AMINA Bank AG

AMINA Bank AG  AMINA UK

AMINA UK  AMINA Hong Kong

AMINA Hong Kong  AMINA EU

AMINA EU Executive Summary

- User adoption and improvement in global macro conditions led to positive price action in the second half of October

- A tight labor market and positive Q3 GDP growth numbers amidst high inflation continue to challenge the Fed

- Money flowed from the US Dollar into other asset classes, with stocks and crypto experiencing some relief

- Bitcoin pushed past the USD 20k psychological level after months of low volatility last month

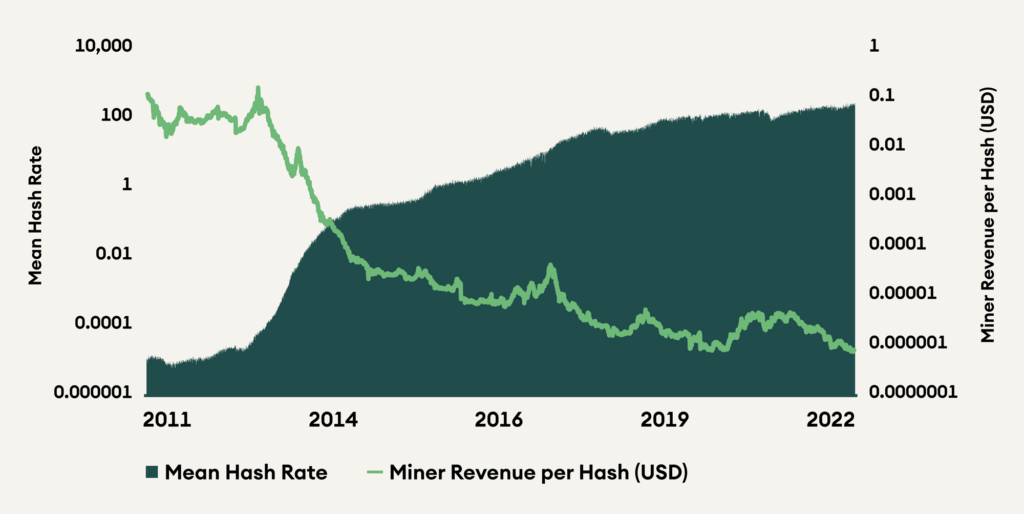

- Bitcoin’s mean hash rate continues to rise while miner revenue is dropping, putting pressure on the miners securing the network

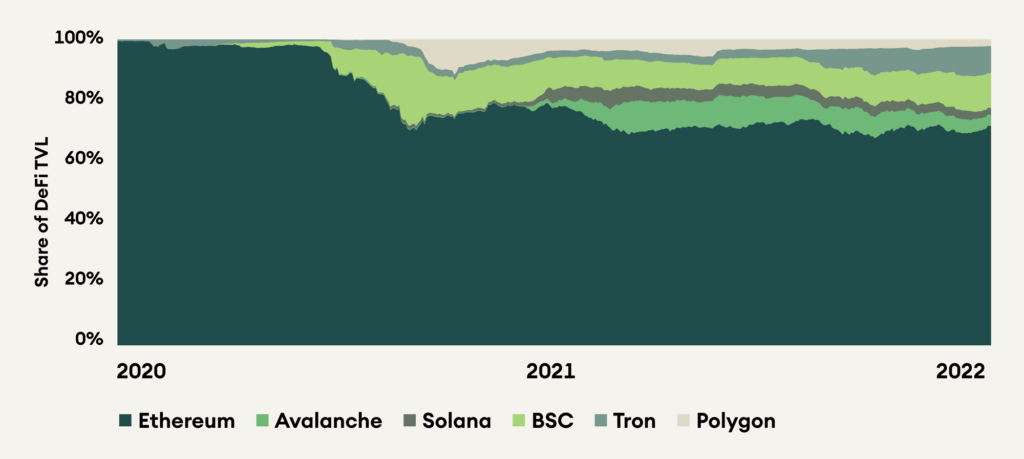

- Ethereum continues to be the leading layer one blockchain and enjoys the lion’s share on defi total value locked

Outlook

October economic data depicts a world torn between high inflation and growth fears with the Ukrainian war in the background. In the financial sector, all these tensions crystallize in the yield curve and then express themselves in various ways, such as dollar strength, equity prices, and cryptocurrencies.

In November 2021, Bitcoin reached an all-time high of USD 67k before sliding into crypto winter. At the time of writing, Bitcoin’s price has just passed the critical USD 20k mark. Bitcoin price declined the day US inflation crossed the 6% mark for the first time in a generation. This historic moment coincided with a dramatic change in the market environment. It marked the end of the zero-interest rate policy and ample liquidity conditions that have been the norm since the Global Financial Crisis.

Since November last year, the yield curve has steepened in anticipation of central bank rate hikes that materialized earlier this year. The most visible impact has been the repricing of major asset classes. We are now at a point where aggressive monetary policy is widely anticipated, though there remains uncertainty about the level interest rates will eventually reach.

The critical question is and remains when the Fed will pivot. As inflation is set to stay above the 2% target in the foreseeable future, it is unlikely the Fed will change its mind on inflation soon.

As we will see in the macroeconomic section below, we have become marginally more constructive as the Fed may have reached peak hawkishness.

Macroeconomics

Macroeconomic uncertainties have come down, though all is not palatable. Turbulent times could be just around the corner with the Fed’s following rate hike announcement in the first week of November. The market is expecting a 75-basis point rate hike. Anything other than this would lead to a pump or a dump, considering the market liquidity increase over the next few weeks. We could witness an unprecedented 1% hike owing to tight conditions in the labour market and the positive Q3 growth in the US.

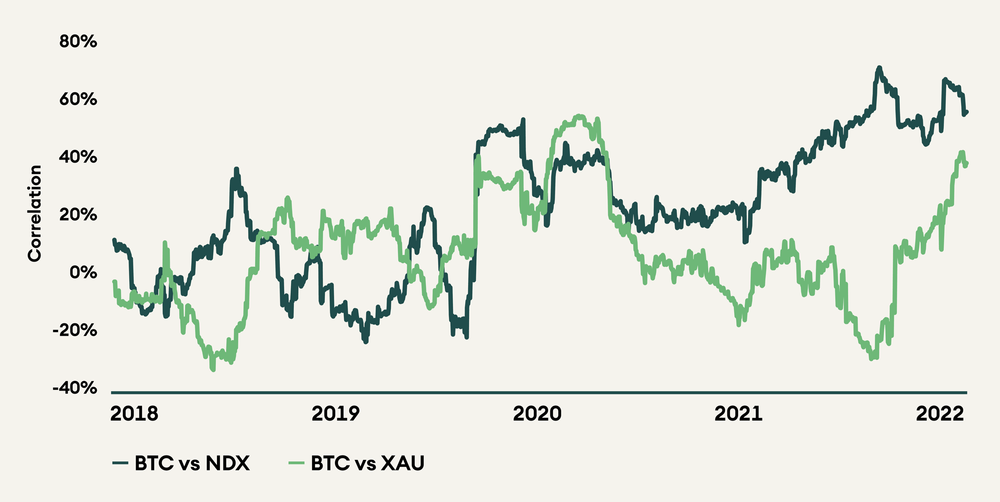

The 3-months correlation between Bitcoin and Nasdaq 100, a tech-heavy index, has retraced below 60% while Bitcoin’s correlation with Gold is elevated.

Figure 1: 3 months Correlation of Bitcoin with Nasdaq (NDX) and Gold (XAU)

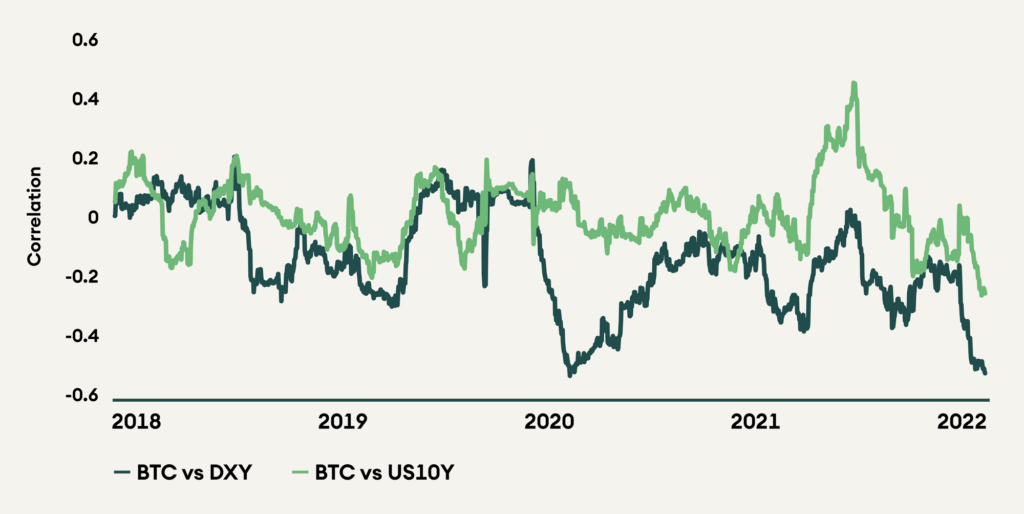

On the other hand, the inverse correlation between Bitcoin and DXY is reaching the levels last seen in 2020, right before the world got infected with COVID and the monetary conditions were extremely tight. Except for the brief period from February to April 2022, Bitcoin remains inversely correlated with US 10Y treasury yields. As the liquidity conditions improve, characterized by a decline in US 10Y rates, the market may change to a more risk-on sentiment.

Figure 2: 3 months Correlation of Bitcoin with DXY (Dollar Index) and US10Y

The DXY has slid down over the past week while stocks and crypto markets have rallied. This move indicates money moving out of the US Dollar into other assets. It reflects the market consensus that the Fed may have passed peak hawkishness.

The highlight of the past week was Elon Musk’s takeover of Twitter. He made a promise to bring free speech to the platform. While signs of development in this regard have started to show on the forum, we are to see how an open social media platform could affect the upcoming midterm elections in the USA. The market expects volatility before and after the election toon 8 November.

On the energy sector front, gasoline prices in the US have not moved. The current administration is pouring reserves from the Strategic Petroleum Reserves (SPR) into the economy, keeping prices artificially low for the time being. However, the situation may change depending on prices once the government eventually stops doing so. Gas prices in Europe, too, have fallen, thanks to the milder-than-expected Autumn. Europeans have not had to heat their homes as much this season, and oil imports continue to flow. This has led to low demand for fuel and a drop in prices. However, Winter is fast approaching, and we are to witness how these prices would change with a colder-than-expected Winter if it does actualize.

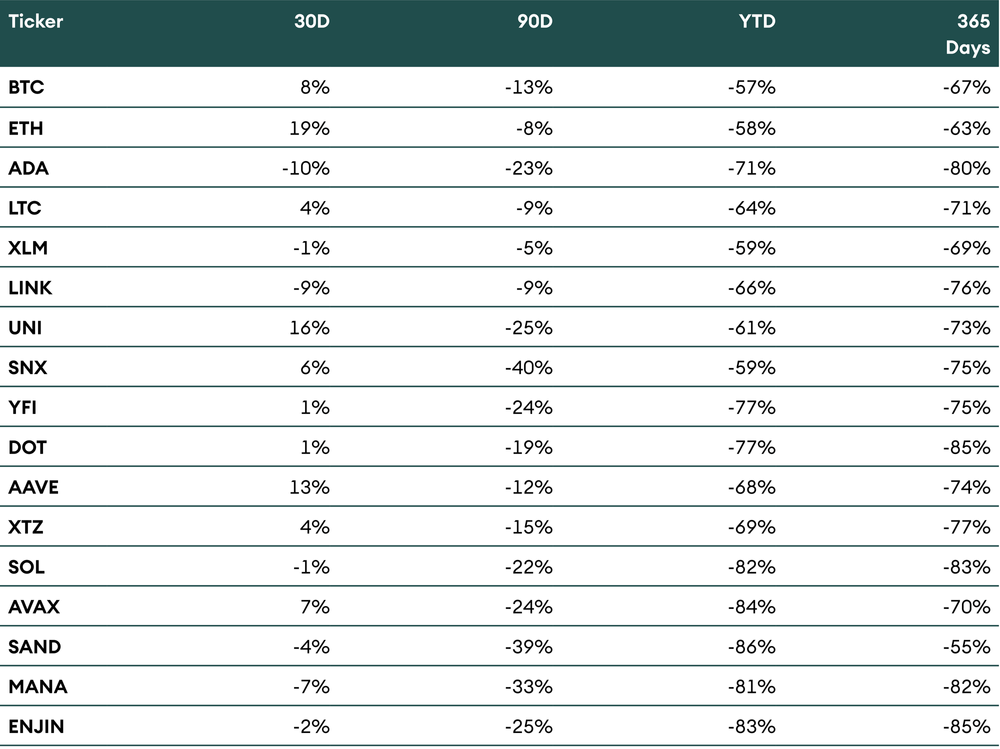

Table 1: Performance of AMINA Bank universe coins as of 1 November 2022

Bitcoin (BTC)

Bitcoin rallied above the USD 20k psychological level early November, and low volatility was low last month. This positive price move has come at the heels of macroeconomic conditions easing up and some institutional adoption.

Digital bank N26 recently announced that they would allow select customers to buy and sell cryptocurrencies on their app – N26 Crypto. In other news, 21Shares, the world’s largest issuer of exchange-traded cryptocurrency products, debuted a Bitcoin ETP in the United Arab Emirates. It started trading on Nasdaq Dubai under the ticker ABTC on 12 October, 2022.

Though Bitcoin experienced some volatility after a relatively stable couple of weeks, the available liquidity seems to be decreasing. Over the past month alone, 0.86% of the total circulating supply of Bitcoin has exited the centralized exchanges. That is a large number, and such behavior is closer to market bottoms. Will the market recover from here, or would we spend more time at these USD 20k levels? Only time will tell. The Lightning Network, however, has seen a decline in activity over the month. The number of nodes and channels in the network has fallen by over 5.5% and 6%, respectively, for October. On-chain activity seems stable, with the Bitcoin hash rate still climbing and miner revenue per hash dropping.

Figure 3 – Bitcoin Mean Hash Rate and Miner Revenue per Hash (USD)

Ethereum (ETH)

With The Merge behind us, things are looking bright for Ethereum. It continues to be the leading layer one smart contract blockchain. It continues to generate the highest revenue among all chains. Rollups have brought customers who previously stayed clear of Ethereum due to its high fees on the main net. Users who once used chains like Avalanche, Polygon, and Solana for their low fees have migrated a portion of their liquidity onto Ethereum rollups like Arbitrum and Optimism. The next upgrade on Ethereum’s roadmap is EIP 4844, also known as Proto-Danksharding. It changes the way data is stored on the blockchain and reduce gas costs further. Ether continues to be the most trusted collateral in crypto. It is also highly integrated into defi protocols, and any major price shock could lead to cascading liquidations.

Figure 4 – Ethereum continues to enjoy the lion’s share of DeFi TVL

Arbitrum One and Optimism continue to be the leading layer two’s on Ethereum. The total value locked in defi on the two continues to increase. Vitalik Buterin, the co-founder of Ethereum, expressed his favor for zero-knowledge technology as more efficient. Many crypto projects have recently announced their zkEVM to be released sometime in 2023. The layer 2 wars have begun, and we could not be more excited.

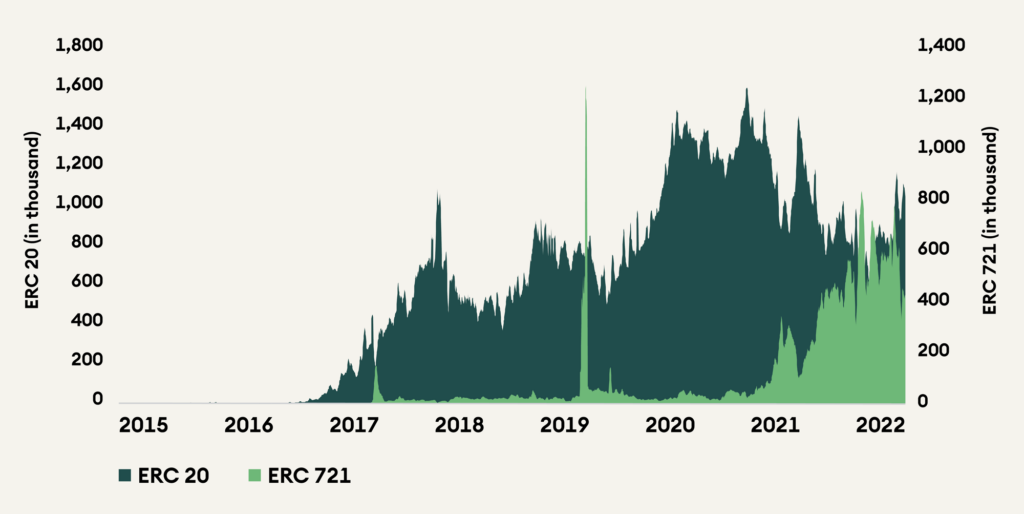

Another strong trend is the increasing share of NFT transactions in the space. NFTs took off in the summer of 2021, and projects like Bored Ape Yacht Club dominated the pack except for some old projects like the CryptoPunks. NFTs have continued to gain institutional adoption as well. Nike made the first significant move in acquiring RTFKT Studios to launch their own set of NFTs for their metaverse. More recently, Reddit launched digital collectible avatars, a top collection on the Polygon blockchain. Interest in NFTs (ERC 721) continues to grow, as evidenced by the share of transactions below.

Figure 5 – Transactions by type over time on Ethereum

Cardano (ADA)

FTX recently announced adding a spot ADA pair on its centralized exchange. This is good news for ADA holders and investors. Cardano NFTs have experienced a gold rush, with trade volumes increasing 120% over the past month. Recently, an Apes Society NFT sold for approximately USD 64K, leading to some traders calling for the next NFT bull run on Cardano.

Avalanche (AVAX)

CME Group has announced plans to launch the AVAX reference rate and real-time indices, which CF Benchmarks will calculate and publish. Investors and traders are watching this since this could soon lead to a CME AVAX futures listing. The Head of Engineering at Ava Labs recently hinted that Avalanche might quickly support the Rust programming language. If Rust were to launch on Avalanche, it would be a game changer for Avalanche, considering the increase in the number of developers open to building on Avalanche. Also, Open Sea recently added support for Avalanche NFTs, which led to a temporary uptick in NFT activity on the network.

Aave (AAVE)

Aave launched a Lido Staked Ethereum (stETH) earn strategy through Oasis, the frontend for borrowing DAI this month, allowing Lido stakers to borrow against their tokens. They can now use stETH as collateral and borrow ETH to participate in DeFi. Aave Companies, one of the contributors developing the Aave protocol, released a technical paper on Aave’s upcoming GHO stablecoin, along with the results of its first security audit, which said that ‘it found no critical bugs’. The stablecoin project was proposed in July and has now come to fruition.

Uniswap (UNI)

Uniswap Labs recently raised USD 165 million in Series B, valuing it at USD 1.6 billion. It has finally achieved “unicorn” status. The community greenlit a proposal to launch the protocol on zkSync. It is expected to go live in the next four to six weeks. Optimism-Uniswap Liquidity Mining Program has kicked off. It will run until 800K OP tokens in incentives run out. This will bring the adoption of Optimism and, despite the temporary token inflation rewards, is a good strategy in the long term.

Polkadot (DOT)

The Polkadot network architecture allows parachains to interoperate with each other, enabling cross-blockchain transfers of any information or asset. A cross-consensus message (XCM) is required to do so, and this has spurred growth within the ecosystem, increasing parachain adoption. In addition to this, parachain auctions continue successfully through this bear market. Each of these auctions leads to locking up more DOT for two years, reducing the DOT supply in circulation. Challenges in front of the team are mainly regarding competition, marketing, and user experience. Cosmos, Avalanche, Polygon, and Solana are the biggest competitors to Polkadot as alternative chains, and they are growing bigger. User experience is probably the most critical concern, and the Polkadot interface is not appealing to many. Chains like Solana and layer 2’s like Arbitrum offer top-notch user experience. If DOT wants to compete in the space, the user experience will need to be a priority for its developers.

Stellar (XLM)

Tildamail is a decentralized email and storage platform that recently integrated with the Stellar Lumens network. This functionality is a step forward in improving technological flexibility concerning cryptocurrencies and makes it easier for users to operate their native XLM coins.

Stellar’s overall network health is not good. The ecosystem’s revenue is about USD 8k a month despite a 200% increase last month.

Looking at the distribution of coins, we observe that the entire locked supply (49% or 24 billion XLM tokens) is controlled by Stellar Foundation, raising severe concerns about its decentralization. These coins were minted at the genesis, and the foundation uses the tokens for the platform’s growth. Notice that the coins do not reward network participation since there is no node operating rewards, and the node count stands at 23.

Solana (SOL)

Solana’s biggest strength is its NFT community, the second largest after Ethereum. SOL price shows a high correlation with ETH despite the very difference in the status of both these currencies. It is surprising as Solana is a new generation blockchain with repeated downtimes, while Ethereum is an established blockchain with a long track record.

Recently, Coinbase announced that users could access Solana Dapps using their Coinbase wallet. This is significant news for the Solana ecosystem and its participants since it reduces network friction.

Solana is known for reliability issues, as many downtimes mark its history. After three months without problems, a new downtime paralyzed the network for 3 hours on 30 September. There are also concerns regarding some applications, as some are closed source, leading to more vulnerability.

Litecoin (LTC)

For Litecoin, there has been a slow and gradual adoption of private transactions, which coincides with the ethos of cryptocurrencies. Also, its price has been close to its historical bottom since 2017. The long-term sustainability of the ecosystem is worrisome as most of the miner rewards on the network come from fresh issuance of USD 4 million per day. To go with this, it also has annual inflation of 3.41%. Both these factors weigh on the coin price.

Tezos (XTZ)

While activity on Tezos remains low, it may be fundamentally strong since it has prominent players validating the network. For instance, 76% of the supply is staked by large validators like Binance, Coinbase, and Kraken.

As on-chain activity is low, a single play-to-earn NFT or gaming application can boost the token’s price due to the increase in daily wallets it would bring with it.

However, there are challenges before the network can grow. For starters, it is not EVM-compatible and so struggles to onboard developers into the space. As a result, the DeFi activity on Tezos is small, only 0.01% of that on non-EVM chains. In addition, whales have been steadily dumping the token, and their holdings are currently at the lowest levels they have been in the past three months.

Chainlink (LINK)

Recently, Chainlink made upgrades for the network and its token holders. Apart from Chainlink 2.0, the major announcement is the collaboration of Chainlink and SWIFT, the international payment backbone of traditional finance. They are developing interoperability standards called CCIP for the Cross Chain Interoperability Protocol. The goal is to use Chainlink to facilitate business interaction and communication across numerous chains by partnering with SWIFT. As a result, trading will be cheaper and faster, increasing further integration with traditional finance.

Staking for LINK tokens was also mentioned by the Chainlink team. The estimated APY on LINK is 5%, and the tentative date for betting LINK tokens is December 2022.

Yearn Finance (YFI)

A cause of worry for YFI is that the realized market capitalization of long-term holders has declined, which may be signaling profit-taking behavior. In the list of liquidity pools with high TVL, Yearn Vaults rank at #92, which is lower than expected since it is considered a top DeFi protocol. Investors in the token need to pay attention since YFI is a low-liquidity token. Low liquidity tokens with higher volatility in subject to sharp price movements.

Synthetix (SNX)

There has been a low demand for SNX products – sUSD and sETH due to a decline in on-chain activity across blockchains. However, adopting perp and futures trading on platforms like Kwenta, 1inch, and Lyra Finance will boost demand for synths, increasing demand for SNX. These platforms could gain more users in the upcoming months since they facilitate trading on synthetic forex tokens, which might look attractive due to the macro environment and the current geopolitical scenario.

Conclusion

In the last seven days alone, daily active addresses, value settled, and overall interactions in crypto have increased due to a week of relief in market prices. The global macro conditions move in cycles, and considering Bitcoin’s correlation to Nasdaq and global liquidity; crypto is behaving like a high beta stock. Though crypto is technically still in a bear market, developer activity has remained strong and this has us excited for the next bull run.