early supporters. The layer 2 ecosystem is big enough with 100+ DApps and approx. USD 500 million TVL in DeFi protocols. The number of unique addresses on the network shot up after the airdrop announcement, and there is steady growth in the daily transaction count. We talked about Optimism and how it works in one of our recent Crypto Market Monitor. Click here to read more.

The second event is that Yuga Labs, the company behind two of the most popular PFP NFT collections (BAYC, CryptoPunks), conducted one of the biggest NFT mints of all time on Ethereum, causing network congestion and a massive spike in transaction (gas) fees. The company raised USD 300 million by selling virtual land plots, and users spent a whopping USD 180 million in gas fees. Greater than expected demand for these NFTs caused some people to pay as much as USD 10,000+ for transactions that eventually failed. Yuga Labs has stated they will refund lost fees but also hinted at moving ApeCoin to its native blockchain to achieve high scalability.

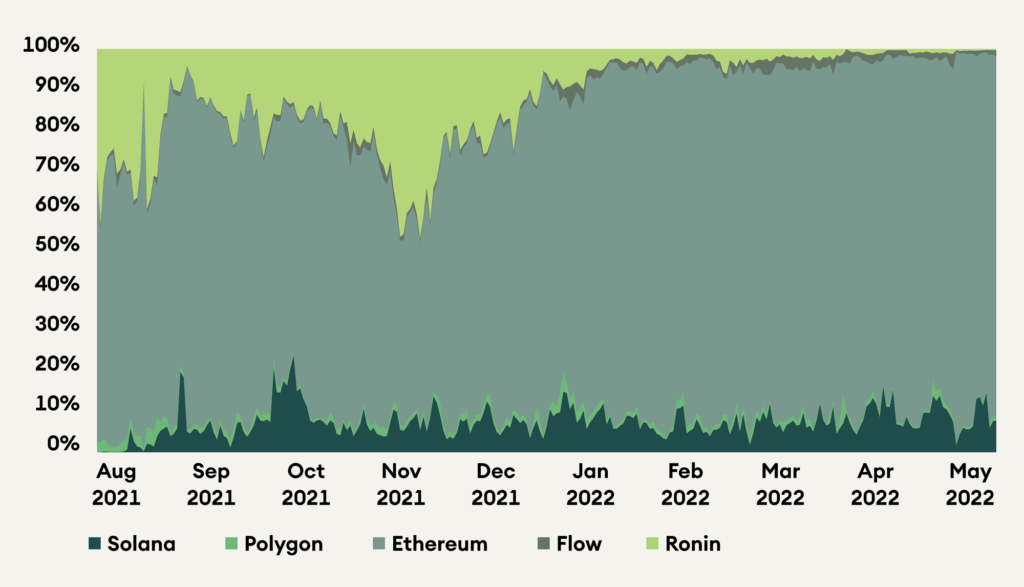

Further, during the rise of NFTs in 2021, alongside Ethereum, we saw many other smart contract platforms also adapting to NFTs and gaining market share. But as we continue to six-month-long duration since a new all-time high level, Ethereum has proved to be the most reliable platform for NFTs and is regaining market share, followed by Solana.

Figure 2: Daily NFT sales volume, with Ethereum leading the way

Alternative Blockchains

Alternative platform chains have followed the larger crypto market in terms of price movements; Avalanche (AVAX) fell by as much as 39%, followed by Polkadot (DOT) with 33%, and Litecoin (LTC) by 21%.

Ava Labs, the company developing Avalanche, raised funding of USD 350 million at a valuation of USD 5 billion. Polkadot Parachain auction for the 16th slot is underway, and it seems Polkadex will secure it with the help of 800,000 DOT (USD 12 million), raised from 1700+ contributors.

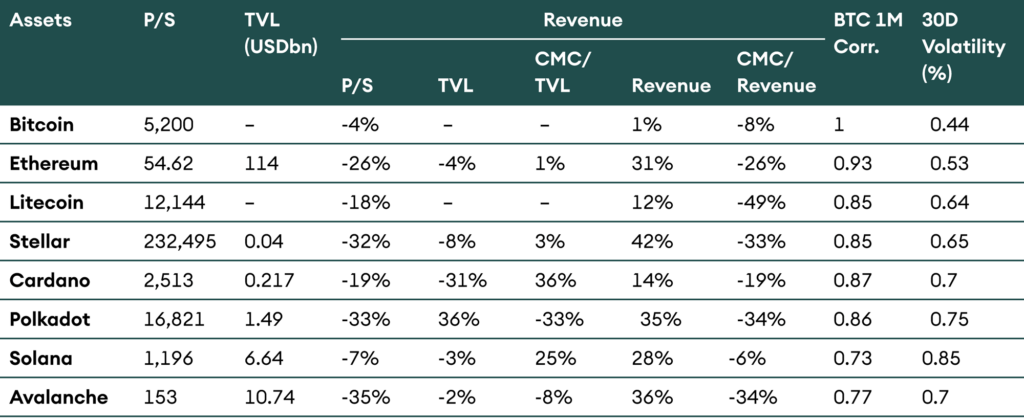

30-day volatility was low for most leading assets last month. While we see revenue growth in the table below, TVLs for key platforms are down except for Cardano and Polkadot. Indicating a low user growth rate in the DeFi ecosystem caused by a lack of innovation and the limitations of the technology.

Older payment altcoins such as Litecoin (LTC) and Stellar (XML) continue to gradually erode. Transaction counts and the number of developers is trending downwards.

Table 2: Valuation Overview

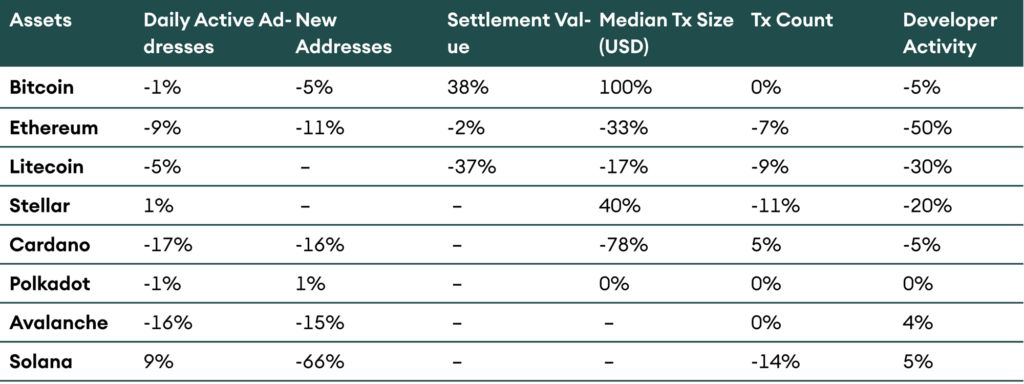

Daily active addresses, new user accounts, and transaction count are down for most assets with key exceptions, as seen below. NFT trading has been mainly responsible for a lot of on-chain user activity, but the daily NFT trading volume continues to decrease this month. The daily volume dropped by 60%, but the market cap only fell by 20% while gaining 10% new users every month.

Table 3: Fundamental Overview – 30D % change for all parameters

In a very uncertain macro-economic environment, like today, trust usually shifts towards hard assets, those who have seen the test of time and have been through multiple bull and bear cycles. Within the crypto ecosystem, only a handful of assets are eligible for the benefit of such a situation, BTC and ETH. These two assets have fallen the least and continue to be slightly safer.

Decentralised Finance (DeFi)

As we move towards the more application-specific assets, DeFi tokens, impact of macro parameters is significant, with UNI and AAVE prices dropping by 39% and YFI by 27%. As mentioned in the previous Digital Investors, the new user growth rate for the DeFi ecosystem is slowly declining. Keeping users on the platform is difficult as the only significant incentive is to generate a higher Annual Percentage Yield (APY). New projects usually offer higher APYs initially but fail to sustain them, resulting in most DeFi protocols taking the route of going multi-chain to retain/grow their user activity.

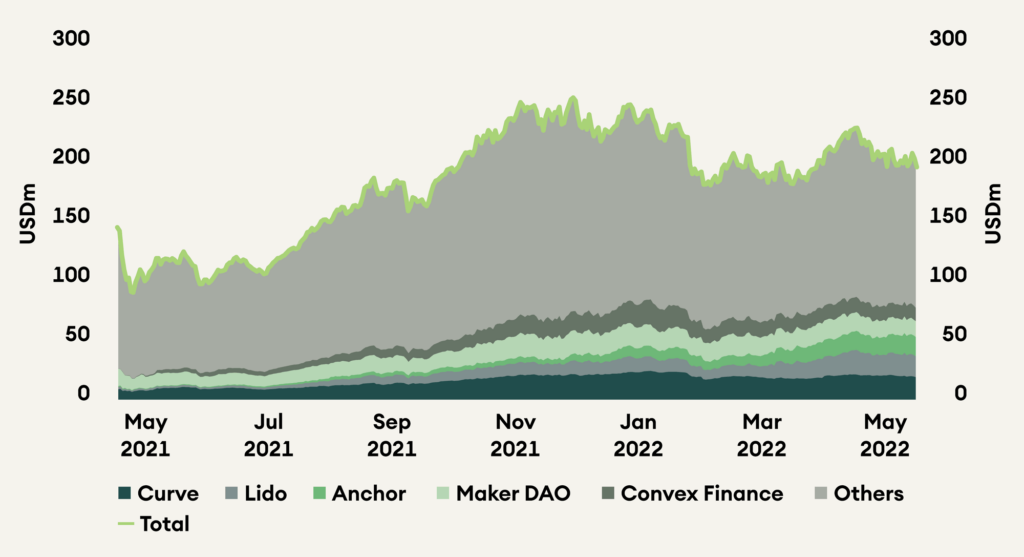

Tracking Total Value Locked (TVL) for leading DeFi protocols across multiple blockchains shows a clear plateauing trend since the beginning of 2022. Interesting to note that leading TVL protocols are related to providing some service for efficient use of stablecoins in the DeFi ecosystem.

DeFi takes a step back in the crypto ecosystem, especially with the rise of NFTs and Metaverse projects. Many leading brands are talking about associating themselves with the web3 world; some are buying NFTs for their balance sheets, and others are doing full-fledged NFT mints. DeFi ecosystem desperately needs some breakthrough innovation to be back on its exponential growth trajectory.

Figure 3: Total Value Locked (TVL) across chains in DeFi, with key contributors

Conclusion

Digital and traditional assets are moving in tandem. We think that this situation is likely to persist in the coming months as sentiment is expected to remain poor. According to our macroeconomic scenario, the war in Ukraine is set to continue, inflation will remain elevated, and the central bank will keep a hawkish tone. We expect growth and earnings expectations to be revised downwards in the coming months and weigh further on risky and digital assets.

Established assets around for a long time and with robust security are performing better than new platforms with a nascent ecosystem of DApps in the crypto space. Therefore, we prefer bitcoin and ether over altcoins and DeFi tokens.

The use of cryptocurrencies as a form of payments is rising, with now two countries in the world using bitcoin as legal tender and through layer 2 implementations for fast and cheap transactions. NFTs and metaverse projects still see high demand, as we witnessed one of the biggest NFT mints of all time only a couple of days ago.

We remain cautious in our portfolios and wait for a better time to increase our exposure to digital assets.