AMINA Bank AG

AMINA Bank AG  AMINA UK

AMINA UK  AMINA Hong Kong

AMINA Hong Kong  AMINA EU

AMINA EU Executive Summary

- At close to $300 billion market cap, stablecoins have now become a killer use case in crypto to grow into crypto’s 8th largest sector. It has reached a staggering scale very few imagined even five years ago.

- In 2025, Solana and Base (Ethereum Layer-2 built by Coinbase) have emerged as the most active chain for stablecoin usage, with Ethereum, Tron and BNB Chain following closely behind.

- Merchant related stablecoin transaction volume has exceeded $2.2 trillion, now accounting for more than 5% of global stablecoin activity.

- Regulators are closely monitoring stablecoins, aiming to simultaneously support fintech innovation and safeguarding fiat strength. Jurisdictions are positioning themselves competitively to attract stablecoin projects.

- The market is gearing up for the launch of new stablecoin-focused projects including the likes of Peter Thiel-backed Plasma Network, Ethena Labs’ TradFi-focused stablecoin incubated by Franklin Templeton and perp DEX Hyperliquid’s USDH.

Introduction

Markets have always leaned on anchors of stability to make trade possible. Whether it was gold in the past or the US Dollar today. Crypto, however, is notoriously unstable.

Back when crypto projects were racing to build the most decentralised, scalable and secure blockchains between 2017 and 2021, one company saw a different opportunity: enabling crypto trade through a stablecoin. That company was Tether, and its rise has since become one of the defining stories of the industry. The scale of its annual profits has left the entire market stunned (for example, the company made a total net profit of $5.7 billion in H1 2025), sparking a rush where every player now wants a piece of the action. The story of Tether and how every single Dick and Harry in crypto is now eyeing or vying for a share of their enormous gains is one for the books. Today, there are over 350 US dollar-based stablecoins, not including several highly-anticipated stablecoin announcements coming up.

It’s easy to get lost or distracted by the sheer number of stablecoin announcements. This begs the question: why are there so many stablecoins and how will the landscape look like in the future?

The Birth of Crypto Stables

From Gold playing that role in the 1800s to the US Dollar taking the crown by 1944 as the world’s reserve currency, markets have always looked towards reliable forms of value to create economies.

Meanwhile, crypto has been characterised by chaos. The sector currently has close to 19,000 tokens. The cryptocurrency market is also notorious for its volatility. This created the need for stable denominators of value against which volatile assets in the sector can be traded. This gap gave birth to stablecoins.

The first attempt came in the form of BitUSD released in July 2014. This was issued on the BitShares blockchain and was designed to be pegged to the US Dollar. However, the project lost its peg in 2018 and has not recovered since. Following BitUSD, NuBit was another stablecoin which was launched in 2014 but failed in being successful.

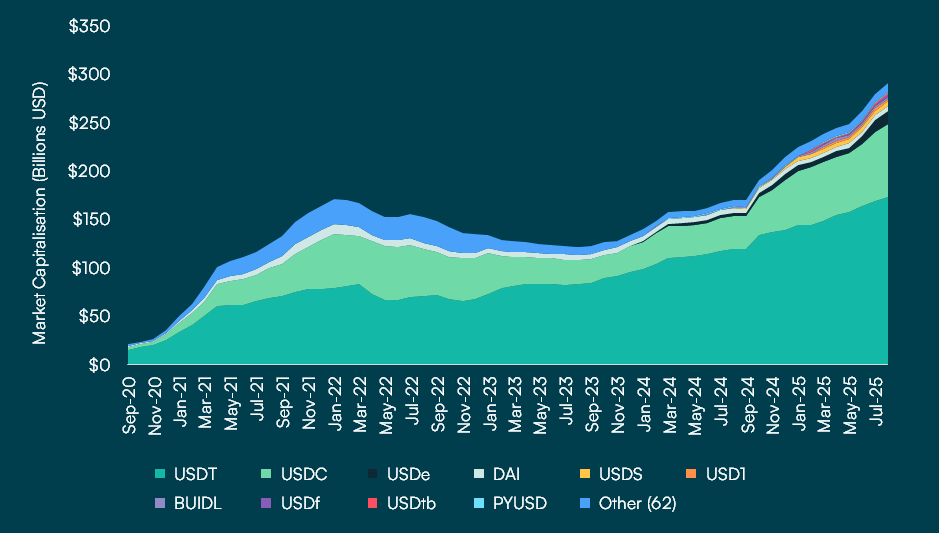

Another project called Realcoin got its origins in 2012 on the Bitcoin network. By November 2014, it had rebranded to USD Tether (USDT) and announced tokens pegged to three fiat currencies (the US Dollar, the Japanese Yen and the Euro) each backed by cash and cash equivalents. A few months later, in January 2015, Bitfinex listed USDT, sparking the adoption curve that would define the next decade in crypto. As of September 2025, USDT’s market cap stands at $172 billion, cementing it as the dominant player with a 63% stablecoin market share.

Then came new challengers. In 2017, MakerDAO launched DAI, the first decentralised stablecoin. Rather than relying on bank reserves, DAI was backed by overcollateralised crypto locked into Maker’s smart contracts. In August 2024, Maker rebranded to Sky Protocol, and DAI to USDS. However, the model remained the same with every token being fully backed by crypto deposits. Today, USDS commands a market cap of $8.2 billion.

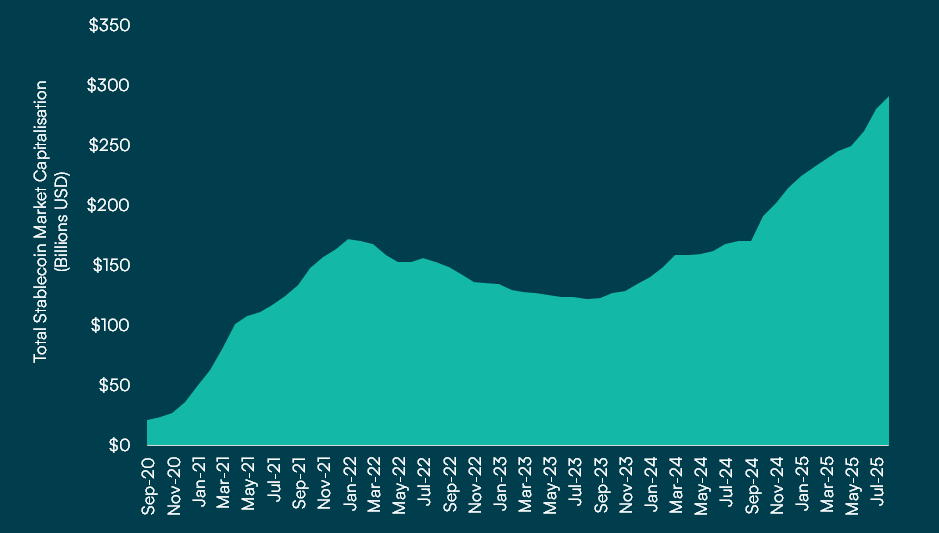

From BitUSD’s failed peg to Tether’s dominance and Maker’s decentralised design, these early projects laid the foundation for what is now a multibillion-dollar sector industry built on the idea that crypto needs its own version of money that doesn’t move like the rest of the market. Today, it stands as the 8th largest sector in crypto behind smart contract platforms and L1s, with a combined market value of $298 billion.

Figure 1: As of 24 September 2025, total stablecoin market capitalisation has grown to over $298 billion.

Source: Artemis, AMINA Bank (24 September 2025)

Just behind Tether sits Circle’s USD Coin (USDC), the second-largest stablecoin with a market cap just under $74 billion as of 22 September 2025. Like USDT, it is pegged 1:1 to the US dollar and fully backed by cash and short-term US Treasuries, though custody rests with Circle. Both USDC and USDT are centralised by design, with reserves managed by their issuers. The sector has also expanded into non-dollar pegs. Gold-backed stablecoins such as Paxos’ PAXG and Tether’s XAUT tie their value to physical bullion, offering investors a tokenised way to hold gold.

Newer models have pushed innovation further. Ethena’s USDe introduced yield-bearing stablecoins in a way previous attempts failed to deliver. By combining ETH staking with perpetual hedge positions, Ethena generates returns distributed to holders of sUSDe. The model has found product-market fit with USDe’s market cap growing more than 550% in the past year.

Alongside, institutions have rolled out cash-equivalent tokens linked to short-term Treasuries. These include BlackRock’s USD Institutional Digital Liquidity Fund, Franklin Templeton’s Onchain US Government Money Fund (shares issued as BENJI tokens), and Ondo’s Short-Term US Treasuries Fund. Together, they show how yield-bearing stablecoin products are expanding beyond DeFi experiments into mainstream asset management.

Figure 2: USDT leads the stablecoin market with the highest market cap ($173 billion), followed by USDC ($74 billion) and USDe ($13.9 billion)

Source: Artemis, AMINA Bank (24 September 2025)

Regulatory Developments

Stablecoins issuers have in the past been scrutinised by regulatory authorities. For example, in 2023, both Paxos and Coinbase had disclosed that the US SEC was investigating each of them for their stablecoin-related activities. But today, regulators are not just monitoring but actively designing frameworks to support stablecoin adoption, and the contest to become the leading hub for issuers is intensifying. Let’s look at how we got here and where the regulatory landscape for stablecoins stands today.

In 2024, stablecoins crossed a milestone few expected to happen so soon. Annual transfer volumes hit $27 trillion, overtaking the combined volume processed by Visa and Mastercard. By early 2025, the market cap of stablecoins onchain had passed $213 billion. That scale commanded immediate attention in Washington. US Treasury Secretary Scott Bessent hinted that reserve rules for stablecoins could fuel more than $2 trillion of demand for US Treasuries. Stablecoins presented the opportunity to support fintech innovation while also preserving global US Dollar dominance.

Momentum from political lobbying led by committees such as Fairshake (backed by Coinbase and XRP’s Ripple Labs) aligned with this urgency and set the stage for formal rules. The result was the GENIUS Act, passed in June 2025. It introduced a three-tier licensing system for issuers. It mandated that every stablecoin must be backed 1:1 by US Dollars, short-term Treasuries or other high-quality liquid assets. Issuers were barred from paying interest, lending reserves, or proprietary trading ensuring stablecoins remain payment instruments and not investment products.

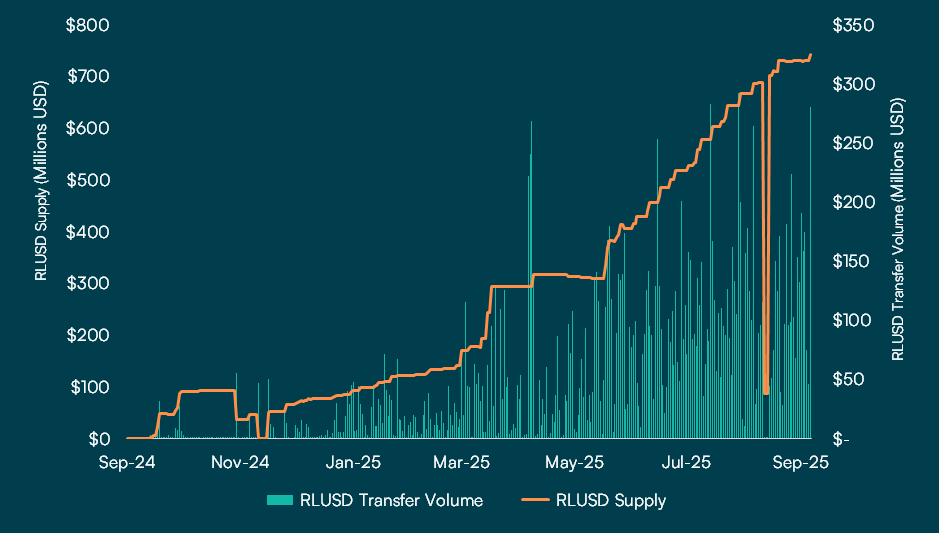

This directly led to USDC issuer Circle emerging as an early beneficiary. Following the news, the company’s stock (which IPO’d earlier that month) rose 34% to reach its all-time high of $292.77 per share. Meanwhile, Ripple was another early mover having launched its USD-pegged RLUSD stablecoin in December 2024. Launched under a trust charter granted by New York’s Department of Financial Services (NYDFS), RLUSD is fully backed by cash, US Treasuries, and other government securities. The GENIUS Act also created a runway for traditional giants like JP Morgan and Bank of America to issue their own stablecoins. In response to the GENIUS Act’s federal eligibility criteria, Ripple Labs, the parent company behind the XRP Ledger and the RLUSD stablecoin has formally applied for a national banking license with the Office of the Comptroller of the Currency (OCC).

Figure 3: Ripple’s RLUSD has immensely benefitted from a friendlier regulatory environment in the US, with supply rising to over $700 million in less than a year since launch in Q4 2024.

Source: Artemis, AMINA Bank (24 September 2025)

In the European Union, the Markets in Crypto-Assets (MiCA) regulation covers guidelines for stablecoin issuers. It became fully enforceable in December 2024, making it illegal to issue or trade many stablecoins in the EU unless the issuer holds an EU license and meets its transparency, reserve and redemption rules. Circle is a major player that has currently obtained authorisation to offer its stablecoins (like USDC and EURC) across Europe.

In Hong Kong, a Stablecoins Bill was passed in May 2025, which came into effect in August 2025. It sets out licensing, reserve, governance and AML rules for fiat-pegged tokens. Issuers will need to be supervised and meet strict requirements to operate legally. Meanwhile in Japan, stablecoins are legally classified as digital money, limiting issuance to licensed institutions with full redemption rights and banning algorithmic or unbacked models.

In the Middle East, Bahrain introduced the Stablecoin Issuance and Offering (SIO) Module, allowing fiat-backed stablecoins (pegged to Bahraini Dinar or USD) under regulatory oversight, while banning algorithmic ones. And in South Korea, the government is pushing for stablecoin law by the end of 2025, pausing its CBDC work for now, and local banks are preparing Won-backed stablecoins once the rules are in place.

These regulatory moves show a pattern where regulators are encouraging stablecoin innovation but only under strict guardrails like complete reserve backing, redemption rights, custody rules, AML controls and clear oversight.

The Stablecoin Growth Story

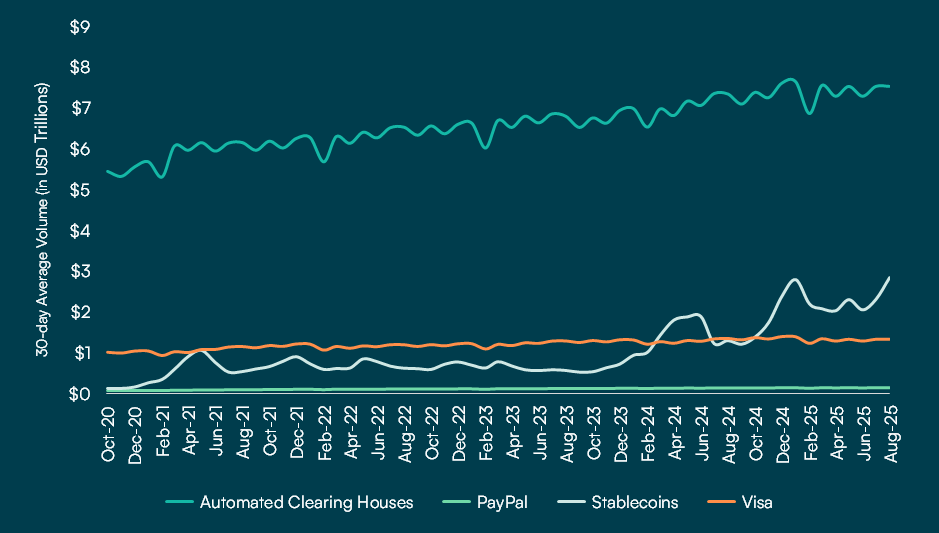

Total supply jumped more than 53% in 2024, ending the year at $214 billion. The momentum carried into 2025, with supply climbing another 34% in the last 9 months to $288 billion. This is not idle capital. Over the past 30 days alone, stablecoin transaction volume topped $2.2 trillion, nearly catching up with automated clearing houses (ACHs), which processed $5.3 trillion in the same period. By comparison, PayPal and Visa moved just over $1 trillion combined.

Figure 4: Stablecoin volumes have surpassed volumes on PayPal and Visa and are quickly catching up with automated clearing houses.

Source: Artemis, AMINA Bank (24 September 2025)

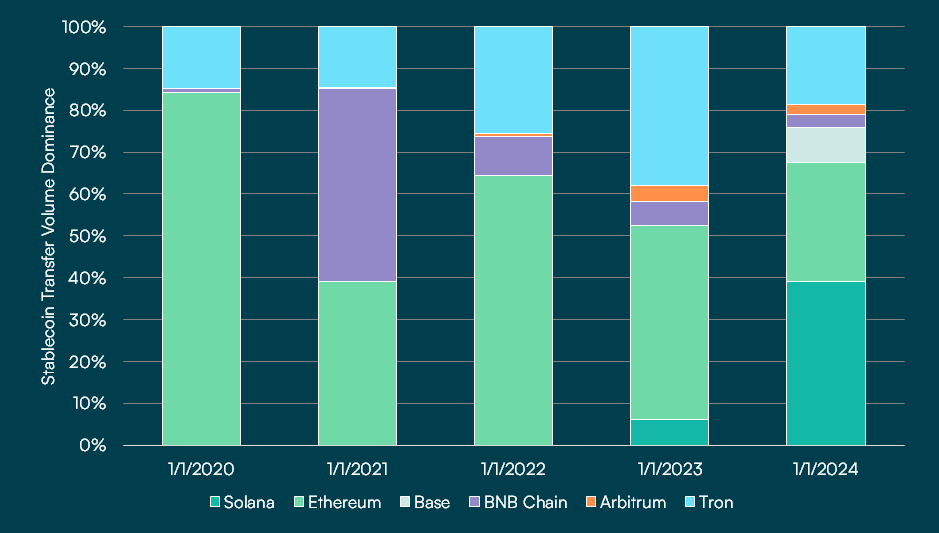

On the blockchain level, Ethereum leads with a stablecoin market cap of $165.3 billion, followed by Tron at $76.9 billion and Solana at $12.5 billion. Ethereum’s share rose slightly year-on-year, while Tron slipped from 35% to 28% as activity shifted to newer ecosystems.

In 2025, Solana and Base emerged as the most active chains for stablecoin usage with stablecoin transfer volumes rising to 7.9 million times and 18 thousand times of their respective levels compared to 2024. Ethereum, Tron, and BNB Chain follow closely behind. Solana’s rise was especially sharp, doubling its stablecoin market cap between January and February 2025, coinciding with the launch of the $TRUMP token and a surge in memecoin activity on the Pump.fun launchpad. Meanwhile for Base, the rise was catalysed by activity on their Zora creator platform as well as an overall jump in onchain activity due to airdrop expectations.

Figure 5: Stablecoin Transfer Volume by Chain

Source: Artemis, AMINA Bank (24 September 2025)

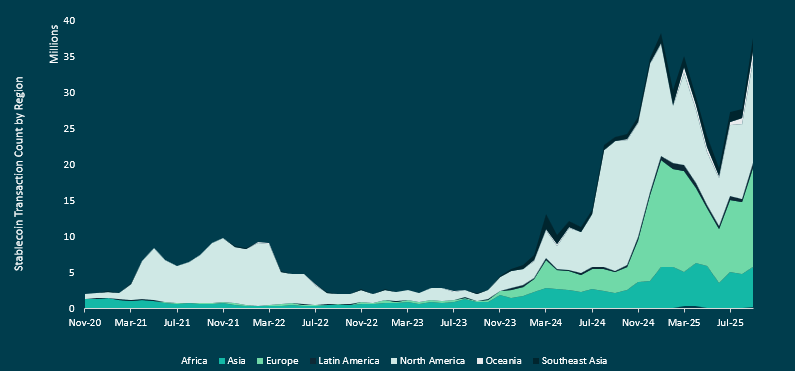

The differences in usage patterns are also clear. USDC dominates overall transfer volume, but USDT remains the go-to coin for peer-to-peer (P2P) transactions, particularly on Tron, which has become the hub for cross-border remittances. Regionally, North America currently accounts for 22.2 million transactions per day, followed closely by Europe at 21.1 million. Asia comes in third at 9.4 million, while Latin America and Africa process around 1.1 million and 365 thousand daily transactions, respectively. Across all geographies, USDT remains the most widely used stablecoin.

Figure 6: Stablecoin transaction count by region

Source: Artemis, AMINA Bank (24 September 2025)

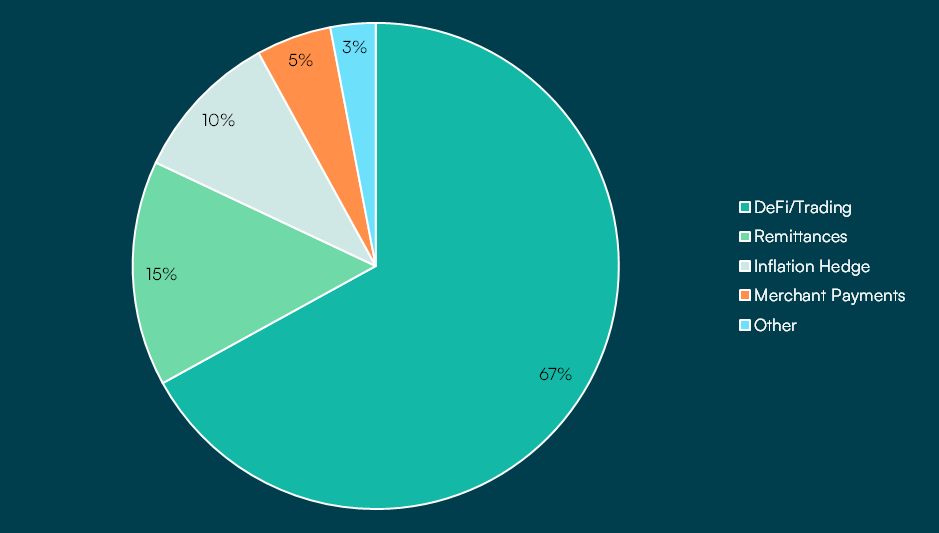

One fast-growing use case of stablecoins is merchant payments. Stablecoins bypass traditional rails like Visa, enabling global commerce directly onchain. According to CoinLaw.io, at least 5% of global stablecoin activity now comes from merchant transactions. With yearly volumes above $44.2 trillion, this puts merchant payments at more than $2.2 trillion annually.

Figure 7: Stablecoin usage by purpose

Source: CoinLaw.io, AMINA Bank

At the same time, stablecoins have also become the foundation for the boom in real-world asset (RWA) tokenisation. The onchain RWA market grew from under $1 billion in early 2023 to more than $15.8 billion today. Stablecoins provided the liquidity and trust for that growth, proving that off-chain assets could be reliably represented onchain. In many ways, stablecoins were the proof of concept for tokenisation, which has created a foundation upon which other tokenised RWAs may thrive.In August 2023, Ondo Finance launched USDY, a yield-bearing stablecoin collateralised by US Treasuries and bank deposits. USDY automatically accrues interest into its price, turning Treasury yield into an onchain stable asset. Its market cap has more than doubled in 12 months to $674 million. Maple Finance takes another approach, focusing on undercollateralised lending to real-world firms. Investors fund pools with USDC and USDT, while borrowers receive stablecoin loans that can be converted to fiat off-chain. In March 2025, Maple introduced syrupUSDC on Solana which is a tokenised representation of a slice of its private credit pools. SyrupUSDC acts like a yield-bearing stablecoin backed by institutional loans, and the demand has been explosive: its market cap hit $1.13 billion within six months which is a 1,700% increase.

Together, these trends highlight how stablecoins are no longer just trading tools. They are becoming the backbone of global payments and the launchpad for onchain finance, from everyday transactions to multi-billion dollar real-world assets.

Sectoral Developments

Crypto protocols are actively looking to generate more value within their ecosystems and as a result, stablecoins have now become a core part of their revenue strategy. A prime example is Hyperliquid which has been one of the fastest-growing decentralised perpetual exchanges this year. It initially used USDC as the stablecoin within its ecosystem for trading. However, it recently announced the launch of its own stablecoin (ticker: USDH) to control its liquidity. The announcement opened a bidding process which drew participation from established players including Paxos and Ethena in the form of proposal submissions to build out the USDH stablecoin. Ultimately, a newer startup called Native Markets won the majority of votes from Hyperliquid’s validators to win the bid for the USDH ticker.

Soon after the process concluded, Circle announced it would deploy USDC natively on Hyperliquid and even took a stake in Hyperliquid’s HYPE token to defend USDC’s market dominance on the exchange. This sets up a dynamic rivalry on the platform between USDH whose reserve profits can potentially be fed back into user incentives versus Circle’s battle-tested USDC. The Hyperliquid saga illustrates how vital stablecoins have become for crypto platforms. By owning the stablecoin infrastructure, protocols aim to capture value even if it means navigating governance challenges. As regulatory clarity improves in the US and the EU, we can expect more exchanges, lenders and networks to follow suit by weaving stablecoins directly into their core architecture, ensuring these digital dollars remain the lifeblood of the crypto economy.

Stablecoins were birthed by DeFi and the sector has seen massive growth. New stablecoin protocols continue to prop up across networks. But the next season for stablecoins will most likely be similar to what we witnessed with BTC and ETH in 2024: driven by institutional participation.

In 2023, PayPal became the first major fintech to issue a US dollar stablecoin (PYUSD) under strict New York NYDFS regulation. Global banks have also entered the race. JP Morgan uses its internal deposit coin (JPM Coin) for corporate payments and even ran cross-border pilots. In Europe, Societe Generale’s digital asset arm launched a euro-backed stablecoin, EUR CoinVertible (EURCV), on the Ethereum blockchain to bridge traditional banking and crypto markets. These reflect a broader trend of banks and payment companies using stablecoins to upgrade legacy payment systems. For instance, Visa has begun settling transactions in USDC on Ethereum and Solana. Such initiatives demonstrate that stablecoins are moving from being a pure crypto play to becoming a core part of the plumbing of global finance.

Major financial institutions are also tying up with DeFi projects to leverage blockchain-based stablecoins. A notable example is Franklin Templeton and Fidelity’s venture arm backing Ethena Labs with $100 million to develop a new regulated stablecoin aimed at institutional use. Even traditional firms are experimenting with stablecoins operationally. Consulting firm Ernst & Young (EY) worked with PayPal and Coinbase to settle invoices in USDC and payments company Payoneer is piloting USDC for international payouts.

The crypto market is also gearing up to welcome new stablecoin-focused protocols. Plasma is a Layer-1 blockchain built specifically for stablecoins and payments. It optimises for speed in stablecoin transfers, even enabling zero-fee USDT transfers. The project has some high-profile backers having raised $24 million in funding led by Framework Ventures with participation from Bitfinex, Peter Thiel and Tether’s CTO Paolo Ardoino. Plasma is targeting emerging markets where dollar access is in demand.

An upcoming Ethereum scaling solution is MegaETH and it is launching its own US dollar-pegged stablecoin called USDm to power its ecosystem. USDm will be issued on Ethena’s USDtb rails meaning its reserves will be held mostly in BlackRock’s tokenised US Treasury fund (BUIDL) along with other liquid stablecoins. This gives USDm a transparent, institutionally-backed reserve model from the start. Rather than offering direct cash redemption at launch, USDm will be swappable 1:1 with USDtb.

Conclusion

Stablecoins have gone from being a crypto side story to the backbone of the sector today. PayPal’s PYUSD, Ethena’s USDe and Plasma show how both tradfi and crypto players today are investing millions into building out stablecoin infrastructure. Traditional big Banks have entered the race too. Regulators are trying to keep up with regulations being framed both in order to support fintech innovation as well as to maintain their fiat dominance. More than simply being tokens, stablecoins have become power plays for governments and protocols.

___________________________________________________

Disclaimer – Research

This document has been prepared by AMINA Bank Ltd. (“AMINA”) in Switzerland. AMINA is a Swiss licensed bank and securities dealer with its head office and legal domicile in Switzerland. It is authorised and regulated by the Swiss Financial Market Supervisory Authority (“FINMA”).

This document is published solely for educational purposes; it is not an advertisement nor a solicitation or an offer to buy or sell any financial investment or to participate in any particular investment strategy. This document is for publication only on AMINA website, blog, and AMINA social media accounts as permitted by applicable law. It is not directed to, or intended for distribution to or use by, any person or entity who is a citizen or resident of or located in any locality, state, country or other jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation or would subject AMINA to any registration or licensing requirement within such jurisdiction.

Research will initiate, update and cease coverage solely at the discretion of AMINA. This document is based on various sources, incl. AMINA ones, and was generated using artificial intelligence (“AI”). No representation or warranty, either express or implied, is provided in relation to the accuracy, completeness or reliability of the information contained in this document, except with respect to information concerning AMINA. The information is not intended to be a complete statement or summary of the subjects alluded to in the document, whereas general information, financial investments, markets or developments. AMINA does not undertake to update or keep current information. Any statements contained in this document attributed to a third party represent AMINA’s interpretation of the data, information and/or opinions provided by that third party either publicly or through a subscription service, and such use and interpretation have not been reviewed by the third party.

Any formulas, equations, or prices stated in this document are for informational or explanatory purposes only and do not represent valuations for individual investments. There is no representation that any transaction can or could have been affected at those formulas, equations, or prices, and any formula(s), equation(s), or price(s) do not necessarily reflect AMINA’s internal books and records or theoretical model-based valuations and may be based on certain assumptions. Different assumptions by AMINA or any other source may yield substantially different results.

Nothing in this document constitutes a representation that any investment strategy or investment is suitable or appropriate to an investor’s individual circumstances or otherwise constitutes a personal recommendation. Investments involve risks, and investors should exercise prudence and their own judgment in making their investment decisions. Financial investments described in the document may not be eligible for sale in all jurisdictions or to certain categories of investors. Certain services and products are subject to legal restrictions and cannot be offered on an unrestricted basis to certain investors. Recipients are therefore asked to consult the restrictions relating to investments, products or services for further information. Furthermore, recipients may consult their legal/tax advisors should they require any clarifications.

At any time, investment decisions (including, among others, deposit, buy, sell or hold investments) made by AMINA and its employees may differ from or be contrary to the opinions expressed in AMINA research publications.

This document may not be reproduced, or copies circulated without prior authority of AMINA. Unless otherwise agreed in writing, AMINA expressly prohibits the distribution and transfer of this document to third parties for any reason. AMINA accepts no liability whatsoever for any claims or lawsuits from any third parties arising from the use or distribution of this document.

©AMINA, Kolinplatz 15, 6300 Zug