AMINA Bank AG

AMINA Bank AG  AMINA UK

AMINA UK  AMINA Hong Kong

AMINA Hong Kong  AMINA EU

AMINA EU Market State and Institutional Adoption (September 2025)

Tokenised cash has matured into a multi-hundred-billion-dollar ecosystem at the centre of institutional finance. As of September 2025, the sector holds close to $300BN in circulation. Stablecoins dominate with c. $270BN, accounting for around 90% of the market. Tokenised treasuries and money market funds (MMFs) have surged to $8BN after an 80% increase this year, while the broader real-world asset tokenisation segment excluding stablecoins has expanded 600% to c. $28BN. These figures confirm that tokenisation is no longer at the experimental stage but is embedded in institutional liquidity and payment operations.

Models of Tokenised Cash

Three distinct models define the landscape. Stablecoins provide 24/7 payment rails that operate outside traditional clearing systems. Tokenised MMFs deliver blockchain-native yield strategies and new liquidity instruments. Deposit tokens offer instant settlement while remaining fully integrated into regulated banking. Collectively, these models signal a fundamental rethinking of financial market infrastructure.

Tokenised Money Market Funds

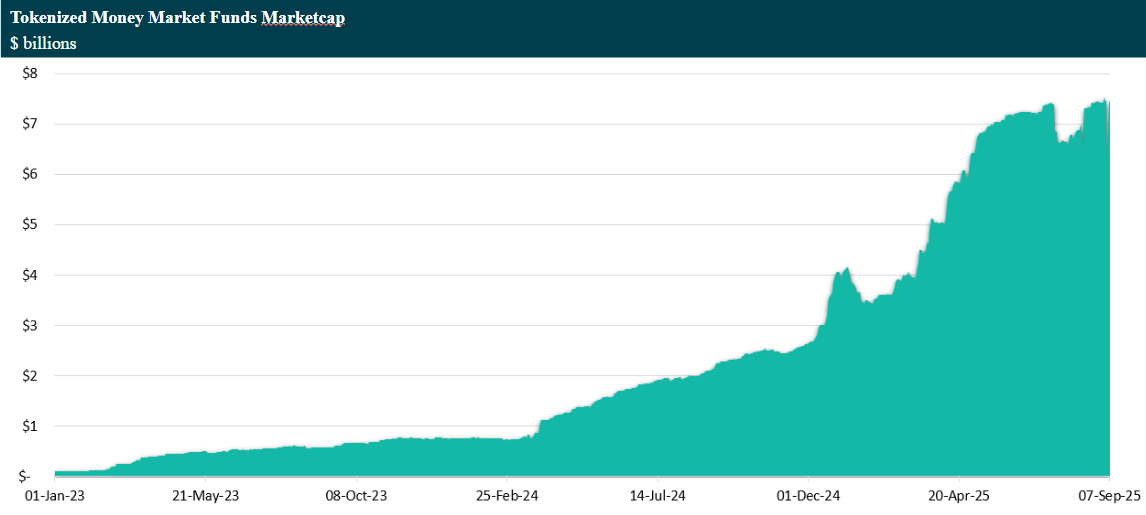

BlackRock’s BUIDL fund remains the flagship product with c. $2.3BN in assets under management across Ethereum, Polygon, Solana, Optimism, Arbitrum, Avalanche and Aptos. Although down from its June peak of c. $2.9BN, BUIDL has become the institutional benchmark. Franklin Templeton’s BENJI fund follows as the second largest. Goldman Sachs and BNY Mellon have strengthened distribution by integrating tokenised MMFs into BNY Mellon’s LiquidityDirect and Goldman’s Digital Asset Platform.

The operational advantages are immediate. Treasury desks gain instant redemptions, dividend payments are automated through smart contracts, and liquidity is accessible at all times. Collateral management is now an important use case. BUIDL tokens can be pledged on Crypto.com and Deribit while continuing to accrue underlying yield. This addresses liquidity pressures such as those seen during COVID-19 and the UK gilt crisis when collateral proved slow to mobilise.

Figure 1: Year on Year Growth of Tokenised Money Market Funds Market Capitalisation

Source: RWA.xyz, AMINA Bank

Stablecoins as Global Payment Infrastructure

Stablecoins remain the dominant instrument with c. $270BN in circulation. Tether leads with c. $166BN and a c. 61% market share, followed by USDC with more than $70BN. Average daily USDT transaction volumes of c. $20–25BN make stablecoins the largest blockchain-native payment network to date.

The scale is extraordinary. In 2024, stablecoins processed c. $32TN in transactions, equal to c. 3% of global cross-border payments. McKinsey projects that their share could rise to 20% within five years, representing more than $60T in annual flows. Adoption is uneven across geographies, with Nigeria, Argentina and Vietnam leading in grassroots usage. In these markets, stablecoins are not only efficient but also provide resilience in volatile monetary environments.

Tokenised Deposits

Deposit tokens have emerged as the most bank-centric model. JPMorgan’s JPMD, developed on Coinbase’s Base, is limited to institutional clients and combines regulatory oversight with real-time settlement. Citi has made tokenised deposits a strategic priority. DBS Bank, working with Ant International, has created multi-currency Treasury Tokens capable of clearing across more than 40 currencies instantly.

The operational benefits are clear. Cross-border transfers are settled instantly without correspondent banks. Liquidity management becomes continuous, with internal estimates suggesting savings of around $150MN per year for every $100BN in deposits. Compliance processes are automated through programmable contracts that embed KYC and AML directly into settlement flows.

Regulation and Global Divergence

The regulatory environment has moved decisively from theory to practice. In the United States, the GENIUS Act was signed in July 2025, establishing a federal stablecoin framework. It mandates 1:1 reserves in USD or Treasuries, places large issuers under Office of the Comptroller of the Currency (OCC) oversight, guarantees bankruptcy priority for holders, and prohibits interest payments. Implementation is scheduled for mid-2026.

The European Union’s Markets in Crypto Assets (MiCA) regulatory framework takes a broader approach by classifying stablecoins as either e-money or asset-referenced tokens. It requires reserve disclosures, daily transaction caps, and licensing for issuers. In Asia-Pacific, regulators have advanced into live deployment. Singapore’s Project Guardian now involves more than 40 institutions across seven jurisdictions, while Hong Kong’s Project Ensemble has positioned the city as a hub for wholesale Central bank digital currency (CBDC) settlement. The mBridge project has processed HK$171MN in multi-currency transactions in under 30 seconds. Switzerland’s Project Helvetia has issued CHF 750MN in digital bonds using wholesale CBDC, and Australia’s Project Acacia is testing tokenised fixed income, private credit, receivables and carbon credits under ASIC oversight.

Efficiency and Cost Dynamics

The numbers underline the efficiency gains. Cross-border settlement times have collapsed from three to five days to under 30 seconds. Settlement costs have fallen from the traditional 6% of transaction value to 2–3%. Liquidity optimisation delivers around $150MN in annual savings for every $100BN in deposits. Tokenised MMFs are particularly transformative since they can be pledged as collateral while continuing to generate yield, reducing systemic risk.

Market Concentration and Competition

Market share is heavily concentrated. BlackRock controls more than 30% of tokenised MMFs, while Tether dominates stablecoins with a 61% share that regulators increasingly view as a systemic risk. JPMorgan holds a first-mover advantage in deposit tokens, but Citi and DBS are catching up rapidly. Multi-chain expansion has emerged as a differentiator. BlackRock’s decision to extend BUIDL to Solana this year shows that institutions are willing to embrace non-Ethereum ecosystems when performance benefits are demonstrable.

Risk Considerations

Tokenised cash mitigates some traditional risks but introduces new ones. Atomic settlement removes counterparty and settlement risks. Deposit tokens carry Federal Deposit Insurance Corporation (FDIC) or central bank backing. Stablecoin risk still varies depending on reserve quality and issuer practices. Operational concerns remain around smart contract vulnerabilities, network congestion and custody security. However, institutional products such as BUIDL have processed billions without major incidents, strengthening market confidence.

Conclusion

The evolution of tokenised cash reflects a clear shift in financial market infrastructure. Recent years have already shown consolidation among stablecoin issuers, rising bank participation in deposit tokens, and early central bank pilots of wholesale CBDCs. Between 2025 and 2026, regulatory frameworks such as the US GENIUS Act and Europe’s MiCA are expected to shape market structure more firmly, with stablecoins and bank-issued tokens coming under uniform oversight.

The period from 2026 to 2028 is likely to highlight questions of interoperability as stablecoins, deposit tokens and CBDCs begin operating in parallel. Market experiments with atomic swaps, cross-chain bridges and harmonised compliance standards are expected to accelerate. By the end of the decade, many central banks plan to advance CBDC deployment, raising questions about how these public-sector initiatives will interact with private tokenised funds and stablecoin infrastructure.

If current growth patterns persist, tokenised funds may represent several hundred billion dollars in assets, while the broader tokenised cash ecosystem could approach trillion-dollar scale. Whether this leads to a more resilient financial system or introduces new systemic risks remains an open question that regulators, banks and technology providers are still in the process of testing.

_______________________________________

Disclaimer – Research and Educational Content

This document has been prepared by AMINA Bank Ltd. (“AMINA”) in Switzerland. AMINA is a Swiss licensed bank and securities dealer with its head office and legal domicile in Switzerland. It is authorized and regulated by the Swiss Financial Market Supervisory Authority (“FINMA”).

This document is published solely for educational purposes; it is not an advertisement nor a solicitation or an offer to buy or sell any financial investment or to participate in any particular investment strategy. This document is for publication only on AMINA website, blog, and AMINA social media accounts as permitted by applicable law. It is not directed to, or intended for distribution to or use by, any person or entity who is a citizen or resident of or located in any locality, state, country or other jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation or would subject AMINA to any registration or licensing requirement within such jurisdiction.

Research will initiate, update and cease coverage solely at the discretion of AMINA. This document is based on various sources, incl. AMINA ones, and was generated using artificial intelligence (“AI”). No representation or warranty, either express or implied, is provided in relation to the accuracy, completeness or reliability of the information contained in this document, except with respect to information concerning AMINA. The information is not intended to be a complete statement or summary of the subjects alluded to in the document, whereas general information, financial investments, markets or developments. AMINA does not undertake to update or keep current information. Any statements contained in this document attributed to a third party represent AMINA’s interpretation of the data, information and/or opinions provided by that third party either publicly or through a subscription service, and such use and interpretation have not been reviewed by the third party.

Any formulas, equations, or prices stated in this document are for informational or explanatory purposes only and do not represent valuations for individual investments. There is no representation that any transaction can or could have been affected at those formulas, equations, or prices, and any formula(s), equation(s), or price(s) do not necessarily reflect AMINA’s internal books and records or theoretical model-based valuations and may be based on certain assumptions. Different assumptions by AMINA or any other source may yield substantially different results.

Nothing in this document constitutes a representation that any investment strategy or investment is suitable or appropriate to an investor’s individual circumstances or otherwise constitutes a personal recommendation. Investments involve risks, and investors should exercise prudence and their own judgment in making their investment decisions. Financial investments described in the document may not be eligible for sale in all jurisdictions or to certain categories of investors. Certain services and products are subject to legal restrictions and cannot be offered on an unrestricted basis to certain investors. Recipients are therefore asked to consult the restrictions relating to investments, products or services for further information. Furthermore, recipients may consult their legal/tax advisors should they require any clarifications.

At any time, investment decisions (including, among others, deposit, buy, sell or hold investments) made by AMINA and its employees may differ from or be contrary to the opinions expressed in AMINA research publications.

This document may not be reproduced, or copies circulated without prior authority of AMINA. Unless otherwise agreed in writing, AMINA expressly prohibits the distribution and transfer of this document to

third parties for any reason. AMINA accepts no liability whatsoever for any claims or lawsuits from any third parties arising from the use or distribution of this document.

©AMINA, Kolinplatz 15, 6300 Zug