AMINA Bank AG

AMINA Bank AG  AMINA UK

AMINA UK  AMINA Hong Kong

AMINA Hong Kong  AMINA EU

AMINA EU Executive Summary

Last month, digital assets and equities did well. Bitcoin price increased by 22%, ether by 38%, and the Decentralised Finance (DeFi) token AAVE jumped as much as 100%.

The current high inflation scenario is expected to continue, given geopolitical uncertainty and high prices for energy and commodities. If the supply bottlenecks continue, high inflation may weigh on consumption and reduce growth.

In these uncertain times, important developments in the crypto ecosystem continue to move forward. Russia is considering bitcoin as a means of payment for its energy exports, major oil and gas company, Exxon Mobil, and some of the world’s most prominent asset managers (Fidelity, Goldman Sachs, Morgan Stanley, and BlackRock) have started experimenting with bitcoin. The Luna foundation has started acquiring bitcoin with the goal of a total of USD 10 billion worth of bitcoin reserves over time.

Ethereum development is in line with the latest roadmap. The community expects “The Merge” to be completed at the end of Q2 2022 when Ethereum shifts its consensus mechanism from Proof-of-Work (PoW) to Proof-of-Stake (PoS) . “The Merge” was successful on the first public testnet, Kiln. Ethereum captures most of the DeFi and Non-Fungible Token (NFT) activity. It continues to grow with new NFT/metaverse projects and continuous innovation in the DeFi space.

Bitcoin’s scaling solution, the Lightning network, is gaining more users in the larger crypto ecosystem and has added more features to this layer. Solana continues to be the most popular blockchain for Decentralised Applications (DApps) after Ethereum, touching almost USD 1 billion in NFT trading volume last month. After five years of conception, Polkadot has finally deployed the first batch of 14 parachains on the network with more than USD 2 billion of value locked in the ecosystem. Avalanche announced a Bitcoin bridge during their summit in the last week of March, along with new partnerships with Coinbase and Terra.

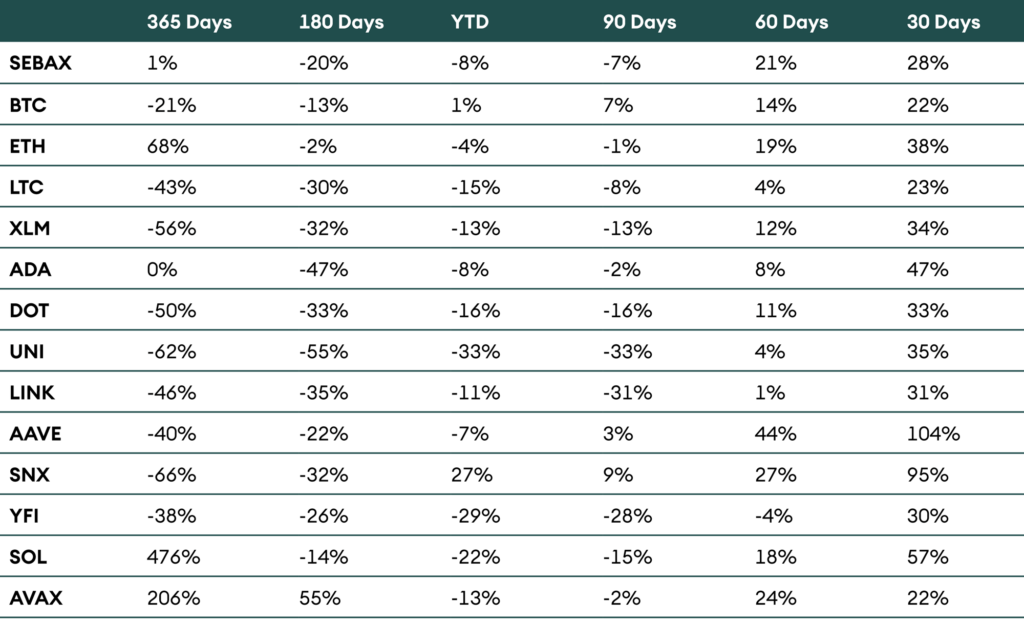

Table 1: Performance of AMINAX and AMINA coin universe assets as of 4th April 2022

Introduction

The main drivers of traditional and digital financial markets have essentially been the same last month. The development of the war in Ukraine and the Fed’s 25 basis point hike in mid-March have been the major events.

The second half of the month contrasts with the first half. The Ukrainians have shown strong resistance and slowed down the advance of the Russian troops. The West welcomed this development, which led to an improvement in risky assets. The possibility of a war spreading across the European continent faded. The VIX index and oil price fell.

However, the war is not over yet, and the outcome remains uncertain. We see two possible scenarios. The first is a rapid end to the hostilities in a few weeks or months, following an agreement between Russia and Ukraine. The second scenario is a stalemate that marks the beginning a long war of attrition.

We think the first scenario has a lower probability. In the second scenario that we consider more likely, uncertainty will remain high and inflation will rise. In addition to the high energy prices, we expect wheat prices to increase further, of which both Russia and Ukraine are top producers. Ukraine’s upcoming grain harvest is expected to be low as farmers are fighting for their country, fuel and fertilizers are not available, and the transport of grain across the black sea is no longer possible as the Bosphorus straight is close. While Russia can still produce wheat, sanctions will prevent most countries from buying them.

Growth is likely to falter due to persistent supply shock inflation, as consumption gets affected. If this scenario materializes, central banks will find themselves stuck between a rock and a hard place as hiking further will primarily slow down the economy without curbing much inflation.

Another consequence of this scenario will be that payment systems will become even more restricted. The EU has already banned several Russian banks from the SWIFT international payment system. We know that Russia and China have started building their own systems in the mid-2010s to reduce their dependency on the US dollar.

In this context, the March 2022 Executive Order on Ensuring Responsible Development of Digital Assets signed by POTUS Joe Biden shows how digital assets have become an essential element of geopolitics.

As far as digital assets are concerned, the current murky environment is conducive to it. War is an expression of trust failure, and geopolitics is an expression of ideological power struggle. The blockchain is a fabric of trust, independent of ideologies. As Vitalik Buterin reminded us: “Ethereum is neutral, but I am not.”

Blockchain is a bastion of trust, and cryptocurrencies are the vehicles to record, transfer, and hold values, whether means of payments, non-fungible assets, or contractual rights.

As we will see in the rest of this report, on-chain fundamentals have remained strong despite the long decline in digital asset prices since the all-time highs in November last year. In addition to the strength in fundamentals, many innovations are on the cusp of being implemented, offering a cheaper and faster environment to build new and improve existing decentralised applications.”The Merge” is a singularity in the life of Ethereum; it is the moment the old PoW Ethereum will become the new PoS Ethereum 2.0 network, offering scalability and a drastic reduction in energy consumption, and a few new features.

Bitcoin

The crypto market mainly moved sideways in March 2022, except last week. From February until the last weekend of March, the bitcoin price had been between USD 37,500 and USD 42,500. Given the macro landscape, this was surprising. Bitcoin and other digital assets started rallying upwards only after 16 March, when the Fed announced rate hikes, much in line with market expectations. Bitcoin broke the USD 40,000 resistance level and has gained 18%.

The Luna Foundation Guard (LFG) announced its plan to buy up to USD 10 billion worth of bitcoin to back its stable coin TerraUSD (UST). The persistent bitcoin purchases by LFG have proved to be a near-term tailwind for the bitcoin price.

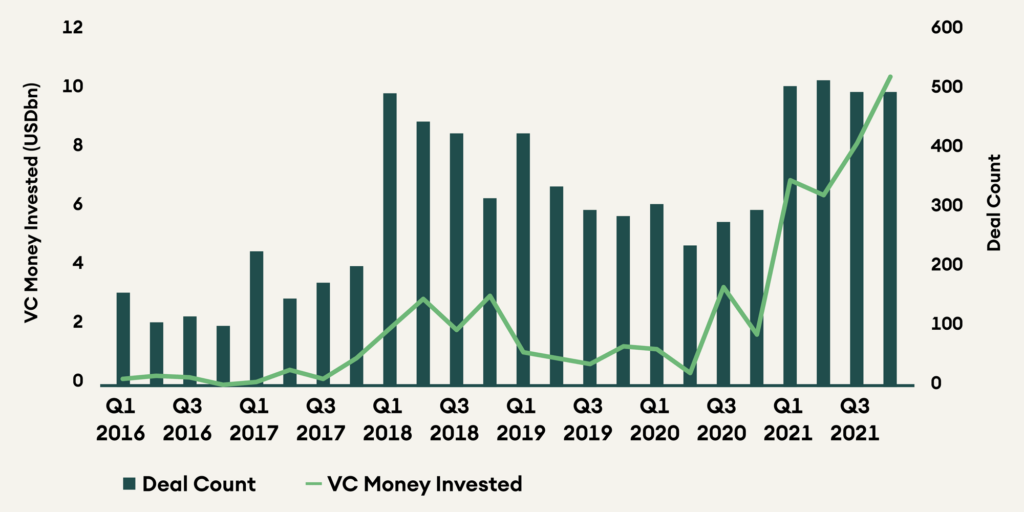

The understanding and interest in crypto are also growing. Institutional investors traded USD 1.14 trillion worth of crypto via Coinbase alone in 2021, 10 times the amount in 2020. One report estimates that 80% of institutions are now allowed to allocate to crypto. According to Fidelity, 70% of institutional investors plan to buy digital assets soon, while a survey from Nickel Digital Asset Management says it’s more like 80%. Understanding leads to action. Institutions are pouring money into the space.

Figure 1: Venture Capital Investment in blockchain/crypto projects/companies over the years

Ethereum

Bitcoin isn’t the only asset investors like. The market favoured ether (ETH) compared to bitcoin (BTC), with ETH gaining 34% since the Fed announcement. Ether’s price catalyst came on 14 March when Ethereum successfully “merged” on the Kiln testnet ahead of the blockchain’s eventual move to PoS. Ethereum’s move toward being a more energy-efficient and faster blockchain started in 2017, and it took a long time to achieve this goal.

Post merge, the tokenomics will be adjusted as well, with massive implications on the supply. ETH daily issuance will fall by 90%. Currently approx. 12,000 ETH are paid daily to PoW miners, creating a significant selling pressure as ETH are exchanged for fiat currencies to cover electricity costs. After Ethereum transitions to PoS, approx. 1,280 ETH will be issued to validators. A fall in daily issuance coupled with ETH burning (due to the burning of transaction fees) will make Ethereum a deflationary asset, giving it the status of ‘ultrasound money.’

With more than 2 million ETH burned, 11 million ETH locked in Ethereum 2.0, and more than 30 million ETH locked in smart contracts, there is enormous demand for ether tokens and a shrinking supply.

Some commentators also suggest that it might even lift the coin’s market cap above bitcoin’s as more institutional investors buy-in. According to some crypto evangelists, Ethereum will overtake bitcoin in market cap; it’s not a question of ‘if’ but ‘when.’

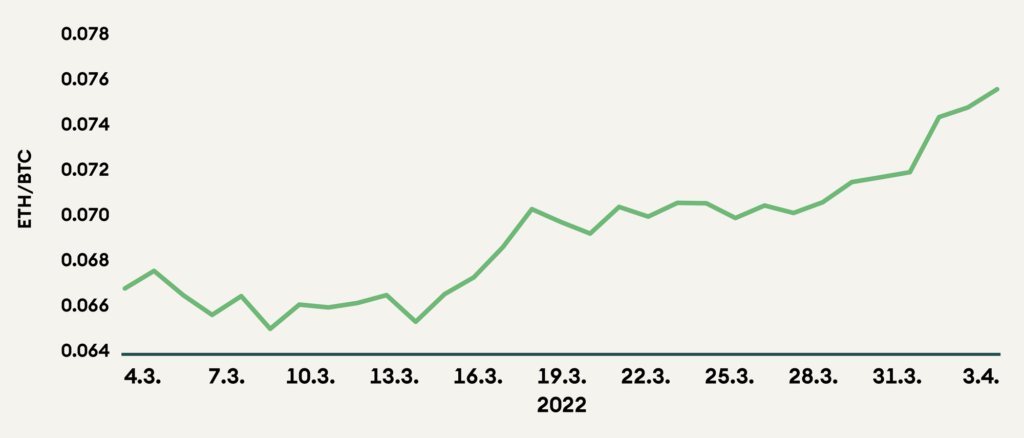

Below we look at ETH/BTC ratio, and as can be seen, post Kiln testnet merge, the ratio has reversed.

Figure 2: ETH/BTC Ratio

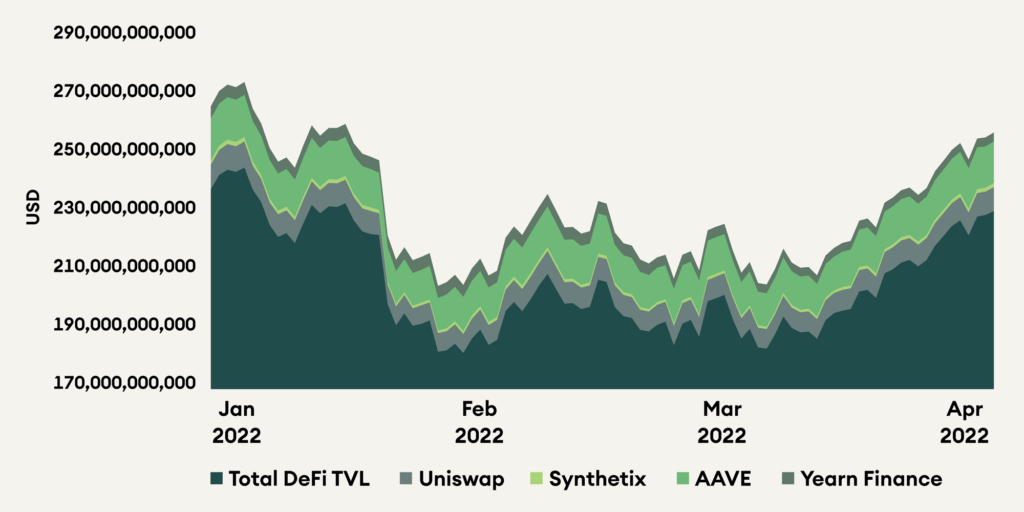

In March, activity on all platform chains declined, including Ethereum. NFT trading volumes shrank by 50% from their ATH of USD 5 billion on OpenSea in January 2022. The total value locked (TVL), a metric of Decentralised Finance (DeFi) activity, also contracted by 16% from its ATH of USD 236 billion in November, only to recover in the last week of March.

Alternative Blockchains

Bitcoin scaling solution, the lightning network, saw a spike in its daily active addresses in the past few days. This is attributed to significant developments on the network. Synonym, a Bitcoin company, sent the first stable coin transaction on the lightning network. This will bring a host of other tokens to the network and provide a better use case for its users.

Polkadot’s first 14 parachains are now live. Five years after conception, Polkadot successfully completed its multistage launch of parachains. The first 14 parachains bonded 126 million DOT (11% of the total supply, worth USD 2.1 billion) for the two-year lease periods. With the parachains live and funding secured, the fruits of developers’ labour are finally accessible to the masses. Each parachain brings unique functionality and use cases to the Polkadot ecosystem.

Cardano is seeing tremendous growth in demand from institutional investors. The trading volume on Cardano’s blockchain rose by 13x just in 2022. Although the active addresses and transaction counts remain the same over the past three months, the mean transaction size has grown manifold. ADA (the native coin of the Cardano blockchain) has been among the best-performing assets in the last few weeks as it gained 47% for its investors.

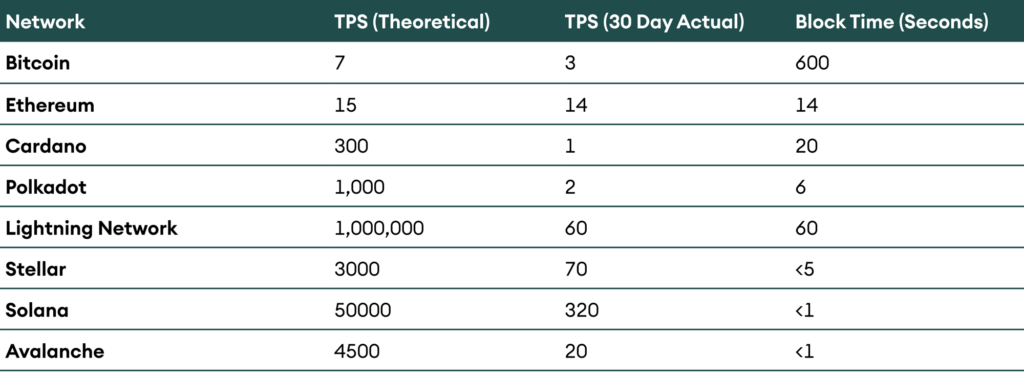

Table 2: Transaction speed comparison of different blockchains

Solana is the new second favorite blockchain for NFT traders. Its native NFT marketplace, Magic Eden and Solanart, clocks in more than 200K monthly traders and nearly USD 1 billion in trading volume. SOL, the Solana cryptocurrency, continued its two-week uptrend and passed USD 120, a critical resistance level. SOL’s price catalyst came from OpenSea integrating Solana’s NFTs and, Coinbase wallet adding support for Solana and Solana-based tokens.

Avalanche concluded its summit in Barcelona, Spain, on 22-27 March 2022. Many exciting announcements were made during the summit, like the Avalanche bridge that connects to the Bitcoin network to facilitate the usage of its DeFi applications by bitcoin holders. Team also announced a new partnership with Terra Luna and Coinbase. The prime catalyst of AVAX’s run to USD 100 is its incentive program, Rush of USD 290 million, which boosts liquidity in its DeFi applications and 70,000 daily active users of its novel blockchain.

Stellar is a blockchain focusing on cross-border payments and remittances. Although the trading volume and active addresses continue to rise on the Stellar blockchain, Lumen (XLM), its native token, has not reached its ATH of USD 0.87 made in January 2018, which may deter wider adoption.

Decentralised Finance (DeFi)

More than 100,000 new users are coming to explore DeFi every month. But the growth rate in terms of month-on-month percentage is slowing compared to 2020 and early 2021. This can be attributed to the steep learning curve required to get involved in the DeFi ecosystem, along with the not-so-successful narrative of DeFi 2.0 and the rise of NFTs in 2021.

Total value locked (TVL) is one of the key metrics used to evaluate the DeFi ecosystem. It moves in parallel with the price of protocol tokens that provide liquidity for the efficient functioning of decentralised applications (DApps). With the downfall of overall crypto markets in November 2021, DeFi tokens took a huge hit, and some lost more than 50% of their value. However, on the flip side, since the market has been up last month, DeFi tokens significantly outperform leading crypto assets such as bitcoin and ether.

Figure 3: Total Value Locked (TVL) in different DeFi protocols since January 2022

Chainlink continues to be the number one decentralised oracle network that brings real-world data onto blockchain networks. Over the past month, Chainlink has had 17 new integrations across five different chains – BNB, Solana, Polygon, Ethereum, and Arbitrum. These new integrations and the overall market uptrend are the catalysts for Link’s price action. The real game-changer for Link holders will be Chainlink 2.0, which will improve its token economics and is expected to be launched sometime in 2022.

Uniswap continues to be the Top Decentralised Exchange (DEX) on the Ethereum blockchain, with more than 85% of all exchange volume concentrated on its DApp. Though highly concentrated in the hands of large holders, the UNI token stood well below its ATH of USD 42 in May 2021. Turning on the fee switch that gives UNI holders a share of the protocol’s revenue will certainly change investors’ sentiments and should lead to a rally in the token price. It remains to be seen when that happens.

Synthetix saw a major upgrade last month with its pool merge of Ethereum and Optimism debt pools to enhance liquidity on the protocol. This upgrade and the launch of Ethereum futures trading on the platform led to an 80% price jump in SNX.

Aave took the most significant step in taking DeFi mainstream with the launch of the Aave V3. Aave V3 brings a host of improvements for Aave users, better yield on their investments, and more governance power to its holders. The launch has been a significant catalyst in its price rally to USD 224 from USD 124, an approx. – 100% gain.

Yearn Finance has been the DeFi underdog for most of 2021-22. Its founder, Andre Cronje, famously left crypto, and YFI’s initial fame of USD 73,000 wore thin over the year. Its competitors like Convex and Cream finance stole its limelight while Yearn team continued to work and develop their product in the background. Through the pure genius of its talented team and developers, Yearn continues to survive the many shocks it has seen over the past year. YFI token increased by 25% in the last month, owing to its buyback plan (as a form of dividend) to incentivize holders.

Conclusion

In March, the crypto market survived the geopolitical stress test and performed better than other asset classes. The EO (Executive Order) signed by the POTUS also had an optimistic undertone for crypto. Whether Russia is using crypto to evade sanctions or crypto donations in Ukraine are used to fund war efforts, the next phase of crypto adoption will look very different from the last.

Cryptos continue to boast solid fundamentals and constant innovation. The correlation between crypto and stocks that rose early this year is also declining. There may be a sentiment change around crypto as institutions are gradually entering the space.