AMINA Bank AG

AMINA Bank AG  AMINA UK

AMINA UK  AMINA Hong Kong

AMINA Hong Kong  AMINA EU

AMINA EU

Executive summary

- July was a challenging month with mixed performances in global equities and cryptocurrency markets.

- Technology and communication services were the worst-performing sectors after an 18-month rally.

- The Fed left interest rates unchanged but indicated significant progress in reducing inflation, suggesting a possible rate cut in September 2024.

- The anticipated US interest rate cuts could lead to rising prices of risk assets and Trump’s potential election win could create a favorable regulatory environment for the crypto industry.

- For July, Solana and Aave were top performers Bitcoin and Ethereum moved sideways.

- Multiple onchain indicators including the accumulation trend score, the reserve risk metric and the sell-side risk ratio indicate that Bitcoin has entered oversold conditions.

- The nine US spot ETH ETFs launched in July generated $6.62 billion in total volume, saw net outflows of over $462 million post listing and their total AUM currently stands at $8.46 billion. Meanwhile in the month of July, the US spot Bitcoin ETFs did close to $38 billion in total volume, saw net inflows of over $3.16 billion and their cumulative AUM stands at $54 billion.

- The SEC’s recent move to back off from labeling many major altcoins as securities is a positive step that could bring more stability.

Introduction

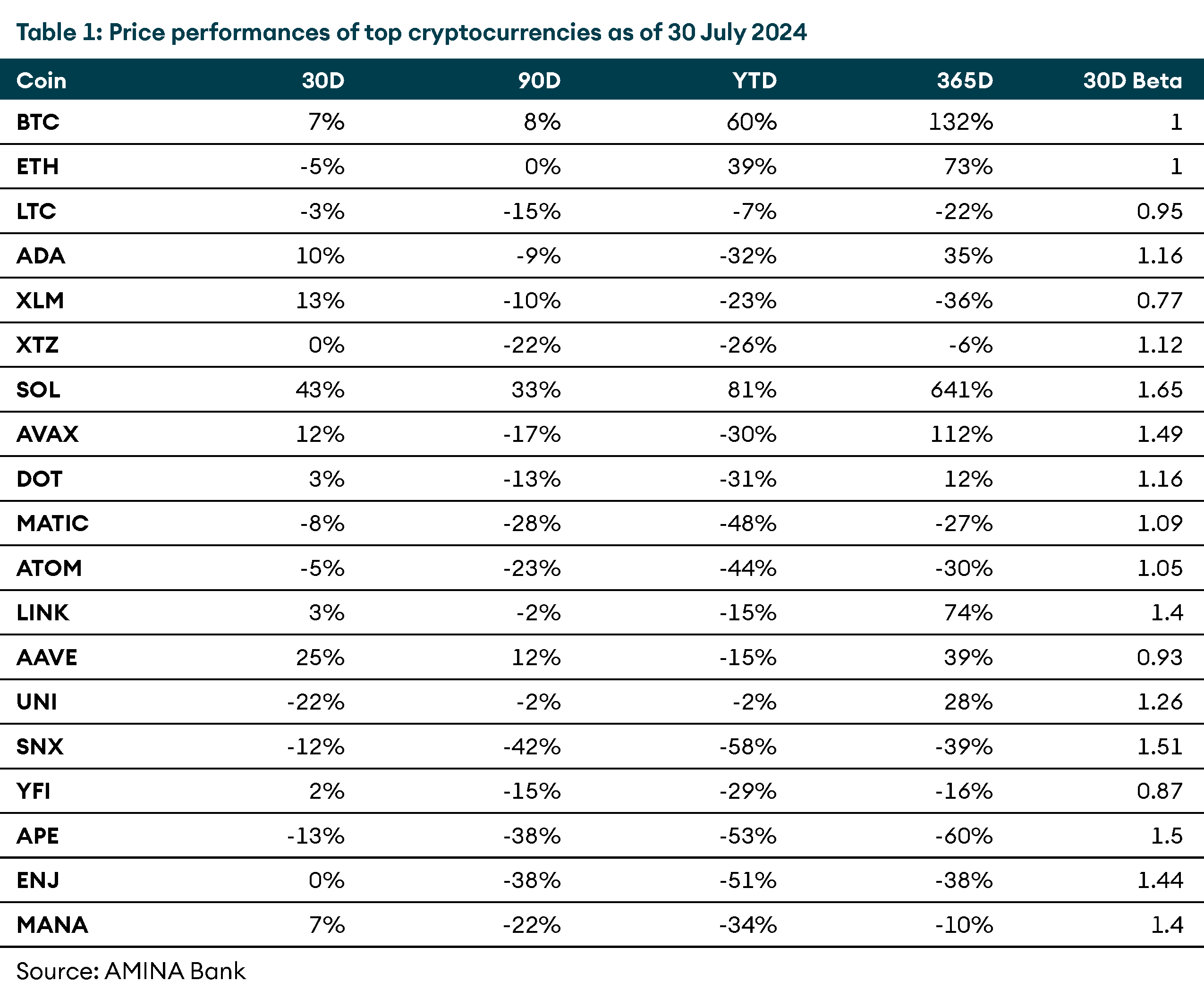

July saw mixed performances across global equities, with corporate earnings taking center stage. Wall Street experienced one of its worst months, wiping out nearly $985 billion off Nasdaq’s market cap. Despite this, there were glimmers of optimism although the US Fed kept rates unchanged. In crypto, SOL (+43%) and AAVE (+25%) were top performers for the past month while BTC (+7%) and ETH (-5%) moved sideways.

Table 1: Price performances of top cryptocurrencies as of 30 July 2024

This blog delves into the recent turbulence in the US stock market, the current state of Bitcoin’s investor cohort onchain, the shifting dynamics of Ethereum and a few key developments in the decentralised finance (DeFi) sector.

Macroeconomy

Throughout July 2024, global equities largely moved sideways, with corporate earnings taking center stage. The S&P 500 rose by 1.01%, while the Nasdaq and the Euro Stoxx 50 fell by 1.62% and 0.44%, respectively. In the US, inflation was lower than expected, pushing bond yields down. Large tech companies saw a sharp sell-off due to weak earnings outlooks, increasing recession fears among investors. Technology and communication services were the worst-performing sectors after an 18-month rally. Investors shifted towards risk-off sectors. The Fed left interest rates unchanged but indicated significant progress in reducing inflation, suggesting a possible rate cut in September 2024. Currently, the possibility of a rate cut in September stands at 99.5% according to CME FedWatch.

Meanwhile, European equities rallied early in July following the UK Labour’s election victory but lost gains later due to uncertainty over the French election and mixed earnings. Chinese equity markets have been in a downtrend since mid-May 2024, with investors worried about the government’s lack of progress in improving the struggling property market. In Japan, the yen rallied against the dollar, with USDJPY falling below 150 for the first time in four months. Towards the end of July, the Bank of Japan hiked interest rates for the first time since 2007. This led to a ripple effect which caused drawdowns across global markets.

Throughout July, crypto continued to make waves in US politics. Republican presidential candidate Donald Trump spoke at the Bitcoin 2024 conference in Nashville, promising to boost energy production to support Bitcoin miners, replace the current anti-crypto SEC Chairman Gary Gensler and establish a US Strategic Bitcoin Stockpile. Trump wasn’t alone in his pro-crypto stance. Independent candidate Robert F. Kennedy Jr. pledged to buy 4 million BTC for the US government if elected. Wyoming Senator Cynthia Lummis also introduced a bill to create a strategic Bitcoin reserve, aiming to accumulate 1 million BTC over five years. Meanwhile, Democratic nominee Kamala Harris is reportedly meeting with crypto giants like Ripple, Coinbase, and Circle to strengthen her party’s ties with the crypto community. The fact that multiple candidates are courting the crypto vote highlights the industry’s growing influence and how quickly its political significance can shift even in a major economy like the United States.

Bitcoin

There were two main sources of sell pressure last month: Bitcoin seized by the German government, and Bitcoins used for repaying creditors by Mt. Gox. After over a decade of legal processes, the long-awaited creditor distribution of Bitcoin recovered from the Mt. Gox exchange collapse is underway. This marks a historic event for the Bitcoin industry, especially for the patient creditors who fought to be reimbursed in BTC rather than fiat currency. Over 141K BTC were recovered, with just under 59K BTC redistributed to creditors and another 79.6K BTC soon to follow. Psychologically, this represents a big chapter in a major market overhang since 2013. Meanwhile, the German government has now sold-off all the 50K BTC (worth roughly $45.9 million) that it confiscated from a movie pirating website earlier.

Currently, on-chain trends show a positive medium-to-long-term future for BTC. The supply of long-term holders is increasing while short-term holders are declining. Many coins acquired during the height of the BTC ETF hype in Q1 2024 are likely transitioning into long-term holding status, which should accelerate this divergence. A higher proportion of

long-term holders signify greater strength for BTC and higher long-term market conviction regardless of short-term sentiment.

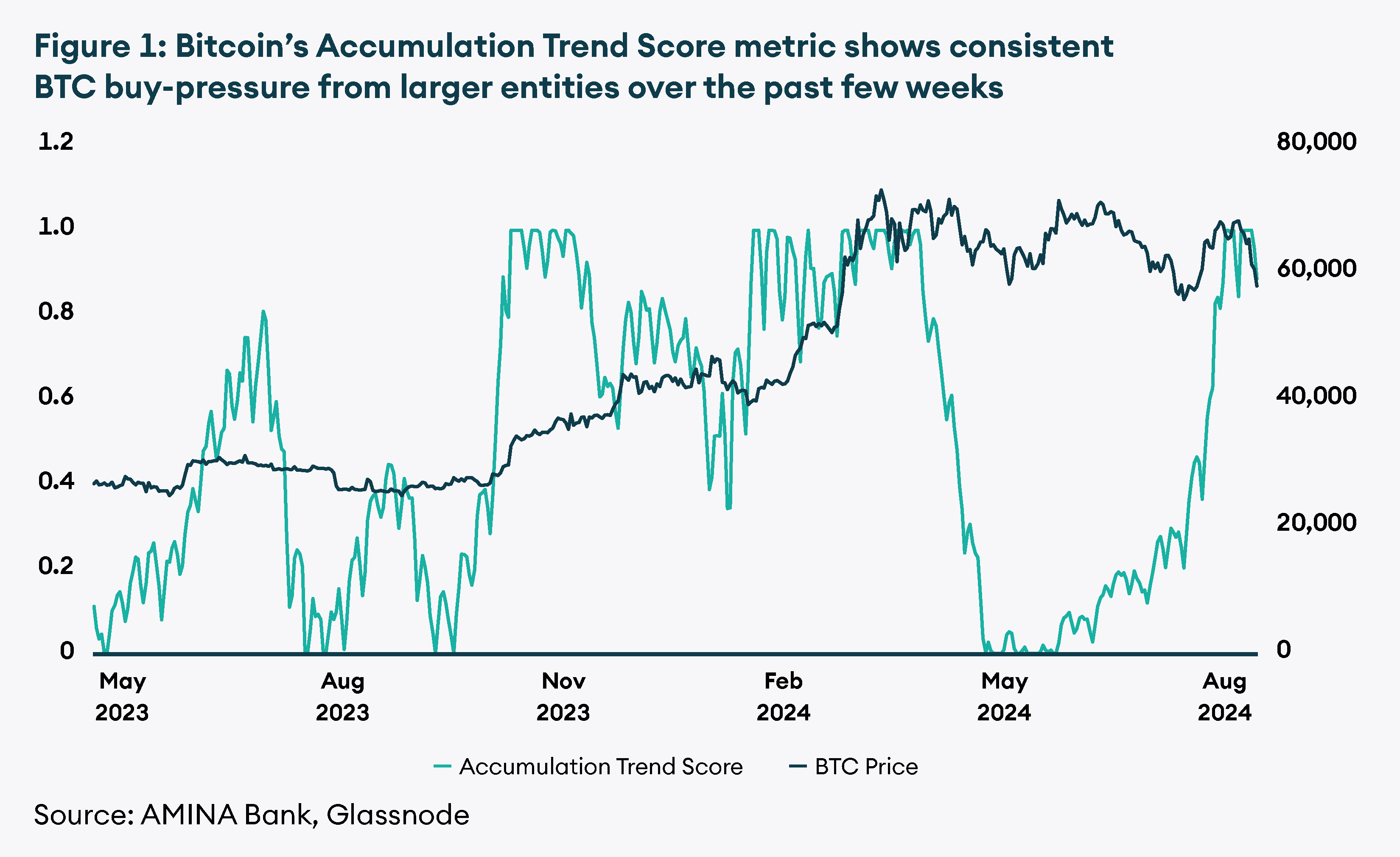

The Accumulation Trend Score (ATS) reflects the relative size of entities actively accumulating coins on-chain. An ATS closer to 1 indicates large entities are accumulating, while a value closer to 0 indicates distribution or lack of accumulation.

Figure 1: Bitcoin’s Accumulation Trend Score metric shows consistent BTC buy-pressure from larger entities over the past few weeks

Despite consecutive price drops in July, the ATS metric has consistently moved higher, hitting its upper limit of 1 more than five times in the past month. This generally indicates an upcoming price rally for BTC, as seen in Q4 2023 when BTC made all-time highs after the ATS hovered around its upper limit.

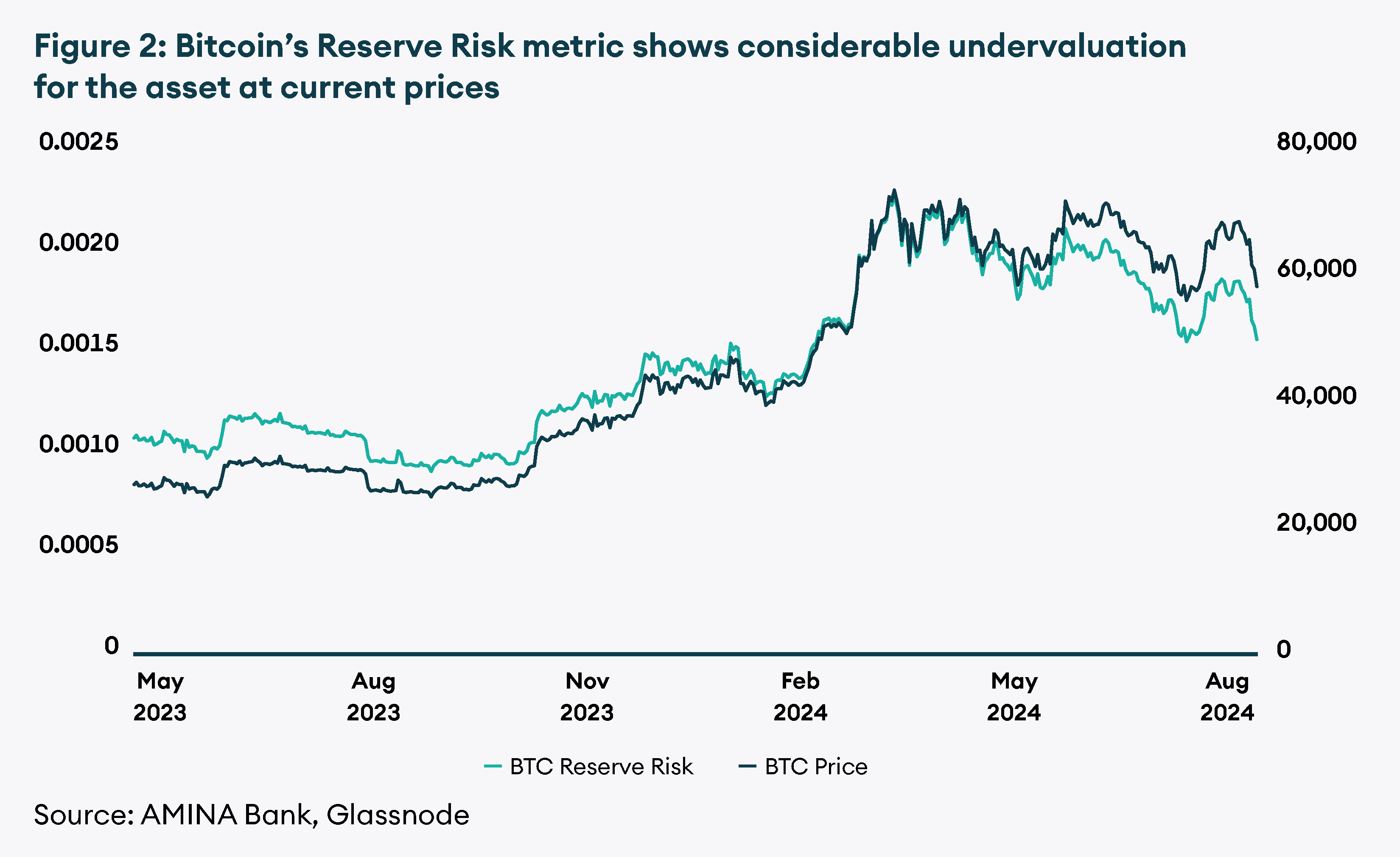

The Bitcoin Reserve Risk (RR) metric assesses the confidence of long-term holders relative to BTC’s price. To understand reserve risk, it’s important to understand Bitcoin’s Days Destroyed (BDD) and the HODL Bank.

BDD: Bitcoin’s Days Destroyed represents the number of coin-days lost when a Bitcoin is moved from its idle state. It is calculated by the number of days the Bitcoin was held without movement before its transfer or transaction. For example, if a Bitcoin was held for 7 days and then moved, its BDD would be 7, reflecting the value of those 7 coin-days that were “destroyed” upon the transaction. (To be clear, Bitcoin itself is not destroyed here.)

During periods of accumulation, BDD is low and during periods of selloffs, BDD is relatively higher since long-term holders finally decide to sell.

HODL Bank: Between buying and selling, BTC holders pay an opportunity cost to hold these BTC instead of selling them at market prices. The accumulated opportunity cost up until the point of selling is the HODL Bank of the market. For interested readers, this opportunity cost can be understood in terms of the BDD metric as explained by this article.

Finally, Reserve Risk is defined as the current price of Bitcoin divided by the HODL Bank described above. It compares the current valuation of BTC against the buyers’ opportunity cost in the market. As Bitcoin’s market value inches closer to the buyers’ opportunity, the asset slowly exits underbought conditions. As this happens, the risk of existing buyers selling their BTC holdings increases and thus there’s a rise in the Reserve Risk metric. When confidence is high and the price is low, the RR ratio is low (below 0.0025), indicating an attractive risk/reward ratio. When the RR is above 0.02, BTC may be overvalued. As shown above, the RR is currently at 0.001, suggesting that current levels present great entry points for long-term investors.

Figure 2: Bitcoin’s Reserve Risk metric shows considerable undervaluation for the asset at current prices

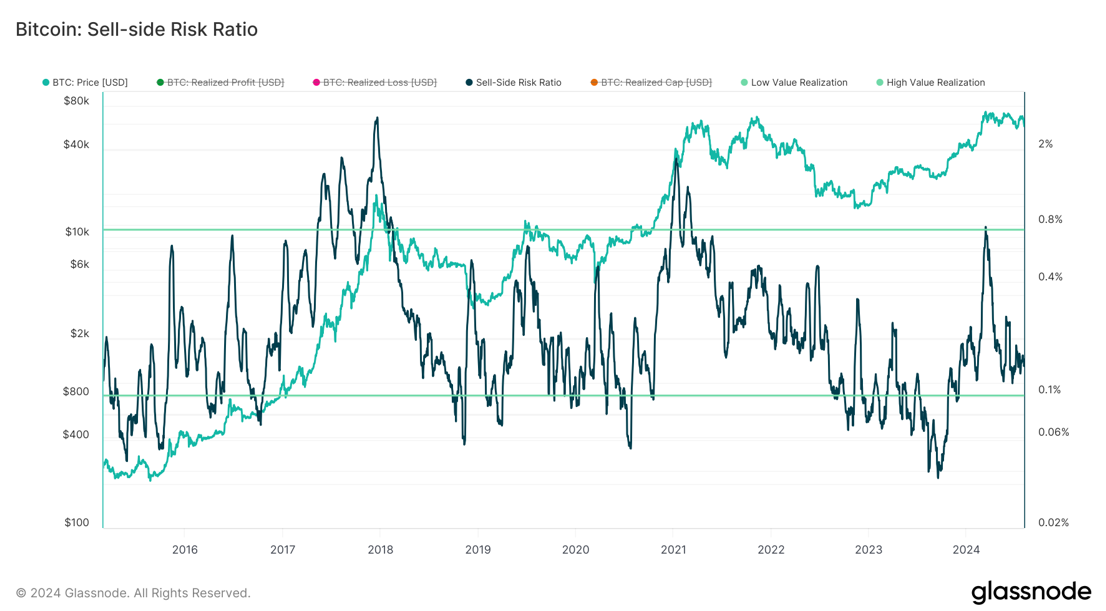

The Sell-Side Risk Ratio measures the potential risk of selling Bitcoin by comparing the total realized profits and losses on-chain to Bitcoin’s realized market capitalization. Realized market capitalization values each Bitcoin transaction based on the price it was last moved, not its current market price. Essentially, this ratio assesses how much investors are spending or realizing in profits and losses each day compared to the total value in Bitcoin transactions they made. By analyzing this, the metric helps quantify the overall risk of selling Bitcoin on the market. Currently, it is at 0.145%, well below the high-risk level of 0.75%. This low value indicates market consolidation, accumulation phases, and a low sell-side risk environment. As such, there is significant potential for BTC to surpass its current all-time high of $73,000 as the market matures.

Figure 3: The Sell-Side Risk Ratio metric indicates that at current levels, it is safe to enter an investment in BTC

Miners’ Status

While current prices are good levels to enter BTC for long-term investors, they are hurting miners. Last week, the Bitcoin network saw a mining difficulty rise of 10%. This combined with the recent drop in prices has now pushed miner revenue per terahash to an all-time low of $0.039, going below $0.04 for the first time in history.

In July, miners earned $951.11 million, the lowest monthly earnings so far this year. This included $24.9 million from on-chain transaction fees, reflecting a continuing trend of low transaction fees within the Bitcoin network. This figure represents a decrease of about $12 million compared to June when miners earned approximately $963.67 million, including $101.25 million from transaction fees. If this downward trend continues with declining Bitcoin prices amidst rising costs, it’s unclear how miners will adapt going forward.

On the derivatives side, Bitcoin’s sharp price correction of over 25% since last week temporarily flipped its 25 Delta Call-Put skew into negative on the front-end of the skew with 25 Delta Put implied vols trading at almost 10%-premium over Calls. Currently, call options with expiries longer than 3 months are trading at a vol premium (1.5-3%). Overall, the Call-Put Skew reflects the increasing demand for hedging the downside. Meanwhile, cumulative open interest in BTC options on Deribit and OKX currently is at $14.5 billion.

Options traders even flocked to bullish bets on BTC for Deribit’s new US election contracts. The options contracts, which expire on November 8 three days after the US Presidential elections, went live on July 18. These call options give buyers the right to buy BTC at a specified price on expiration, they will be in profit (or in-the-money) if BTC is above the strike price at expiration. The highest volume strike for BTC contracts expiring on November 8 was on the $75,000 strike. According to Kaiko, most of these contracts were call options. These bullish bets likely reflect traders growing conviction that the former President will win in November.

Ethereum

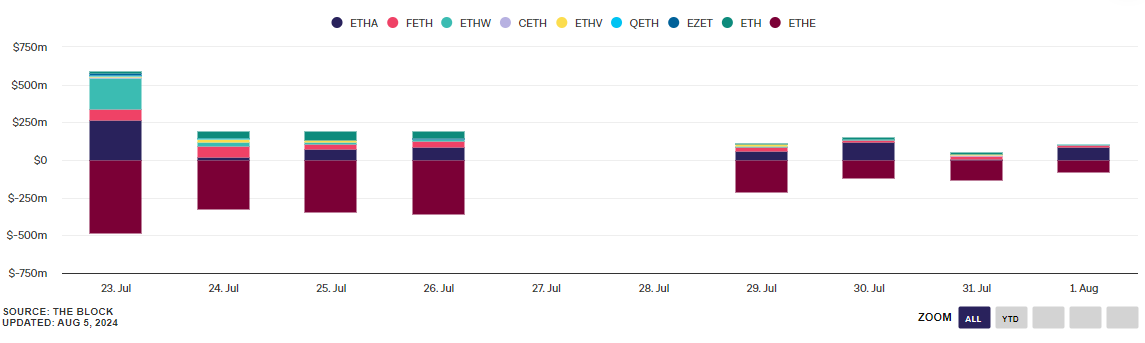

The first few weeks of trading for Ethereum ETFs largely met market expectations. The nine ETFs generated $6.62 billion in total volume and total AUM stands at $8.46 billion at the time of writing. Outflows from Grayscale’s ETHE ETF is down over 80% from initial levels and continue to go down. Meanwhile, BlackRock’s ETHA leads the US spot ETH ETF market with inflows much higher than the rest of the pack.

Figure 4: US Spot ETH ETF Flows

The evolving onchain dynamics show that as the industry matures, ETH is increasingly seen as a utility coin to provide economic security through staking (and restaking) rather than an instrument for speculation. Users are now more engaged in speculating with DeFi coins and other alt-L1s.

On the derivatives side, the 25-Delta Call-Put Skew turned negative for ETH on the front-end of the curve, implying a Put vol premium of up to 17% on 7-day expiries over Calls. Longer-dated expiries of more than 3months are now trading flat in terms of Skew, down from an average of +3.5% Call vol premium over Puts. Currently, ETH’s Call-Put skew mirrors the market’s short-term fear of ETH breaking even lower and the medium-term outlook is less optimistic. Currently, cumulative open interest in ETH options on Deribit and OKX is at $ 4.5 billion.

Like BTC, election dated ETH option contracts saw interest from traders. While volumes were much smaller than the equivalent contracts for BTC they remained very bullish. Most options volume for ETH on this expiry coalesced around strike prices between $4,500 and $6,000.

Aave and Compound Finance

July saw significant events for two of the largest DeFi protocols. The largest DeFi lending platform, Aave, proposed fee revenue sharing with holders of the staked-Aave token on its governance forum. This proposal, if approved, will enhance the utility of the AAVE token beyond governance. Following the release of this proposal, AAVE’s price rose by 10%, reflecting the market’s enthusiasm for its potential implementation.

There was a similar development on Compound Finance orchestrated by the notorious DeFi whale known as Humpy (@Titanium_32 on X). Humpy and his team of collaborators (aka the Golden Boys) attempted to attack Compound’s governance and set up a proposal to direct COMP emissions to some low-liquidity pools. The proposal requested a transfer of 499K COMP tokens (about $24 million) to the team’s own goldCOMP vault. He argued that this was to provide additional yield for COMP holders through a wrapped token called goldCOMP.

However, the proposal gave the Golden Boys’ multi-signature wallet significant control over these funds. The proposal passed by a narrow margin: 682K votes for and 633K against. (Notably, only 57 addresses participated in the vote, highlighting concerns about voter engagement and concentration of power.) The protocol’s security advisor warned this could be considered a governance attack to take funds from the protocol. Soon, Compound Finance and its community scrambled to respond and mitigate potential risks.

Ultimately, after negotiations, the Compound team and Humpy reached a compromise. They agreed that in exchange for withdrawing the proposal, a staking product for COMP token holders would be created to generate yield. This yield would be comprised of 30% of the protocol’s treasury and 30% of its revenues. As a result, COMP is now an interest-bearing token. Shortly after the news of the negotiated terms hit the market, the price of the COMP token rose by 13%.

Good news from the US SEC

On July 30, the US SEC announced it would no longer ask to declare the tokens named in its lawsuit against crypto exchange Binance as securities. These tokens include BNB, Solana, Binance USD, Cardano, Polygon, Cosmos, The Sandbox, Decentraland, Axie Infinity, and Coti. While this development is positive news for the crypto community, the market views it as a politically motivated step, coinciding with presidential candidates’ attempts to win over pro-crypto US voters.

However, some crypto companies continue to face legal battles. For instance, Ethereum software development firm Consensys is fighting allegations of engaging in the unregistered offer and sale of securities through its MetaMask product (a wallet and staking software). Similar allegations have been made against other crypto exchanges, and the case against Coinbase is still ongoing. Uniswap Labs is also battling a case with similar allegations against it.

Conclusion

Bitcoin is holding up relatively well compared to altcoins, even though market sentiment on social platforms like X is low, likely due to many participants being exposed to altcoins while Bitcoin dominance continues to rise. Despite miners facing stress at current prices, promising on-chain metrics suggest a cautiously optimistic outlook for Bitcoin. Anticipated US interest rate cuts and a favorable regulatory environment could strengthen long-term buying for Bitcoin and crypto in general. Additionally, according to Glassnode, the profile of Mt. Gox creditors appears to be like that of long-term investors. This might reduce the impact of sell-side pressure in the coming weeks.

Bitcoin outperformed earlier this year due to rising institutional demand through ETFs and an improved macro environment. While it is unclear if spot ETH ETFs will see the same demand as BTC ETFs, their recent approval in the US could boost ETH’s institutional adoption and increase its short-term correlation with BTC.

We believe it’s important for readers to remember that until fulfilled, pro-crypto promises during US Presidential election campaigns are just that—promises. It’s key to not get carried away by words before we see any development on that front. On-chain, many DeFi protocols are expanding the use cases for their tokens beyond governance, which is positive as it strengthens the investment case for these tokens and attracts more users. The SEC’s decision to back down from labeling many major altcoins as securities is also positive, although it may be politically motivated. Currently, traders are speculating on election-dated option contracts as the US elections approach, and market sentiment for Q4 is bullish on both BTC and ETH. As the possibility of rate cuts gets higher, the market can expect a more risk-on sentiment which can hopefully lead to a recovery in cryptocurrency assets going forward.