AMINA Bank AG

AMINA Bank AG  AMINA UK

AMINA UK  AMINA Hong Kong

AMINA Hong Kong  AMINA EU

AMINA EU Executive Summary

- The Digital Asset Market Clarity Act of 2025 (the CLARITY Act), passed with bipartisan support (294-134) on July 17, 2025, is a foundational step toward regulatory certainty for digital assets in the U.S.

- It introduces a functional classification of digital assets based on decentralization, replacing reliance on the traditional Howey Test.

- Jurisdiction over digital assets is clearly delineated between the SEC (Securities and Exchange Commission) and CFTC (Commodity Futures Trading Commission), depending on asset characteristics.

- Establishes new intermediary registration categories (DCE – Digital Commodity Exchange, DCB – Digital Commodity Broker, DCD – Digital Commodity Dealer) under the CFTC, with provisional registration to ensure smooth transition.

- Introduces capital formation pathways and secondary market clarity for compliant digital commodities.

- Offers legal clarity for DeFi (Decentralized Finance) participants and distinguishes between exempt and regulated DeFi functions.

- Overrides SAB 121 (Staff Accounting Bulletin 121), enabling traditional financial institutions to custody digital assets more efficiently.

- Consumer groups have raised concerns over preemption of state laws, limited dispute resolution pathways, and insufficient investor disclosures.

- The CLARITY Act helps U.S. stay globally competitive by providing regulatory clarity, aligning with frameworks like MiCA (Markets in Crypto-Assets Regulation – EU), PSA (Payment Services Act – Singapore), and China’s digital yuan model, the UK’s institutional-grade regulatory framework and Japan’s progressive self-regulatory model, reinforcing American leadership in digital finance through clear jurisdictional divisions between the SEC and CFTC.

Introduction: From Ambiguity to Regulatory Cohesion

The United States digital asset ecosystem has been hindered by inconsistent regulatory interpretation and adversarial enforcement practices. The CLARITY Act, introduced by Congressman French Hill, is a response to these systemic deficiencies. It builds upon the earlier FIT21 (Financial Innovation and Technology for the 21st Century Act) proposals and aims to end the era of “regulation-by-enforcement,” offering a predictable and rules-based framework. The bipartisan support (294-134) for the bill in the House demonstrates strong political will to embrace a long-term digital asset strategy.

Core Innovations and Structural Reforms

Functional Asset Classification

The CLARITY Act replaces the traditional reliance on the Howey Test with a decentralization-based classification methodology, thereby aligning regulatory definitions with technological realities. It introduces key categories such as “Digital Commodity,” “Investment Contract Asset,” and “Mature Blockchain System,” each assigned to the appropriate regulator (CFTC or SEC).

Jurisdictional Clarity

The Act ends regulatory turf wars by assigning oversight of spot markets in digital commodities to the CFTC while reserving the SEC’s role in securities oversight and anti-fraud enforcement. Interagency coordination is required via MOUs (Memoranda of Understanding) to streamline supervision. This delineation helps market participants understand which rules apply and to whom.

Transition Mechanism: Decentralization Pathway

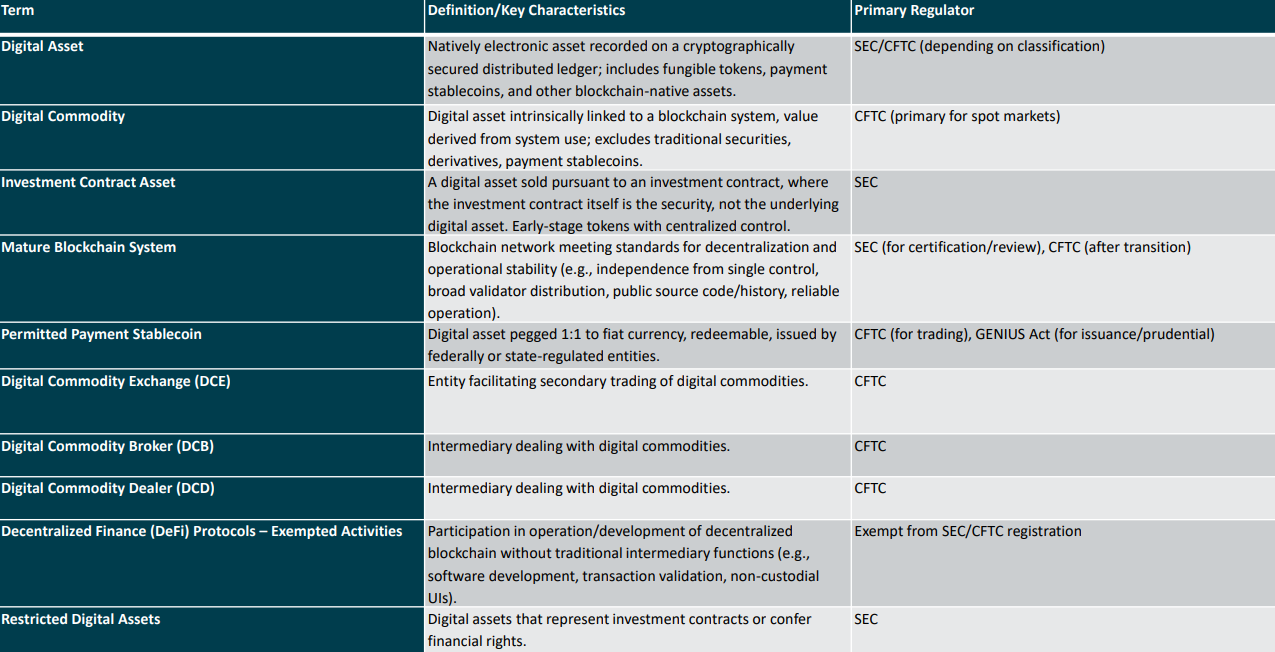

To support its functional asset classification model, the CLARITY Act defines a series of digital asset categories, their features, and corresponding regulators. These definitions serve as the foundation for assigning jurisdiction and tailoring compliance obligations.

Blockchain projects are allowed to declare their intent to achieve “mature blockchain system” status within four years. This mechanism offers a structured transition from SEC to CFTC regulation, encouraging decentralization as a compliance objective. The CLARITY Act thus incentivizes developers to progressively eliminate central control and reduce regulatory friction over time.

The following table provides a concise overview of these terms, their characteristics, and the assigned regulatory body:

Figure 1: Table Consisting Key Definitions and Regulatory Oversight under the CLARITY Act

Source: AMINA Bank AG

Regulatory Architecture for Intermediaries

New Registration Classes

The Act establishes three new intermediary categories under the CFTC: Digital Commodity Exchanges (DCEs), Brokers (DCBs), and Dealers (DCDs). These entities must comply with principles similar to those applied in traditional financial markets, including customer asset segregation, market integrity, and operational resilience. Their establishment addresses the prior regulatory vacuum in spot markets.

Provisional Regime & Dual Registration

To facilitate a smooth transition, the CLARITY Act provides a provisional registration process for existing entities. Firms dealing in both securities and commodities must register with both the SEC and CFTC, coordinated to avoid regulatory duplication. This dual structure ensures continuity while bridging the old and new regimes.

AML/KYC Integration

Entities registered with the CFTC must adhere to BSA (Bank Secrecy Act) standards, incorporating full AML (Anti-Money Laundering) and KYC (Know Your Customer) procedures, transaction monitoring, and reporting obligations. This positions crypto intermediaries within the scope of traditional financial compliance and helps prevent illicit finance.

DeFi: Acknowledging the Non-Custodial Model

The Act makes a crucial distinction between non-custodial, decentralized development and activities resembling traditional intermediaries. Developers, validators, and UI (User Interface) providers for DeFi (Decentralized Finance) protocols are not required to register, provided they do not exercise discretionary control or custody over customer assets. However, if a DeFi actor performs such functions, they are subject to full registration and oversight. This balance enables innovation without sacrificing accountability.

Capital Formation and Secondary Market Reforms

Digital Commodity Offering Exemption

The Act allows compliant issuers to raise up to $75 million per year without full SEC registration, provided disclosures meet specified standards and decentralization milestones are pursued. This exemption supports early-stage innovation while maintaining transparency, and offers a regulatory on-ramp to the digital economy.

Secondary Market Clarity

Tokens originally sold as part of investment contracts are no longer treated as securities in secondary markets once the initial sale concludes. This significantly reduces legal ambiguity for exchanges and investors, enhancing market liquidity and facilitating institutional entry.

Insider Controls

To prevent market manipulation, insiders are subject to trading lockups and volume restrictions, with reduced restrictions after the network achieves mature blockchain status. This ensures alignment between development teams and long-term market integrity.

Institutional Engagement: Enablers and Friction Points

Enablers

The CLARITY Act removes barriers that previously deterred institutional involvement. It overrides SEC guidance (SAB 121), allowing banks to custody digital assets off-balance sheet. It also classifies digital commodity activities as “financial in nature,” enabling BHCs (Bank Holding Companies) to offer related services and participate more fully in digital finance.

Challenges

Despite its benefits, compliance costs are expected to rise. Institutions must upgrade systems to meet AML/KYC mandates and prepare for the complexities of dual registration. This may require significant legal and technical investment, particularly for firms with global operations.

Consumer Protection: Balancing Growth with Accountability

Consumer advocacy groups have flagged potential issues with the CLARITY Act. These include concerns that federal preemption could weaken state-level legal protections, that the absence of a national dispute resolution framework may leave investors vulnerable, and that self-certification of decentralization might enable abuse. Additionally, critics argue that required disclosures are too technical for retail investors and that DeFi exemptions could be exploited by pseudo-centralized entities.

These concerns highlight the importance of careful rulemaking during the implementation phase. Transparent SEC and CFTC processes and guidance documents will be essential to ensuring accountability while sustaining innovation.

Implementation Outlook

The CLARITY Act awaits Senate consideration as of July 22,2025. Its success hinges on prompt rule issuance by the SEC and CFTC, clear standards for determining blockchain maturity, strong agency collaboration, and effective industry alignment with compliance goals. How quickly and transparently the regulators operationalize the CLARITY Act will determine its real-world success.

Conclusion

The CLARITY Act marks a regulatory inflection point for the U.S. digital asset market. It introduces a modern framework that supports innovation while preserving investor protection and market integrity. For institutional stakeholders, it offers long-needed regulatory certainty, opening pathways for broader participation in the crypto economy.

Ongoing monitoring of the Senate process and regulatory rulemaking will be essential to assess the CLARITY Act’s effectiveness and implementation trajectory.

Disclaimer – Research and Educational Content

This document has been prepared by AMINA Bank Ltd. (“AMINA”) in Switzerland. AMINA is a Swiss licensed bank and securities dealer with its head office and legal domicile in Switzerland. It is authorized and regulated by the Swiss Financial Market Supervisory Authority (“FINMA”).

This document is published solely for educational purposes; it is not an advertisement nor a solicitation or an offer to buy or sell any financial investment or to participate in any particular investment strategy. This document is for publication only on AMINA website, blog, and AMINA social media accounts as permitted by applicable law. It is not directed to, or intended for distribution to or use by, any person or entity who is a citizen or resident of or located in any locality, state, country or other jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation or would subject AMINA to any registration or licensing requirement within such jurisdiction.

Research will initiate, update and cease coverage solely at the discretion of AMINA. This document is based on various sources, incl. AMINA ones, and was generated using artificial intelligence (“AI”). No representation or warranty, either express or implied, is provided in relation to the accuracy, completeness or reliability of the information contained in this document, except with respect to information concerning AMINA. The information is not intended to be a complete statement or summary of the subjects alluded to in the document, whereas general information, financial investments, markets or developments. AMINA does not undertake to update or keep current information. Any statements contained in this document attributed to a third party represent AMINA’s interpretation of the data, information and/or opinions provided by that third party either publicly or through a subscription service, and such use and interpretation have not been reviewed by the third party.

Any formulas, equations, or prices stated in this document are for informational or explanatory purposes only and do not represent valuations for individual investments. There is no representation that any transaction can or could have been affected at those formulas, equations, or prices, and any formula(s), equation(s), or price(s) do not necessarily reflect AMINA’s internal books and records or theoretical model-based valuations and may be based on certain assumptions. Different assumptions by AMINA or any other source may yield substantially different results.

Nothing in this document constitutes a representation that any investment strategy or investment is suitable or appropriate to an investor’s individual circumstances or otherwise constitutes a personal recommendation. Investments involve risks, and investors should exercise prudence and their own judgment in making their investment decisions. Financial investments described in the document may not be eligible for sale in all jurisdictions or to certain categories of investors. Certain services and products are subject to legal restrictions and cannot be offered on an unrestricted basis to certain investors. Recipients are therefore asked to consult the restrictions relating to investments, products or services for further information. Furthermore, recipients may consult their legal/tax advisors should they require any clarifications.

At any time, investment decisions (including, among others, deposit, buy, sell or hold investments) made by AMINA and its employees may differ from or be contrary to the opinions expressed in AMINA research publications.

This document may not be reproduced, or copies circulated without prior authority of AMINA. Unless otherwise agreed in writing, AMINA expressly prohibits the distribution and transfer of this document to third parties for any reason. AMINA accepts no liability whatsoever for any claims or lawsuits from any third parties arising from the use or distribution of this document.

©AMINA, Kolinplatz 15, 6300 Zug