AMINA Bank AG

AMINA Bank AG  AMINA UK

AMINA UK  AMINA Hong Kong

AMINA Hong Kong  AMINA EU

AMINA EU Introduction

By early 2026, digital asset treasuries (DATs) have fully transitioned from a niche corporate experiment into a mainstream capital-markets strategy with growing institutional legitimacy. While the foundation of this model was laid in 2025, its implications became clearer as the market entered 2026 with scale, precedent, and institutional familiarity.

Public companies increasingly incorporated cryptocurrencies as core balance-sheet assets, with nearly 200 entities collectively holding over $110 billion currently and close to $180 billion at peak exposure. The underlying structure, issuing public equity or debt followed by systematic acquisition of a chosen digital asset, proved repeatable, financeable, and increasingly transparent to institutional investors who preferred public-market wrappers over direct token custody.

This evolution creates distinct operational requirements. Corporate treasurers deploying digital asset strategies need integrated treasury management, regulatory-compliant execution frameworks, and multi-jurisdictional banking partnerships that understand both traditional finance mechanics and crypto-native operations. The convergence is particularly evident in the expanding adoption of Ethereum treasury strategies, where staking income transforms pure accumulation into cash-generative balance sheet management.

The Expansion of DATs

The defining feature of this cycle was not the existence of DATs, but the breadth of adoption and the speed with which the playbook spread beyond Bitcoin. Strategy, led by Michael Saylor, remained the archetype. Beginning in 2020, the firm redirected excess cash and newly raised capital into Bitcoin, progressively transforming a legacy software business into a leveraged digital-asset accumulation vehicle.

Chart 1: Strategy (MSTR) Bitcoin Holdings vs Stock Price

Source: The Block (As on 01.29.2026)

As of 29th Jan 2026, Strategy holds 712,647 BTC, at an aggregate cost basis of about $54.19 billion (approximately $76,040 per BTC), representing around 3% of Bitcoin’s total supply and well over half of all BTC held by public companies. At the time of writing, Strategy’s BTC position is valued above $62.5 billion.

What changed during 2025—and now defines the 2026 landscape—is that this model began to be adopted as a generalized playbook. Corporate treasury inflows into digital assets accelerated throughout 2025, with the clearest inflection emerging in Q3. Data tracked by DeFiLlama showed several months of large net inflows into treasury strategies, with August and September together exceeding $23 billion. These inflows were not confined to a single issuer; rather, they reflected a structural shift in corporate financing behavior, with public companies increasingly using conventional instrument such as fund systematic digital-asset accumulation https://aminagroup.com/research/michael-saylors-microstrategy-bitcoin-trade/while presenting equity investors with a regulated, exchange-listed proxy.

This acceleration requires supporting infrastructure. Corporate treasury strategies at scale demand execution capabilities across multiple jurisdictions, institutional-grade custody meeting vary regulatory standards, and integrated banking services that combine traditional treasury management with crypto-native operations. The infrastructure gap—between what pure crypto exchanges offer and what traditional banks can provide—became increasingly obvious as adoption broadened beyond early-mover corporates to mainstream treasury operations.

Asset Allocation Trends

Bitcoin remained the dominant treasury asset, but 2025 marked the point at which Ethereum emerged as a credible corporate treasury alternative. That shift carries forward into 2026.

The investment rationale was straightforward: ETH functions both as a strategic balance sheet reserve and as a productive, yield-bearing asset through staking. As a result, ETH treasuries offered the possibility of recurring income that could support corporate liabilities and reduce dependence on continuous equity issuance.

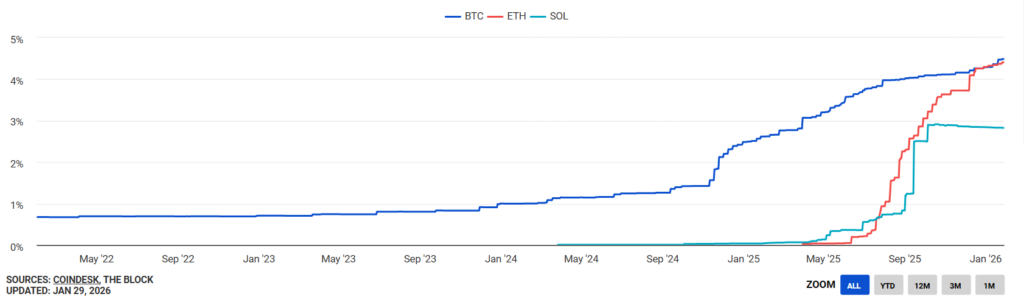

Chart 2: Percentage of Supply Held by Public Companies

Source: The Block (As on 01.29.2026)

ETH vs BTC as a Treasury Asset

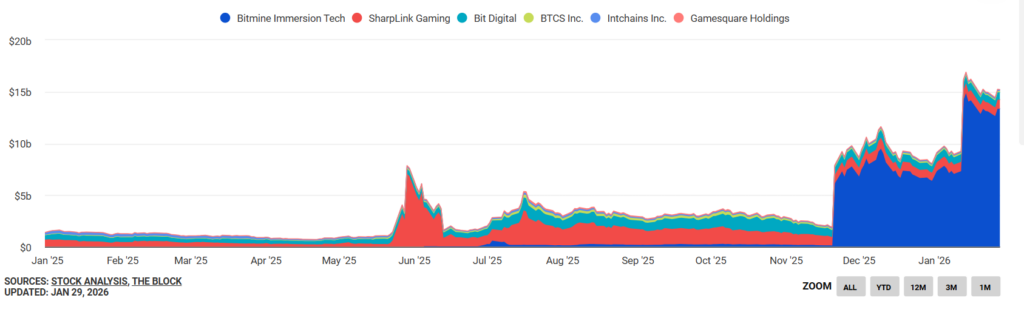

The most visible ETH treasury strategy in 2026 is BitMine Immersion Technologies (BMNR), chaired by Fundstrat’s Tom Lee. BitMine has emerged as the leading Ethereum treasury company by disclosed holdings, with approximately $13.47 billion in crypto assets, predominantly ETH with a smaller BTC allocation, and a stated ambition to accumulate 5% of total ETH supply.

Chart 3: Stacked Market Caps of Ethereum Treasury Companies

Source: The Block (As on 01.29.2026)

BitMine has begun deploying capital beyond pure accumulation, including equity investments in operating businesses such as Beast Industries, the wildly popular entertainment platform founded by Jimmy Donaldson (otherwise known as Mr. Beast).

From a treasury management perspective, the BitMine strategy highlights ETH’s differentiated mechanics: a large ETH base can be staked to generate cash flow, which can be used to service preferred dividends and coupon obligations. This distinction is critical because the primary vulnerability of treasury vehicles is not asset volatility in isolation, but funding continuity—the ability to service liabilities without forced issuance or asset sales during adverse market conditions.

Staking yield is the mechanism that potentially differentiates ETH treasury companies from BTC treasury companies. However, implementing institutional-grade staking operations introduces operational complexity that corporate treasurers must navigate. Staking infrastructure requires validator management, slashing risk mitigation, liquid staking protocol evaluation, and multi-jurisdictional regulatory compliance as staking classification varies across regulators. Corporate treasury teams deploying ETH strategies benefit from working with regulated banking partners offering integrated staking services combined into a unified regulatory framework rather than assembling fragmented service providers.

A staked ETH base effectively transforms a pure accumulation strategy into a hybrid carry and accumulation strategy. Under realistic yield assumptions in the 2–3% range, staking income can cover a meaningful portion of debt service at moderate leverage levels. The sensitivity is clear: coverage depends on the interaction between ETH price, staking yield, and leverage. At 50% leverage, staking income can cover most or all baseline obligations under reasonable parameters; at higher leverage, shortfalls increase, shifting the burden back onto capital markets.

The operational implication is that ETH treasury issuers have more levers: they can manage leverage, rotate into higher-yielding liquid staking structures, and time issuance more selectively—using converts during volatility spikes to keep coupons low and preserve flexibility, and using ATMs primarily when the equity trades at a premium to NAV.Valuation Frameworks: NAV and mNAV

NAV measures the market value of treasury assets held; mNAV measures the enterprise value premium (or discount) relative to NAV. A sustained premium enables efficient capital formation and accretive asset-per-share accumulation, reinforcing the treasury flywheel. A collapsing premium, by contrast, can force issuers into highly dilutive issuance, liquidity strain, or asset sales—especially for companies with limited operating cash flow outside treasury gains.

The difference between BTC and ETH treasury companies is therefore not only philosophical (“store of value” versus “productive asset”), but mechanical. BTC treasuries are structurally dependent on capital markets for ongoing funding if obligations exist, because BTC does not naturally generate yield. ETH treasuries can, in principle, offset part of that funding dependence through staking income, though that introduces its own operational, custody, and smart-contract risks if liquid staking or DeFi deployment is used.

The operational complexity of ETH treasury strategies—spanning custody, staking infrastructure, smart contract interactions, and multi-jurisdictional regulatory compliance—has driven demand for integrated banking solutions that consolidate these services within unified risk frameworks. This integration reduces operational fragmentation and becomes particularly valuable during market volatility when treasury flexibility matters most.

Regulatory Support and Market Infrastructure

The Q3 2025 inflection point was therefore not a single event, but a convergence: materially larger net inflows into treasury strategies, accelerating issuer formation, and visible diversification into multiple assets. The category’s growth was further supported by easing regulatory and operational constraints across multiple jurisdictions.

Regulatory clarity emerged as a critical enabler, though the path to clarity varied significantly by jurisdiction. In the United States, SEC guidance on protocol staking and liquid staking, published in May and August 2025, reduced a major regulatory overhang for ETH treasury strategies specifically.

In Europe, MiCA—fully applicable since early 2025—classified liquid staking tokens (LSTs) as regulated crypto assets, requiring service providers to meet standards on disclosures, custody, and operations, while emphasizing authorization and consumer protection over securities classification, thereby reducing uncertainty for staking services across EU member states.

Switzerland’s FINMA issued new staking guidance in July 2025, allowing licensed institutions to offer direct staking without capital requirements under strict conditions like asset segregation, providing a pragmatic compliance path for supervised entities handling ETH staking.

Abu Dhabi’s FSRA proposed a dedicated staking framework in October 2025 via Consultation Paper No. 10, regulating proof-of-stake validation with client protections, permissions for custody and management, and comprehensive disclosures, while explicitly noting awareness of LST issuance but focusing on core staking activities.

Hong Kong’s SFC and HKMA released joint guidance on 7 April 2025, permitting licensed platforms and funds to offer staking services and enabling ETH spot ETFs with staking rewards, supporting yield opportunities within regulated environments aligned with the jurisdiction’s virtual asset roadmap.

At the same time, lower borrowing costs through mid-2025 improved the economics of debt-funded accumulation. The combination of regulatory clarity, favourable financing conditions, and maturing operational infrastructure laid the groundwork for the institutional-grade treasury strategies now visible in early 2026.

Outlook

Entering 2026, digital asset treasuries have become one of the most visible points of convergence between traditional equity markets and crypto balance sheets. Looking ahead, the sector’s long-term durability will depend less price performance and more on whether issuers evolve from passive accumulation toward institutional-grade treasury management: consistent disclosure, conservative leverage policy, disciplined issuance practices, and effectively timing the capital raises.

Disclaimer – Research and Educational Content

This document has been prepared by AMINA Bank Ltd. (“AMINA”). AMINA is a Swiss licensed bank and securities dealer with its head office and legal domicile in Switzerland. It is authorized and regulated by the Swiss Financial Market Supervisory Authority (“FINMA”).

This document is published solely for educational purposes; it is not an advertisement nor a solicitation or an offer to buy or sell any financial investment or to participate in any particular investment strategy. This document is for publication only on AMINA website, blog, and AMINA social media accounts as permitted by applicable law. It is not directed to, or intended for distribution to or use by, any person or entity who is a citizen or resident of or located in any locality, state, country or other jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation or would subject AMINA to any registration or licensing requirement within such jurisdiction.

Research will initiate, update and cease coverage solely at the discretion of AMINA. This document is based on various sources, incl. AMINA ones. In preparing this document, AMINA may have made limited use of artificial intelligence–enabled tools to assist with research, summarisation, and drafting, with all content subject to human review and validation.

No representation or warranty, either express or implied, is provided in relation to the accuracy, completeness or reliability of the information contained in this document, except with respect to information concerning AMINA. The information is not intended to be a complete statement or summary of the subjects alluded to in the document, whereas general information, financial investments, markets or developments. AMINA does not undertake to update or keep current information. Any statements contained in this document attributed to a third party represent AMINA’s interpretation of the data, information and/or opinions provided by that third party either publicly or through a subscription service, and such use and interpretation have not been reviewed by the third party.

Any formulas, equations, or prices stated in this document are for informational or explanatory purposes only and do not represent valuations for individual investments. There is no representation that any transaction can or could have been affected at those formulas, equations, or prices, and any formula(s), equation(s), or price(s) do not necessarily reflect AMINA’s internal books and records or theoretical model-based valuations and may be based on certain assumptions. Different assumptions by AMINA or any other source may yield substantially different results.

Nothing in this document constitutes a representation that any investment strategy or investment is suitable or appropriate to an investor’s individual circumstances or otherwise constitutes a personal recommendation. Investments involve risks, and investors should exercise prudence and their own judgment in making their investment decisions. Financial investments described in the document may not be eligible for sale in all jurisdictions or to certain categories of investors. Certain services and products are subject to legal restrictions and cannot be offered on an unrestricted basis to certain investors. Recipients are therefore asked to consult the restrictions relating to investments, products or services for further information. Furthermore, recipients may consult their legal/tax advisors should they require any clarifications.

At any time, investment decisions (including, among others, deposit, buy, sell or hold investments) made by AMINA and its employees may differ from or be contrary to the opinions expressed in AMINA research publications.

This document may not be reproduced, or copies circulated without prior authority of AMINA. Unless otherwise agreed in writing, AMINA expressly prohibits the distribution and transfer of this document to third parties for any reason. AMINA accepts no liability whatsoever for any claims or lawsuits from any third parties arising from the use or distribution of this document.

©2026 AMINA, Kolinplatz 15, 6300 Zug