AMINA Bank AG

AMINA Bank AG  AMINA UK

AMINA UK  AMINA Hong Kong

AMINA Hong Kong  AMINA EU

AMINA EU The third quarter of 2025 was a turning point for the cryptocurrency market. Trading activity reached record levels, led by derivatives, which have now become the backbone of the crypto ecosystem. Both centralised and decentralised platforms saw strong growth, and institutional participation continued to expand as clearer regulations and better infrastructure reduced uncertainty. However, this period was also marked by extreme volatility. September brought one of the largest single-day liquidation events in history, testing the resilience of the market and highlighting both the risks and maturity of crypto derivatives.

Perpetual Momentum: Trading Volume and Market Dynamics

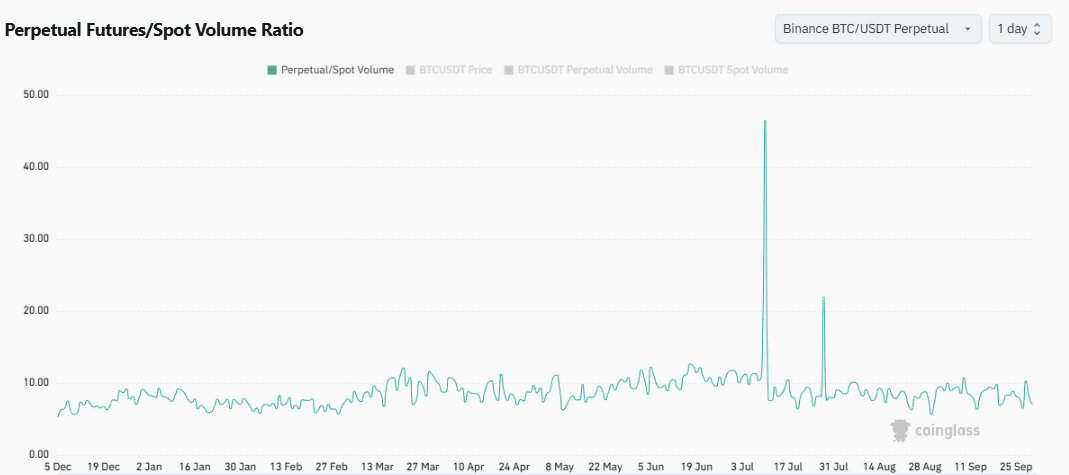

Average daily derivatives volumes reached $24.6 billion in Q3, a 16% increase compared with last year. Perpetual futures continued to dominate, accounting for 78% of trading activity. Their main appeal is uninterrupted exposure, which is especially valuable in crypto’s volatile environment. This preference has persisted for four consecutive quarters. Across every major exchange, derivatives trading once again exceeded spot trading (presently in 5-10x range), showing a trend that began in 2023.

Figure 1: BTC Perpetual Futures/Spot Volume Ratio

Source: Coinglass

The Battle for Market Share: CEXs Hold, DEXs Rise

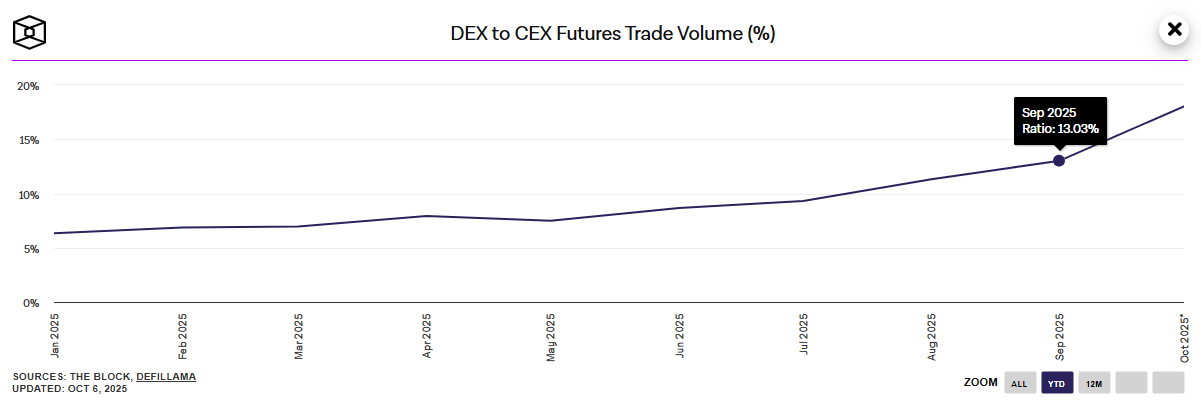

Centralised exchanges continued to lead the market. Binance retained the top position with 35.7% market share and daily volumes above $15.5 billion. Meanwhile, decentralised platforms gained significant traction. The DEX-to-CEX futures volume ratio tripled to 13%, showing that decentralised derivatives are becoming an important part of the market. Hyperliquid emerged as a major player, capturing 73% of DEX derivatives volume with $653 billion in quarterly turnover. This growing parallel ecosystem points to a hybrid market structure where centralised and decentralised platforms coexist.

Figure 2: DEX to CEX Futures Trade Volume (%)

Source: The Block, DefiLlama

Institutions Step Off the Sidelines

Regulatory clarity played a key role in encouraging institutional activity. The September 2025 joint statement from the SEC and CFTC, together with MiCA’s implementation in Europe, reduced operational uncertainty. This coincided with $17.8 billion in net inflows into crypto exchange-traded products during the first half of the year. CME’s derivatives products reflected this trend, reaching record daily volumes of $11.3 billion, a 140% increase year-on-year, while open interest in Bitcoin options climbed to $4 billion by the second quarter. Corporate treasuries also participated, holding 1.07 million BTC and increasing Ethereum holdings nearly 90% in a single month to 4.36 million ETH. These developments show that institutions are not just experimenting with crypto but actively embedding derivatives into treasury and hedging strategies.

September’s Liquidation Cascade

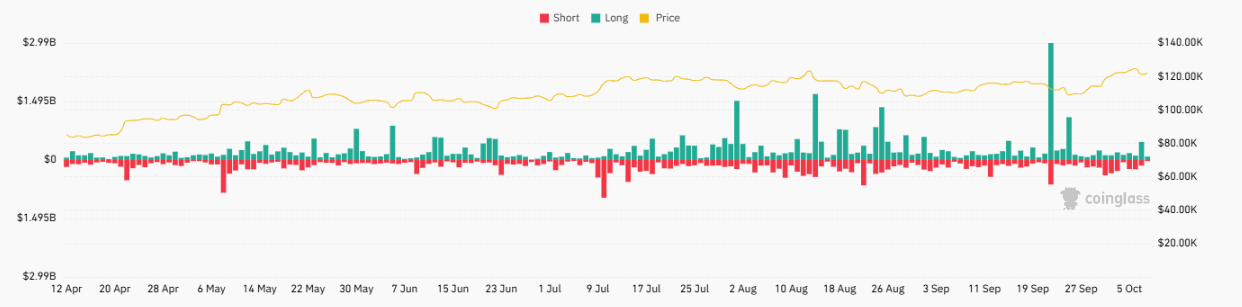

September saw the largest stress event in crypto derivatives history. Within 24 hours, $16.7 billion in positions were liquidated, affecting more than 226,000 traders. Long positions made up 94% of these closures, with Ethereum seeing larger liquidations than Bitcoin. Several factors caused this cascade, including a stronger U.S. dollar, leverage as high as 125 times, thinning liquidity, and ETF outflows that drained $258 million from Bitcoin products alongside $442 million in leveraged liquidations. Prices reacted sharply, with Bitcoin dropping from $124,000 to under $111,000 and Ethereum falling below $4,000. Despite this, historical patterns show that such stress events create conditions for recovery. Between 2022 and 2025, oversold RSI signals below 30 produced 30-day returns averaging 12.4%, and by late September signs of accumulation confirmed the market’s resilience.

Figure 3: Total Crypto Derivatives Liquidations

Source: Coinglass

On-Chain Derivatives: From Niche to Necessity

Decentralised derivatives platforms not only survived the September turmoil but also grew. Aster processed $23 billion in perpetual futures trades by the end of the quarter, and its native token rose over 2,700% since launch. Layer-two solutions and zk-based order books helped overcome latency and cost challenges. Open interest across dYdX and Synthetix reached $1.45 billion, showing that on-chain liquidity has reached a meaningful scale. Decentralised derivatives are now functioning markets with real capital and trust.

Risk and Resilience: Lessons from Leverage

Leverage continued to drive both opportunity and risk. During Q3, 81% of derivatives positions were closed within 24 hours, highlighting the speculative churn in the market. Funding rates also reached extreme levels, with the CF Bitcoin Kraken Perpetual Index at 8.37% annualised in September. In response to the stress event, exchanges began introducing more dynamic funding mechanisms and stricter liquidation thresholds, which may lead to more disciplined risk management going forward.

The Options Renaissance

Options markets expanded in both volume and diversity. Bitcoin and Ethereum accounted for roughly 68% of derivatives activity. On September 26, open interest included 90,000 in-the-money calls and 62,000 out-of-the-money calls. Ethereum options daily volume grew 65% year-on-year in Q2, while altcoin options, particularly Solana and Cardano, saw rising demand. Volatility data confirmed recurring patterns: realised volatility reached historic lows of 20% for Bitcoin, 40% for Ethereum, and 56% for Solana before the September crash. Similar low-volatility periods in 2023 and 2022 preceded major market dislocations, demonstrating the cyclical nature of derivatives markets.

Looking Ahead: From Expansion to Entrenchment

Q3 2025 was a quarter of contrasts, combining record growth with the harshest market stress to date. Together, these forces accelerated the transformation of derivatives markets. Institutions are now entrenched, decentralised platforms are gaining relevance, and exchanges are adjusting leverage frameworks to manage systemic risk. With derivatives now accounting for three-quarters of all crypto trading activity, it is clear that this segment has shifted from being a speculative tool to becoming a defining structure of the digital asset economy.

_________________________________

Disclaimer – Research and Educational Content

This document has been prepared by AMINA Bank Ltd. (“AMINA”) in Switzerland. AMINA is a Swiss licensed bank and securities dealer with its head office and legal domicile in Switzerland. It is authorised and regulated by the Swiss Financial Market Supervisory Authority (“FINMA”).

This document is published solely for educational purposes; it is not an advertisement nor a solicitation or an offer to buy or sell any financial investment or to participate in any particular investment strategy. This document is for publication only on AMINA website, blog, and AMINA social media accounts as permitted by applicable law. It is not directed to, or intended for distribution to or use by, any person or entity who is a citizen or resident of or located in any locality, state, country or other jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation or would subject AMINA to any registration or licensing requirement within such jurisdiction.

Research will initiate, update and cease coverage solely at the discretion of AMINA. This document is based on various sources, incl. AMINA ones, and was generated using artificial intelligence (“AI”). No representation or warranty, either express or implied, is provided in relation to the accuracy, completeness or reliability of the information contained in this document, except with respect to information concerning AMINA. The information is not intended to be a complete statement or summary of the subjects alluded to in the document, whereas general information, financial investments, markets or developments. AMINA does not undertake to update or keep current information. Any statements contained in this document attributed to a third party represent AMINA’s interpretation of the data, information and/or opinions provided by that third party either publicly or through a subscription service, and such use and interpretation have not been reviewed by the third party.

Any formulas, equations, or prices stated in this document are for informational or explanatory purposes only and do not represent valuations for individual investments. There is no representation that any transaction can or could have been affected at those formulas, equations, or prices, and any formula(s), equation(s), or price(s) do not necessarily reflect AMINA’s internal books and records or theoretical model-based valuations and may be based on certain assumptions. Different assumptions by AMINA or any other source may yield substantially different results.

Nothing in this document constitutes a representation that any investment strategy or investment is suitable or appropriate to an investor’s individual circumstances or otherwise constitutes a personal recommendation. Investments involve risks, and investors should exercise prudence and their own judgment in making their investment decisions. Financial investments described in the document may not be eligible for sale in all jurisdictions or to certain categories of investors. Certain services and products are subject to legal restrictions and cannot be offered on an unrestricted basis to certain investors. Recipients are therefore asked to consult the restrictions relating to investments, products or services for further information. Furthermore, recipients may consult their legal/tax advisors should they require any clarifications.

At any time, investment decisions (including, among others, deposit, buy, sell or hold investments) made by AMINA and its employees may differ from or be contrary to the opinions expressed in AMINA research publications.

This document may not be reproduced, or copies circulated without prior authority of AMINA. Unless otherwise agreed in writing, AMINA expressly prohibits the distribution and transfer of this document to third parties for any reason. AMINA accepts no liability whatsoever for any claims or lawsuits from any third parties arising from the use or distribution of this document.

©AMINA, Kolinplatz 15, 6300 Zug