AMINA Bank AG

AMINA Bank AG  AMINA UK

AMINA UK  AMINA Hong Kong

AMINA Hong Kong  AMINA EU

AMINA EU Ethereum’s market sentiment has improved significantly over the past six months. Trading around $2,000 in March while Bitcoin hovered near $80,000, ETH appeared to be losing ground in the broader crypto narrative. Today, the picture looks different, with ETH trading above $4,300. The ETH/BTC ratio has climbed 80% in the same period, moving from 0.20 to 0.36, signaling renewed confidence in Ethereum’s value proposition relative to Bitcoin.

Two catalysts are driving this reversal: Digital Asset Treasuries (DATs) accumulating ETH and the passage of stablecoin legislation in the U.S. But this raises critical questions about sustainability. Can DAT accumulation and regulatory clarity alone justify Ethereum’s current momentum? More importantly, is the network infrastructure ready to handle an influx of new users and higher transaction volumes?

In this edition of Crypto Market Monitor, we explore whether this momentum rests on solid foundations or fleeting market dynamics.

The Rise of Digital Asset Treasuries

Corporate treasuries are taking an active approach to ETH accumulation. Public companies such as BitMine Immersion Technologies (NYSEAMERICAN: BMNR) and SharpLink Gaming (NASDAQ: SBET) are issuing equity to purchase ETH, mirroring the BTC treasury playbook but with a key difference. Unlike Strategy (MSTR), which passively holds BTC, DATs are exploring staking and DeFi protocols to generate yield on their holdings.

This distinction matters. ETH based DATs function like active portfolio management, where risk-reward optimisation determines returns. Deploying ETH to a lending protocol carries different smart contract risks and rewards compared to staking with a validator. These strategic choices are creating performance variations across different treasury operations, making DATs a more complex investment vehicle than simple asset accumulation strategies.

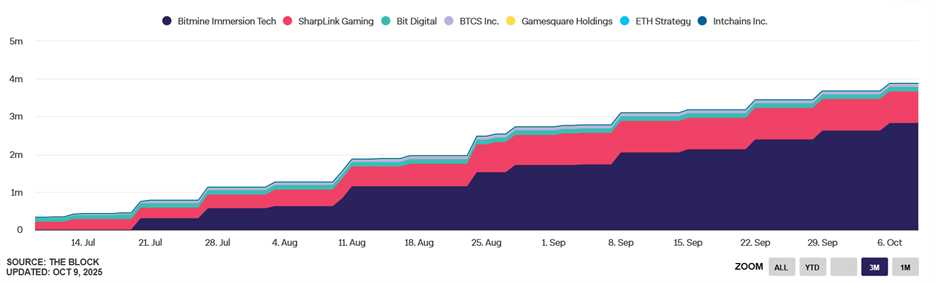

Ethereum treasury companies collectively hold around 5.66 million ETH, equivalent to 4.68% of total supply. Meanwhile, spot Ethereum ETFs hold roughly 6.81 million ETH, or 5.63% of the total supply.

Figure 1: Total ETH holdings by public companies hovers around 5.66 million.

Source: The Block (9 October 2025)

How DATs Work

Understanding how DATs are valued reveals both their attractiveness and inherent risks. These vehicles generally trade above the market value of their underlying ETH holdings – a spread measured by the multiple-of-net-asset-value (mNAV) metric. Investors pay this premium based on the leverage these structures provide and expectations around future Ethereum ecosystem participation.

This premium, however, creates a precarious dependency. DATs need elevated mNAV levels (a level greater than 1) to continue raising capital through equity offerings. When ETH price declines and mNAV compresses, the ability to raise funds diminishes.

Reduced capital inflows cause the equity premium to collapse. When DATs can no longer raise capital at a premium to NAV, their growth model breaks down. Companies trading at discounts may choose to buy back shares using treasury assets, or face shareholder pressure for asset liquidation. Additionally, firms with debt/dividend obligations or insufficient operating revenue may be forced to liquidate holdings to meet expenses, creating downward pressure on ETH prices.

This selling pressure extends beyond spot markets – it can disrupt staking operations and DeFi protocol stability, potentially amplifying losses across the ecosystem.

Yield Generation

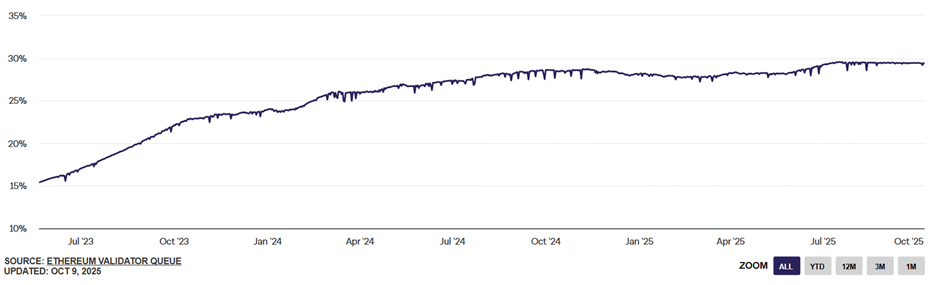

To offset these risks and create sustainable revenue streams, treasuries are increasingly turning to validator staking. Staking rewards represent the baseline yield available from holding ETH. Since November 2024, these returns have been trending downward as total staked ETH increases on the network. Current validator earnings sit around 3%, derived from both base staking rewards and priority fees collected from transactions.

Figure 2: Percentage of total ETH supply staked

Source: The Block (9 October 2025)

This institutional shift toward staking is gaining momentum. Grayscale announced on October 6 that staking functionality is now integrated into its Ethereum Mini Trust ETF (ETH) and Ethereum Trust ETF (ETHE). Investors in these products can now capture staking yields directly, choosing between automatic reinvestment or receiving cash distributions—a development that brings crypto-native yield mechanisms into traditional investment structures.

Network Activity

While institutional players are positioning themselves through DATs and staking, the underlying network is demonstrating its capacity to handle real-world usage. Daily transaction volume on Ethereum has crossed the 1.5 million mark, exceeding the previous peak established in May 2021. More telling is the value being transferred: stablecoin transfers have surged past $60 billion in a single day in Sep 2025—more than double of YTD 2025 average. This volume spans the full spectrum of use cases, from small cross-border remittances to large-scale institutional settlements, indicating that Ethereum is serving as infrastructure for diverse financial activity.

Figure 3: Transaction count on Ethereum Mainnet

Source: The Block (9 October 2025)

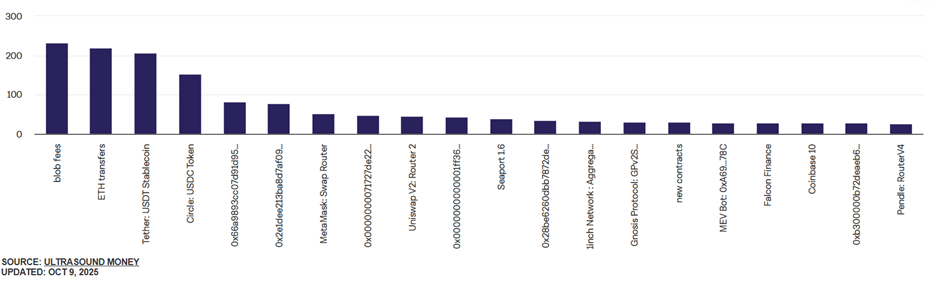

The network’s ability to absorb this growth without deteriorating user experience stems from scaling improvements at multiple layers. Layer-2 networks are posting increasing amounts of blob data to Ethereum’s base layer, which allows them to process higher transaction counts without creating fee spikes.

Figure 4: Top gas guzzler smart contracts on Ethereum Mainnet

Source: The Block (9 October 2025)

Following the Pectra upgrade in May, which raised blob inclusion targets, Ethereum blocks are now routinely carrying more blob data. This expansion is simultaneously increasing throughput capacity and reducing transaction costs across the Layer-2 ecosystem, creating the conditions for sustained usage growth without pricing out smaller participants.

Stablecoin Dominance

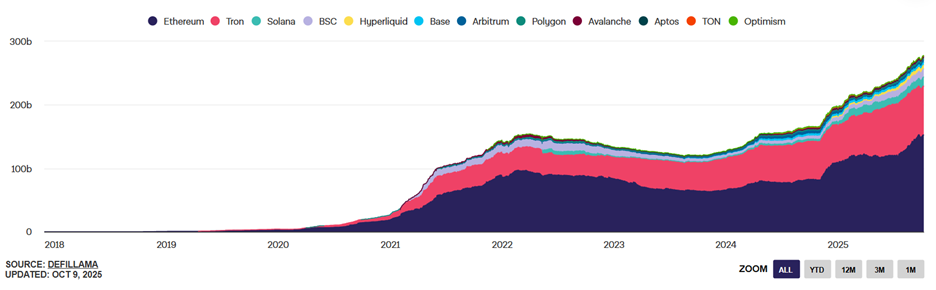

Much of this transaction growth is being fueled by stablecoin activity. Ethereum currently hosts approximately 65% of all stablecoin supply, making it the dominant settlement layer for dollar-denominated digital assets. The passage of the GENIUS Act in the U.S. and broader acceptance of stablecoins as viable payment alternatives have expanded interest among both retail users and commercial entities. This concentration of stablecoin activity is creating organic demand for ETH as users need it for transaction fees and as collateral in various protocols.

Figure 5: Stablecoin supply by chain

Source: The Block (9 October 2025)

However, Ethereum’s stablecoin leadership position faces emerging challenges. The rise of application-specific blockchains designed exclusively for stablecoin settlement (for example – Plasma), along with stablecoins built natively on new generation blockchains, exposes weaknesses in Ethereum’s architecture. These alternatives are gaining traction precisely because they address pain points that Ethereum hasn’t fully solved, calling into question whether stablecoin growth will continue benefiting Ethereum as much as it has historically.

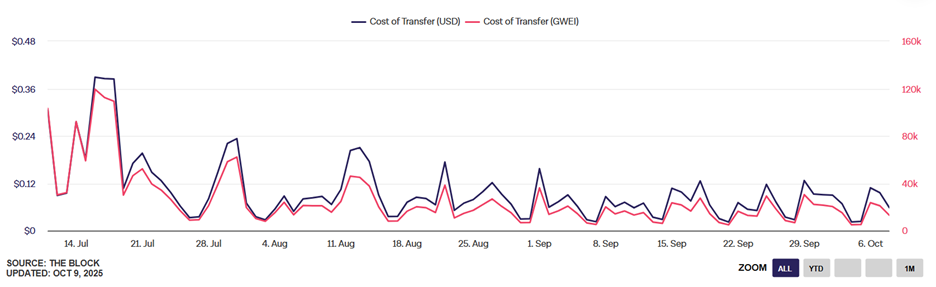

The fee dynamic illustrates this tension. While Ethereum’s transaction costs have decreased, they remain several orders of magnitude higher than alternative networks. For users making frequent, smaller-value stablecoin transfers, these fees become prohibitive.

Figure 6: Transfer costs on Ethereum still remain higher than alternative networks

Source: The Block (9 October 2025)

Layer-2 solutions offer a partial answer—providing the low costs and high speeds necessary for stablecoin scaling—but they bring their own complications. Activity on Layer-2s doesn’t directly translate to base layer activity on Ethereum, meaning the network doesn’t capture the same economic value from L2 stablecoin transactions as it would from mainnet usage.

The Fusaka Upgrade

Recognising these scaling challenges, Ethereum developers are targeting the Fulu-Osaka (Fusaka) upgrade for release on 3rd December 2025 tentatively. The centerpiece of this upgrade is PeerDAS (Data Availability Sampling), which addresses validator efficiency at the consensus layer. Rather than requiring validators to download complete blob datasets for verification, PeerDAS enables them to work with data samples. This approach cuts validator operational costs while accelerating data retrieval speeds – improvements that become increasingly critical as blob usage expands across Layer-2 networks.

Conclusion

Ethereum has recaptured institutional attention and market momentum. Sustaining this trajectory depends on two primary drivers continuing: DATs maintaining their ETH accumulation programs and applications choosing Ethereum as their stablecoin settlement layer. The stablecoin scaling challenge remains real – technical constraints limit how much transaction throughput the network can handle for these transfers.

Yet these constraints haven’t prevented overall network usage from climbing. Ethereum processes higher transaction volumes by optimising for operations that require less computational intensity, which keeps costs manageable for users. The infrastructure is positioning itself to absorb both increased transaction counts and more computation-heavy operations through two parallel paths: expanded blob data capacity on Layer-2s and mainnet gas limit increases.

Both completed upgrades and the upcoming Fusaka release are building a technical foundation for renewed ecosystem engagement. The question isn’t whether Ethereum can scale – the pieces are falling into place. The question is whether the economic incentives around DATs and stablecoin adoption will remain aligned long enough to translate into token value proposition.

___________________________________________

Disclaimer – Research

This document has been prepared by AMINA Bank Ltd. (“AMINA”) in Switzerland. AMINA is a Swiss licensed bank and securities dealer with its head office and legal domicile in Switzerland. It is authorized and regulated by the Swiss Financial Market Supervisory Authority (“FINMA”).

This document is published solely for educational purposes; it is not an advertisement nor a solicitation or an offer to buy or sell any financial investment or to participate in any particular investment strategy. This document is for publication only on AMINA website, blog, and AMINA social media accounts as permitted by applicable law. It is not directed to, or intended for distribution to or use by, any person or entity who is a citizen or resident of or located in any locality, state, country or other jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation or would subject AMINA to any registration or licensing requirement within such jurisdiction.

Research will initiate, update and cease coverage solely at the discretion of AMINA. This document is based on various sources, incl. AMINA ones, and was generated using artificial intelligence (“AI”). No representation or warranty, either express or implied, is provided in relation to the accuracy, completeness or reliability of the information contained in this document, except with respect to information concerning AMINA. The information is not intended to be a complete statement or summary of the subjects alluded to in the document, whereas general information, financial investments, markets or developments. AMINA does not undertake to update or keep current information. Any statements contained in this document attributed to a third party represent AMINA’s interpretation of the data, information and/or opinions provided by that third party either publicly or through a subscription service, and such use and interpretation have not been reviewed by the third party.

Any formulas, equations, or prices stated in this document are for informational or explanatory purposes only and do not represent valuations for individual investments. There is no representation that any transaction can or could have been affected at those formulas, equations, or prices, and any formula(s), equation(s), or price(s) do not necessarily reflect AMINA’s internal books and records or theoretical model-based valuations and may be based on certain assumptions. Different assumptions by AMINA or any other source may yield substantially different results.

Nothing in this document constitutes a representation that any investment strategy or investment is suitable or appropriate to an investor’s individual circumstances or otherwise constitutes a personal recommendation. Investments involve risks, and investors should exercise prudence and their own judgment in making their investment decisions. Financial investments described in the document may not be eligible for sale in all jurisdictions or to certain categories of investors. Certain services and products are subject to legal restrictions and cannot be offered on an unrestricted basis to certain investors. Recipients are therefore asked to consult the restrictions relating to investments, products or services for further information. Furthermore, recipients may consult their legal/tax advisors should they require any clarifications.

At any time, investment decisions (including, among others, deposit, buy, sell or hold investments) made by AMINA and its employees may differ from or be contrary to the opinions expressed in AMINA research publications.

This document may not be reproduced, or copies circulated without prior authority of AMINA. Unless otherwise agreed in writing, AMINA expressly prohibits the distribution and transfer of this document to third parties for any reason. AMINA accepts no liability whatsoever for any claims or lawsuits from any third parties arising from the use or distribution of this document.

©AMINA, Kolinplatz 15, 6300 Zug