AMINA Bank AG

AMINA Bank AG  AMINA UK

AMINA UK  AMINA Hong Kong

AMINA Hong Kong  AMINA EU

AMINA EU As the Markets in Crypto-Assets Regulation (MiCA) moves from policy to practice, the European Union has entered a phase of active supervision and market consolidation. What began as a regulatory blueprint in 2020 is now a living financial ecosystem populated by authorised issuers and service providers. This second part of the MiCA series examines the emerging institutional landscape by classifying entities registered under MiCA and analysing the patterns shaping Europe’s regulated crypto economy.

The New Foundation of Trust: EMT Issuers

At the core of MiCA’s framework are Electronic Money Tokens (EMTs), designed to bridge traditional finance and blockchain-based value transfer. EMTs are single-currency stablecoins fully backed by fiat reserves and redeemable at par value. Their issuers must hold an e-money licence, maintain transparent reserve audits, and comply with capital and redemption requirements defined by the European Banking Authority (EBA).

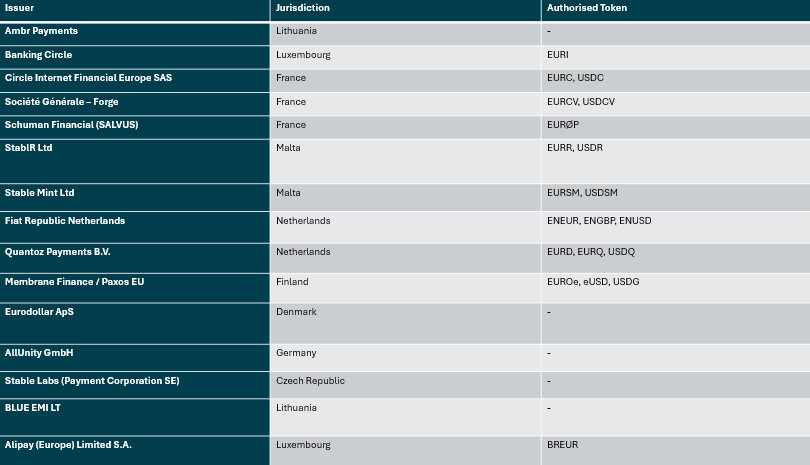

As of October 2025, eleven entities have been authorised to issue EMTs across the European Economic Area. These firms range from regulated fintechs to established banking institutions, marking a significant shift from speculative token issuance to institution-grade digital money infrastructure.

Figure 1: MiCA Authorised Electronic Money Token (EMT) Issuers

Source: MiCA – EMT Issuers List

France, Malta, and the Netherlands have emerged as preferred hubs for MiCA-compliant stablecoin issuers, reflecting their early regulatory alignment and robust digital-asset licensing frameworks. Circle’s authorisation of both EURC and USDC within France exemplifies MiCA’s global resonance, while Société Générale – Forge’s EURCV stablecoin anchors the banking sector’s direct participation in tokenised payment instruments.

The Service Layer: CASP Authorisations and Market Infrastructure

Beyond token issuance, MiCA’s second pillar governs Crypto-Asset Service Providers (CASPs). These include exchanges, custodians, brokers, trading venues, and portfolio managers. CASPs are required to maintain capital adequacy, ensure customer-asset segregation, and establish internal governance controls aligned with EU AML and KYC rules.

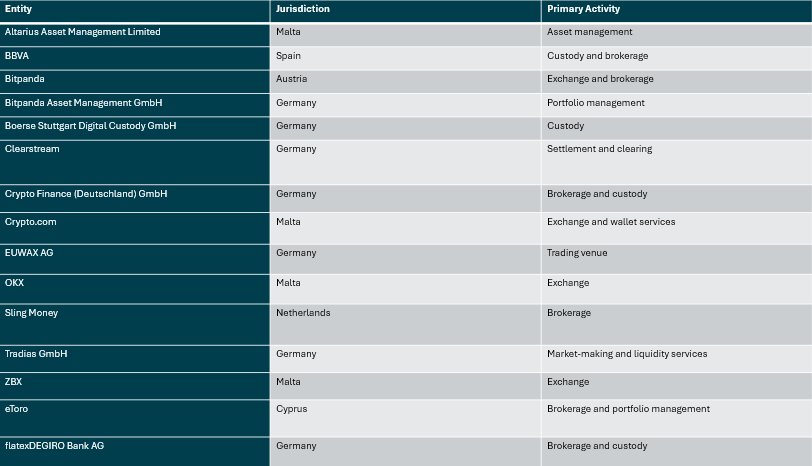

By September 2025, a growing cohort of firms had obtained CASP authorisation, transforming Europe into a unified market for compliant digital-asset services. The current distribution demonstrates a blend of traditional financial institutions and native crypto companies, signalling increasing convergence between the two worlds.

Figure 2: MiCA Authorised Crypto-Asset Service Providers (CASPs)

Germany and Malta have established themselves as the dominant jurisdictions for CASP licensing, accounting for more than half of all active authorisations. The presence of both traditional exchanges such as Boerse Stuttgart and crypto-native platforms like OKX and Bitpanda underscores MiCA’s capacity to integrate legacy and Web3 finance within a single regulatory perimeter.

Observations and Market Dynamics

The structure of authorisations reveals three key dynamics:

- Institutional Convergence: Traditional financial institutions such as Société Générale, BBVA, and Clearstream are now operating alongside crypto incumbents under the same rulebook. This signals a shift from parallel financial systems to an interoperable digital asset economy.

- Jurisdictional Leadership: Germany and Malta’s proactive supervisory approaches have accelerated approvals, giving them first-mover advantages in establishing digital-asset clusters. France, meanwhile, continues to lead in fiat-backed stablecoin issuance.

- Strategic Maturity: Entities obtaining early authorisation are positioning themselves as liquidity providers and market infrastructure enablers ahead of the 2026 transition deadline. This early compliance not only secures regulatory certainty but also opens cross-border passporting rights throughout the EU.

The Road Ahead

MiCA’s early registry paints a picture of consolidation rather than fragmentation. A handful of well-capitalised and compliance-ready firms now dominate issuance and service provision, while smaller or non-EU entities face higher barriers to entry.

In parallel, France has recently called on the European Union to give the European Securities and Markets Authority (ESMA) direct oversight of major crypto firms and stablecoin issuers. The proposal, supported by the Bank of France, highlights growing momentum toward centralised supervision to reduce regulatory arbitrage among member states. If adopted, this change could transform MiCA’s current passport-based model into a more unified EU-level supervisory framework, reinforcing consistency and systemic stability across the bloc.

The European Securities and Markets Authority (ESMA) and the European Banking Authority (EBA) are scheduled to deliver a joint supervisory review by December 2025. This review is expected to address operational resilience, cross-border supervision, and the treatment of algorithmic or decentralised stablecoins. By 2027, the legislative review will likely expand MiCA’s scope to DeFi protocols, tokenised securities, and NFTs, completing Europe’s digital-asset rulebook.

Conclusion

MiCA has transitioned from a theoretical framework to a functioning regulatory ecosystem. Its authorised entities now form the foundation of Europe’s on-chain financial infrastructure, defining how value is issued, stored, and transferred across borders. With the first wave of EMT and CASP approvals now public, the MiCA landscape offers an early glimpse into the institutional architecture of a compliant digital-asset market that is no longer speculative but systematically integrated into Europe’s financial core.

Disclaimer

This document has been prepared by AMINA Bank Ltd. (“AMINA”) in Switzerland. AMINA is a Swiss licensed bank and securities dealer with its head office and legal domicile in Switzerland. It is authorized and regulated by the Swiss Financial Market Supervisory Authority (“FINMA”).

This document is published solely for educational purposes; it is not an advertisement nor a solicitation or an offer to buy or sell any financial investment or to participate in any particular investment strategy. This document is for publication only on AMINA website, blog, and AMINA social media accounts as permitted by applicable law. It is not directed to, or intended for distribution to or use by, any person or entity who is a citizen or resident of or located in any locality, state, country or other jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation or would subject AMINA to any registration or licensing requirement within such jurisdiction.

Research will initiate, update and cease coverage solely at the discretion of AMINA. This document is based on various sources, incl. AMINA ones, and was generated using artificial intelligence (“AI”). No representation or warranty, either express or implied, is provided in relation to the accuracy, completeness or reliability of the information contained in this document, except with respect to information concerning AMINA. The information is not intended to be a complete statement or summary of the subjects alluded to in the document, whereas general information, financial investments, markets or developments. AMINA does not undertake to update or keep current information. Any statements contained in this document attributed to a third party represent AMINA’s interpretation of the data, information and/or opinions provided by that third party either publicly or through a subscription service, and such use and interpretation have not been reviewed by the third party.

Any formulas, equations, or prices stated in this document are for informational or explanatory purposes only and do not represent valuations for individual investments. There is no representation that any transaction can or could have been affected at those formulas, equations, or prices, and any formula(s), equation(s), or price(s) do not necessarily reflect AMINA’s internal books and records or theoretical model-based valuations and may be based on certain assumptions. Different assumptions by AMINA or any other source may yield substantially different results.

Nothing in this document constitutes a representation that any investment strategy or investment is suitable or appropriate to an investor’s individual circumstances or otherwise constitutes a personal recommendation. Investments involve risks, and investors should exercise prudence and their own judgment in making their investment decisions. Financial investments described in the document may not be eligible for sale in all jurisdictions or to certain categories of investors. Certain services and products are subject to legal restrictions and cannot be offered on an unrestricted basis to certain investors. Recipients are therefore asked to consult the restrictions relating to investments, products or services for further information. Furthermore, recipients may consult their legal/tax advisors should they require any clarifications.

At any time, investment decisions (including, among others, deposit, buy, sell or hold investments) made by AMINA and its employees may differ from or be contrary to the opinions expressed in AMINA research publications.

This document may not be reproduced, or copies circulated without prior authority of AMINA. Unless otherwise agreed in writing, AMINA expressly prohibits the distribution and transfer of this document to third parties for any reason. AMINA accepts no liability whatsoever for any claims or lawsuits from any third parties arising from the use or distribution of this document.

©AMINA, Kolinplatz 15, 6300 Zug