AMINA Bank AG

AMINA Bank AG  AMINA UK

AMINA UK  AMINA Hong Kong

AMINA Hong Kong  AMINA EU

AMINA EU Executive Summary

- Real-world asset (RWA) tokenisation converts tangible assets like real estate, gold, and treasuries into blockchain-native tokens with built-in Know Your Customer (KYC), custody and compliance.

- Major institutions, including BlackRock, JPMorgan and Visa are driving adoption alongside crypto-native protocols like Ondo and Centrifuge.

- Ethereum, Solana and Avalanche provide the mature infrastructure needed to issue tokenised assets, ensuring scalability and security.

- RWA platforms currently hold over $10 billion in value, excluding stablecoins with BlackRock’s BUIDL fund leading the way at approximately $1.95 billion. For now, there is more clarity on the global regulations concerning RWAs. Europe has introduced Markets in Crypto-Assets (MiCA), while in the US, the Securities and Exchange Commission (SEC) and the Financial Crimes Enforcement Network (FinCEN) continue to refine oversight. Asia and the Middle East are establishing innovation hubs with progressive frameworks.

- RWA infrastructure is maturing with advances in blockchain tech, enabling deeper integration with decentralised finance (DeFi).

- What’s next? The markets are evolving in a way that may support an evolution toward tokenised Exchange-Traded Funds (ETFs), bonds and real-world collateral that can be natively used in DeFi ecosystems in the foreseeable future.

What if you could buy real estate like buying Bitcoin?

Imagine owning a slice of a luxury villa in Bali, a share of gold in a Zurich-based vault or exposure to U.S. Treasuries – all from your phone, in minutes, no broker required. That’s the promise of RWA tokenisation.

Once reserved for institutional giants and high-net-worth individuals, assets like real estate, bonds and commodities are now being transformed into blockchain-based tokens, making them globally accessible, available 24/7 and instantly liquid.

Real-world assets (RWAs) are quickly becoming a foundational pillar of blockchain adoption, driving the convergence of traditional finance and decentralised infrastructure. What was once a niche seems to be becoming central to the future of global capital markets. Institutions like BlackRock, HSBC and JPMorgan are now actively exploring blockchain infrastructure to tokenise a broad range of assets, from US Treasuries to private credit markets. Governments, too, are joining in: Hong Kong’s Monetary Authority issued tokenised green bonds on-chain; Singapore’s Project Guardian is piloting tokenised government securities; and the UK’s Debt Management Office has explored blockchain-based settlement for sovereign debt instruments.

Meanwhile, crypto-native platforms like Ondo Finance and Centrifuge are pushing the boundaries of innovation. They’re building specialized protocols that allow users to invest in tokenised debt -essentially lending in a digitised, transparent format -and yield-generating assets that offer the potential for compounding returns, all without traditional financial intermediaries.

But how did we get here and where is this all heading? Let’s explore the evolution of RWA tokenisation, the technology driving it, the regulatory frameworks taking shape and why this trend could unlock one of the biggest shifts in global finance this decade.

How we got here: The Evolution of RWA Tokenisation

The Spark: Early Experiments (2015 to 2018)

Tokenising RWAs began as a bold idea: what if physical assets could be represented on a blockchain? Early pioneers like Digix launched gold-backed tokens on Ethereum. Projects like Harbor and Polymath started building tokenised securities that acted as digital shares of real-world companies.

In 2018, a Manhattan condo was tokenised on Ethereum. Investors could now buy fractional ownership in real estate through blockchain. This proved that tokenisation was no longer just theoretical.

Building Momentum: From Real Estate to Debt (2019 to 2020)

By 2019, platforms were enabling ownership of small amounts of a broad range of assets from property to invoices. Simultaneously, institutions began testing tokenised corporate bonds. The narrative began to shift from “what if” to “what next?”

DeFi’s rise in 2020 accelerated this shift. Tokenised assets could now be used as collateral in lending, integrated into yield strategies and traded 24/7. RWAs became active components of decentralised ecosystems.

When Tech Started to Catch Up (2021 to 2022)

Blockchain trailblazers like Solana helped in advancing this concept further. Smart contracts automated ownership and payouts. Oracles like Chainlink provided real-time pricing. Institutional custody solutions improved trust. RWA tokenisation evolved from concept to robust financial product.

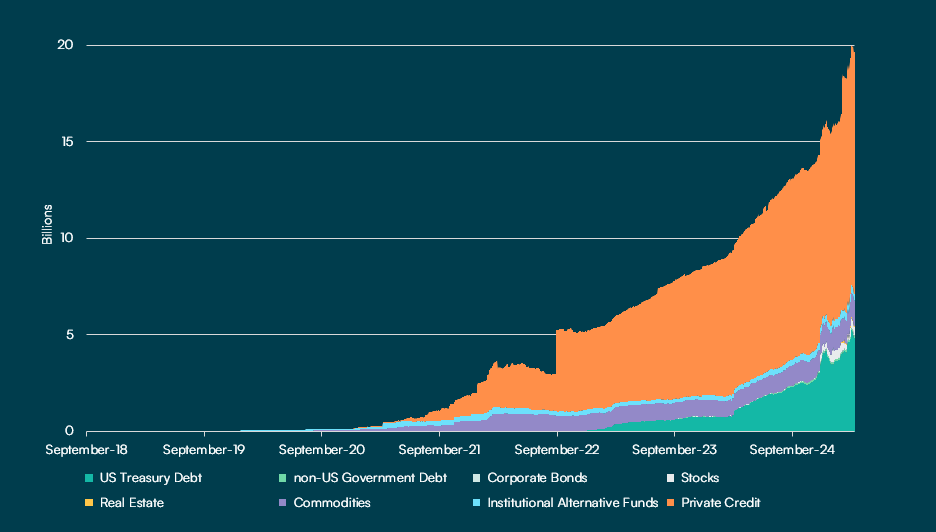

Figure 1: RWA Tokenisation Growth (by asset type)

Source: RWA.xyz, AMINA Bank (31 March 2025)

How it works: Turning Real-World Assets into Tokens

The first step is identifying an asset, such as property, commodities, credit portfolios or sovereign bonds. Legal checks and valuations are performed upfront.

The asset is broken into various pieces like digital tokens, each representing ownership. These are minted on blockchains like Ethereum, Solana or , chosen based on speed, cost and compliance features.

Compliance is required from the get-go. Investors must complete KYC and AML checks. Licensed custodians safeguard the assets. Smart contracts automate ownership, payouts and collateralisation.

Once issued, RWA tokens can trade on centralised and decentralised platforms. Some list on regulated exchanges. Others integrate into DeFi. Investors may earn passive income via rent, interest or DeFi yields.

The New Market Landscape: Key Players and Emerging Trends

Protocols and platforms are driving the RWA revolution across verticals. Ondo Finance operates a protocol that tokenises US Treasuries, bringing fixed-income exposure to the blockchain. Centrifuge is transforming private credit markets by enabling loans and invoices backed by real-world assets. Maple Finance is opening access to tokenised private credit in decentralized markets.

BlackRock’s BUIDL fund, which tokenises short-term Treasuries on Ethereum, underscores how seriously certain institutions are approaching this space.

Traditional finance isn’t far behind. Franklin Templeton and WisdomTree have launched tokenised funds, JPMorgan is piloting on-chain collateral and Visa is exploring how tokenised yields can be integrated into payment systems.

Real-world assets now sit at the intersection of TradFi and DeFi – offering liquidity, transparency and programmable ownership like never before.

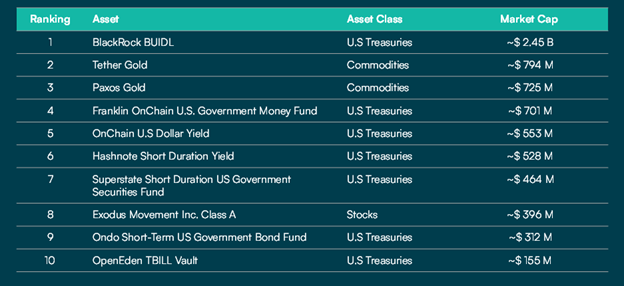

Figure 2: Top 10 Tokenised Assets by Market Cap

Source: AMINA Bank, RWA.xyz (14 April 2025)

Metrics that Matter

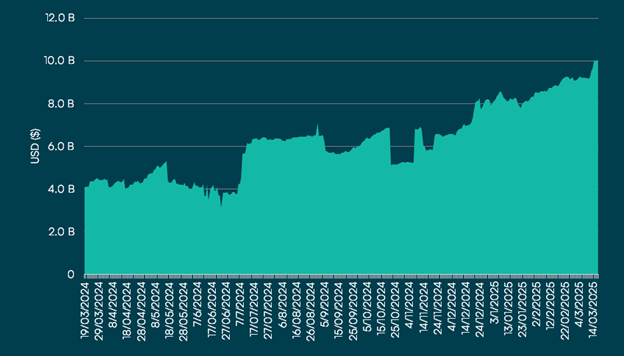

As of March 2025, real-world asset (RWA) protocols have reached an all-time high, with over $10 billion locked. Secondary market activity is gaining momentum, fueled by growing investor confidence and increasing cross-platform compatibility.

Meanwhile, yield strategies are rapidly evolving. Tokenised assets are now more deeply integrated into DeFi ecosystems, enabling investors to pursue enhanced returns without relying on traditional financial intermediaries.

Figure 3: Real-World Asset Sector Total Value Locked (TVL) Growth

Source: DefiLlama, AMINA Bank (15 March 2025)

Regulatory Roadblocks and Compliance Hurdles

Despite the momentum, legal and regulatory considerations remain. Know Your Customer (KYC) and Anti-Money Laundering (AML) regulations are mandatory in most jurisdictions. In the US, the SEC and FinCEN require platforms to follow identity verification rules. December 2024, brings harmonised digital asset regulation to the region. Singapore and the UAE lead with innovation-friendly policies while maintaining rigorous compliance.

However, the classification of tokenised assets remains complex. The US applies the Howey Test, often classifying Real-World Assets (RWAs) as securities. Switzerland takes a . Regulations remain fragmented, with Europe taking the lead on MiCA, while Asia and the Middle East drive innovation in RWA-specific developments.

The Road Ahead: What’s Next for Tokenisation?

The infrastructure for tokenisation is now established, with institutions actively engaged and regulations steadily evolving to keep pace. In the coming years, trillions of dollars in real-world assets could move on-chain, with tokenised treasuries, real estate and commodities integrating into DeFi. Enhanced interoperability will make these assets easily transferable across blockchains and borders.

Imagine a bond minted on Ethereum, used as collateral on Solana. A Singapore real estate token rehypothecated under Swiss law. Legal and technical convergence could redefine global finance. On-chain identity and KYC standards will streamline compliance. We may see tokenised ETFs and structured products inside everyday finance apps.

Conclusion: The Future of Finance Is Onchain

RWA tokenisation is more than a crypto use case. It’s a shift in how value is created, transferred, and accessed. By merging DeFi’s flexibility with traditional finance’s trust, tokenised assets could become as common as ETFs or bonds. For both retail and institutional investors, the age of RWA tokenisation may not just be near – it’s arguably already here and it’s just getting started.

—

Disclaimer – Research

This document has been prepared by AMINA Bank AG (“AMINA”) in Switzerland. AMINA is a Swiss bank and securities dealer with its head office and legal domicile in Switzerland. It is authorized and regulated by the Swiss Financial Market Supervisory Authority (FINMA).

This document is published solely for educational purposes; it is not an advertisement nor is it a solicitation or an offer to buy or sell any financial investment or to participate in any particular investment strategy. This document is for distribution only under such circumstances as may be permitted by applicable law. It is not directed to, or intended for distribution to or use by, any person or entity who is a citizen or resident of or located in any locality, state, country or other jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation or would subject AMINA to any registration or licensing requirement within such jurisdiction.

No representation or warranty, either express or implied, is provided in relation to the accuracy, completeness or reliability of the information contained in this document, except with respect to information concerning AMINA. The information is not intended to be a complete statement or summary of the financial investments, markets or developments referred to in the document. AMINA does not undertake to update or keep current the information. Any statements contained in this document attributed to a third party represent AMINA’s interpretation of the data, information and/or opinions provided by that third party either publicly or through a subscription service, and such use and interpretation have not been reviewed by the third party.

Any prices stated in this document are for information purposes only and do not represent valuations for individual investments. There is no representation that any transaction can or could have been effected at those prices, and any price(s) do not necessarily reflect AMINA’s internal books and records or theoretical model-based valuations and may be based on certain assumptions. Different assumptions by AMINA or any other source may yield substantially different results.

Nothing in this document constitutes a representation that any investment strategy or investment is suitable or appropriate to an investor’s individual circumstances or otherwise constitutes a personal recommendation. Investments involve risks, and investors should exercise prudence and their own judgment in making their investment decisions. Financial investments described in the document may not be eligible for sale in all jurisdictions or to certain categories of investors. Certain services and products are subject to legal restrictions and cannot be offered on an unrestricted basis to certain investors. Recipients are therefore asked to consult the restrictions relating to investments, products or services for further information. Furthermore, recipients may consult their legal/tax advisors should they require any clarifications.

At any time, investment decisions (including whether to buy, sell or hold investments) made by AMINA and its employees may differ from or be contrary to the opinions expressed in AMINA research publications.

This document may not be reproduced, or copies circulated without prior authority of AMINA. Unless otherwise agreed in writing AMINA expressly prohibits the distribution and transfer of this document to third parties for any reason. AMINA accepts no liability whatsoever for any claims or lawsuits from any third parties arising from the use or distribution of this document.

Research will initiate, update and cease coverage solely at the discretion of AMINA. The information contained in this document is based on numerous assumptions. Different assumptions could result in materially different results. AMINA may use research input provided by analysts employed by its affiliate B&B Analytics Private Limited, Mumbai. The analyst(s) responsible for the preparation of this document may interact with trading desk personnel, sales personnel and other parties for the purpose of gathering, applying and interpreting market information. The compensation of the analyst who prepared this document is determined exclusively by AMINA.