AMINA Bank AG

AMINA Bank AG  AMINA UK

AMINA UK  AMINA Hong Kong

AMINA Hong Kong  AMINA EU

AMINA EU Introduction

January 2026 presented with a paradox: crypto prices fell 25% yet the infrastructure supporting institutional adoption sped up.

While Bitcoin declined to a ten-month low near $73,000, BlackRock designed digital assets as a defining investment theme for 2026. While leveraged traders liquidated $2.2 billion in positions, the Depository Trust and Clearing Corporation launched production-grade tokenisation for US Treasuries and equities. While sentiment indices reached extreme pessimism, Y Combinator announced it would start funding startups in USDC.

The first two months of 2026 marked a decisive transition for the digital asset market. What initially appeared to be a disorderly sell-off was, in reality, a broad macro repricing driven by sovereign risk, monetary regime changes, and the forced unwind of global leverage. Unlike previous crypto drawdowns, this episode did not originate within the digital asset ecosystem itself. It emerged from outside of it.

January and February revealed a paradox now central to institutional crypto era. Market prices deteriorated sharply, yet regulatory clarity, infrastructure deployment and institutional commitment advanced at unprecedented speed. This divergence between price action and structural progress defines the current phase of the cycle.

This update analyses how macroeconomic shocks destabilized crypto market structure, why Bitcoin faced an identity challenge as a macro asset, and how institutional capital continued to build through volatility rather than retreat from it.

Institutional Expansion Beneath Market Weakness

Despite the deterioration in spot prices, institutional engagement accelerated rather than slowed. This acceleration reveals a fundamental shift in how sophisticated allocators approach digital assets: infrastructure maturity now matters more than price momentum.

Tokenisation Becomes Core Strategy

BlackRock formally identified digital assets and tokenization as defining investment themes for 2026, placing them alongside artificial intelligence as structural drivers of capital markets.

At Franklin Templeton, innovation leadership described 2026 as the beginning of a wallet native financial system, where equities, bonds and funds are held directly in digital wallets rather than through legacy custodial frameworks.

A pivotal signal came from Y Combinator, which announced that from its Spring 2026 batch onwards, startups may receive funding in USDC across Ethereum, Base and Solana. Stablecoin settlement now routinely clears in under one second at costs below $0.01, offering clear advantages over cross-border fiat rails.

Regulatory Friction Recedes

Regulatory developments quietly removed long-standing structural barriers. The SEC rescinded accounting guidance that had previously discouraged banks from offering digital asset custody services. Concurrently, the Depository Trust and Clearing Corporation launched a production-grade tokenization programme for US Treasuries, large-cap equities and ETFs confirming legal equivalence between tokenised and securities.

This marked a transition from experimental adoption to internal financial infrastructure upgrade.

Regional Competition for Crypto Capital

Jurisdictions increasingly deployed policy as a competitive lever.

Hong Kong announced zero-tax incentives on qualifying digital asset gains for funds and family offices, positioning itself as Asia’s primary institutional crypto hub. By January 2026, 11 licensed virtual asset trading platforms were operational.

Meanwhile, Dubai continued executing its blockchain-first government strategy, targeting on-chain processing for 50% of public sector transactions by the end of 2026. Crypto penetration in the UAE has reached approximately 39% representing over 3.7 million users.

The Macroeconomic Shock That Broke the Calm

Understanding why institutions continued building requires understanding what drive the selloff. The relative stability of 2025 fostered expectations that crypto had entered a lower volatility, institutionally anchored phase. Those assumptions were dismantled in January.

Japan and the Unwinding of Global Leverage

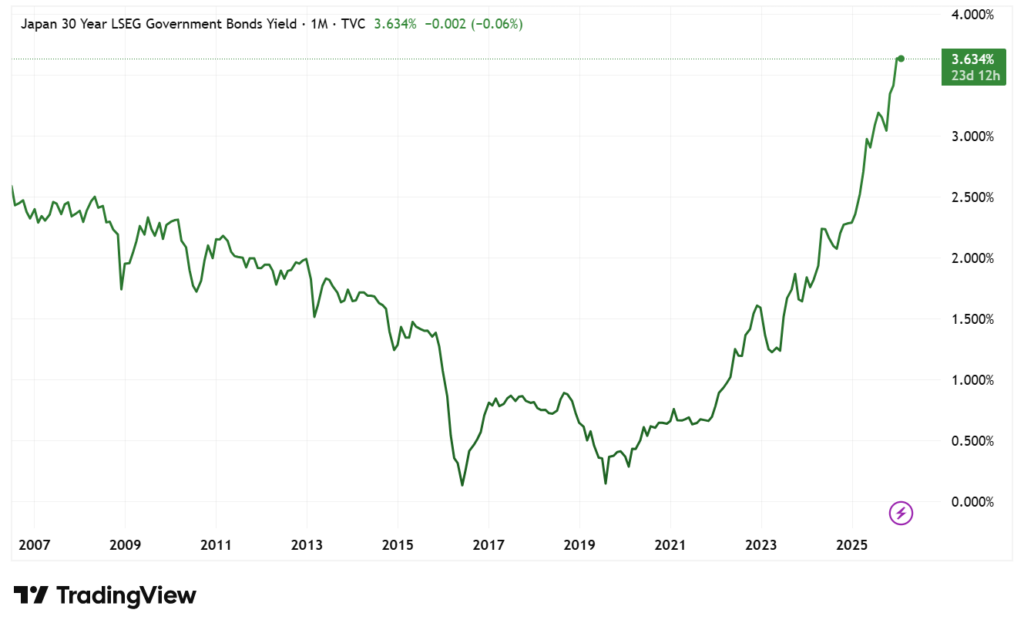

On 20 January 2026, Japan’s government bond market entered acute stress. Thirty-year JGB yield surged more than 30 basis points to 3.91%, the highest level in 27 years, following fiscal rhetoric from Prime Minister Sanae Takaichi that intensified concerns over debt sustainability. Japan’s debt-to-GDP ratio, already exceeding 250%, became the focal point of global bond markets.

Figure 1: Japan 30-Year Government Bond Yield (Historical)

Source: TradingView

The immediate consequence was a rapid unwind of the yen carry trade, one of the largest sources of cheap global leverage. As yen funding costs rose, investors were forced to liquidate risk assets to meet margin requirements. Bitcoin fell below $91000, not due to crypto-specific weakness, but because it functioned as a liquid proxy for balance-sheet repair.

The Warsh Nomination and Monetary Repricing

This pressure escalated on 30 January with the nomination of Kevin Warsh as the next Federal Reserve Chair. Warsh’s long-standing preference for higher real interest rates and a materially smaller Federal Reserve balance sheet was interpreted as a definitive shift away from accommodative monetary policy.

Within 24 hours, the total cryptocurrency market capitalisation declined by approximately $430 billion. Bitcoin fell roughly 7% in a single session, while Ethereum and high-beta altcoins experienced double-digit percentage drawdowns. The move reflected a repricing of global dollar liquidity expectations rather than speculative panic.

Price Action and the Bitcoin Identity Crisis

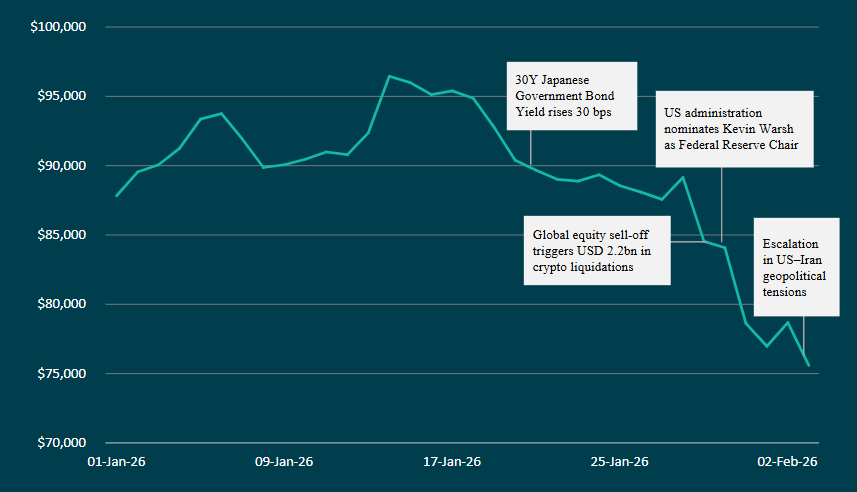

The macro shocks revealed an uncomfortable truth about Bitcoin’s evolution as an institutional asset. The final week of January produced one of the most severe single day dislocations of the institutional era.

On 29 January, Bitcoin declined from $96,000 to $80,000, a single-day drop of approximately 15%. More than $2.2 Billion in leveraged positions were liquidated across crypto derivatives markets. The significance of the move lay not in its magnitude, but in its correlation profile.

Bitcoin failed to decouple from equities and instead traded in line with high-beta technology stocks. Rather than acting as a defensive sheet, it behaved as a liquidity-sensitive risk instrument during a global deleveraging event.

By early February, sentiment indicators reflected extreme pessimism. The Crypto Fear and Greed Index fell to 19, while key technical levels, including the 0.786 Fibonacci retracement at $85,400, were decisively breached. The high $70000s emerged as the market’s primary structural support zone.

Figure 2: Bitcoin Price Decline Driven by Global Macro Events (Jan–Feb 2026)

Source: AMINA Bank

The correlation profile raises fundamental questions about Bitcoin’s role institutional portfolios. If it behaves as a high-beta technology proxy during stress rather than as a defensive hedge, the allocation thesis must adapt accordingly. Yet, institutional commitment continues regardless, suggesting that sophisticated allocators are pricing Bitcoin for its long-term structural role rather than its short-term correlation behaviour.

Protocol Evolution and Competitive Differentiation

While prices declined and macro conditions deteriorated, base-layer development continued uniterrupted. This demonstrates a crucial characteristic of the current cycle: infrastructure development has decoupled from price momentum.

Ethereum remains focused on scaling through execution efficiency, censorship resistance, and MEV mitigation. The upcoming Glamsterdam upgrade targets a gas limit increase toward 200m, with theoretical throughput approaching 10,000 TPS.

Solana is pursuing aggressive performance gains. Its Alpenglow upgrade aims to reduce transaction finality from 12.8 seconds to approximately 100–150 milliseconds, positioning it as one of the fastest settlement layers in production.

These technical advances continue regardless of market sentiment, reflecting long-term capital commitments and engineering devleopments that happen independently of price action.

Security Losses Highlight Operational Risk

Even as institutional infrastructure matured, security incidents underscored persistent operational vulnerabilities. January 2026 recorded over $370 million in stolen funds, the highest monthly total in nearly a year. More than $311 million losses resulted from phishing and social engineering attacks rather than smart contract failures.

The largest single incident exceeded $280 million, involving AI-generated voice impersonation targeting a hardware wallet user. These events underline a structural shift in risk. Human and operational vulnerabilities now represent the dominant attack surface for institutional crypto participants.

This pattern reinforces why custody frameworks operating under regulatory oversight provide competitive advantages beyond compliance. Operational security protocols, institutional-grade key management, and insurance frameworks have become table stakes.

Conclusion

The January–February 2026 drawdown was not a rejection of digital assets, but a repricing within a changing global monetary regime. Crypto now responds directly to sovereign bond markets, central bank leadership, and geopolitical escalation. That sensitivity introduces volatility, but it also confirms integration.

At the same time, institutional adoption, regulatory clarity, and protocol development advanced through the sell-off. Tokenisation moved from narrative to deployed infrastructure, and wallet-native finance shifted from theory to implementation.

Early 2026 did not mark a breakdown of the crypto market. It marked the first genuine stress test of its institutional maturity. And while prices failed the test, the underlying infrastructure passed with flying colours.

The divergence between price action and structural progress with not persist indefinitely as institutional deployment, regulatory clarification, and infrastructure maturation will be reflected in market valuations eventually.

Disclaimer – Research and Educational Content

This document has been prepared by AMINA Bank AG (“AMINA”). AMINA is a Swiss licensed bank and securities dealer with its head office and legal domicile in Switzerland. It is authorized and regulated by the Swiss Financial Market Supervisory Authority (“FINMA”).

This document is published solely for educational purposes; it is not an advertisement nor a solicitation or an offer to buy or sell any financial investment or to participate in any particular investment strategy. This document is for publication only on AMINA website, blog, and AMINA social media accounts as permitted by applicable law. It is not directed to, or intended for distribution to or use by, any person or entity who is a citizen or resident of or located in any locality, state, country or other jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation or would subject AMINA to any registration or licensing requirement within such jurisdiction.

Research will initiate, update and cease coverage solely at the discretion of AMINA. This document is based on various sources, incl. AMINA ones. In preparing this document, AMINA may have made limited use of artificial intelligence–enabled tools to assist with research, summarisation, and drafting, with all content subject to human review and validation.

No representation or warranty, either express or implied, is provided in relation to the accuracy, completeness or reliability of the information contained in this document, except with respect to information concerning AMINA. The information is not intended to be a complete statement or summary of the subjects alluded to in the document, whereas general information, financial investments, markets or developments. AMINA does not undertake to update or keep current information. Any statements contained in this document attributed to a third party represent AMINA’s interpretation of the data, information and/or opinions provided by that third party either publicly or through a subscription service, and such use and interpretation have not been reviewed by the third party.

Any formulas, equations, or prices stated in this document are for informational or explanatory purposes only and do not represent valuations for individual investments. There is no representation that any transaction can or could have been affected at those formulas, equations, or prices, and any formula(s), equation(s), or price(s) do not necessarily reflect AMINA’s internal books and records or theoretical model-based valuations and may be based on certain assumptions. Different assumptions by AMINA or any other source may yield substantially different results.

Nothing in this document constitutes a representation that any investment strategy or investment is suitable or appropriate to an investor’s individual circumstances or otherwise constitutes a personal recommendation. Investments involve risks, and investors should exercise prudence and their own judgment in making their investment decisions. Financial investments described in the document may not be eligible for sale in all jurisdictions or to certain categories of investors. Certain services and products are subject to legal restrictions and cannot be offered on an unrestricted basis to certain investors. Recipients are therefore asked to consult the restrictions relating to investments, products or services for further information. Furthermore, recipients may consult their legal/tax advisors should they require any clarifications.

At any time, investment decisions (including, among others, deposit, buy, sell or hold investments) made by AMINA and its employees may differ from or be contrary to the opinions expressed in AMINA research publications.

This document may not be reproduced, or copies circulated without prior authority of AMINA. Unless otherwise agreed in writing, AMINA expressly prohibits the distribution and transfer of this document to third parties for any reason. AMINA accepts no liability whatsoever for any claims or lawsuits from any third parties arising from the use or distribution of this document.

©2026 AMINA, Kolinplatz 15, 6300 Zug