AMINA Bank AG

AMINA Bank AG  AMINA UK

AMINA UK  AMINA Hong Kong

AMINA Hong Kong  AMINA EU

AMINA EU Executive Summary

- 2025 delivered the regulatory clarity institutional adoption requires: MiCA implementation across 27 EU countries, U.S. stablecoin legislation via the GENIUS Act, and competitive licensing frameworks in Hong Kong, Singapore, and the UAE created predictable compliance pathways.

- Tokenization broke out of pilot phases into production deployments, with $18.6 billion in real-world assets onchain and major asset managers (BlackRock, Franklin Templeton, UBS) launching regulated tokenized products across government bonds, money market funds, and private credit.

- Stablecoins achieved critical mass as financial infrastructure, processing $10.66 trillion in annual transaction volume—demonstrating utility beyond crypto trading to encompass cross-border payments, corporate treasury management, and programmable settlement rails.

- The infrastructure gap became visible: institutions need bridge players that combine traditional banking’s risk management with crypto-native execution speed—a capability set that exists in neither traditional banks nor crypto-native platforms alone.

- 2026 will test execution capacity as frameworks transition to enforcement, pilot programs scale to commercial operations, and institutional allocators commit capital to infrastructure providers with proven operational track records rather than theoretical capabilities.

Introduction

2025 delivered regulatory clarity. 2026 will reveal which institutions can actually execute within those frameworks.

This is the operational challenge AMINA addresses by design. As a FINMA-regulated bank operating across Switzerland, Hong Kong, and Abu Dhabi, AMINA was built to deliver both institutional-grade compliance and crypto-native execution speed. capabilities that historically existed in separate institutions but are now required simultaneously. The question for 2026 isn’t whether tokenization, DeFi, or stablecoins will scale—it’s whether the infrastructure layer can deliver both innovation and institutional-grade risk management simultaneously.

This edition of The Bridge draws on AMINA’s operational experience serving institutional clients across both ecosystems and covers the key developments of 2025 and the themes that will define the industry’s trajectory in the year ahead.

2025: A Year of Structural Shifts

2025 was the year crypto stopped oscillating between extremes and began consolidating into a recognisable part of the financial system. Regulatory clarity deepened across major jurisdictions, tokenisation broke out of the pilot phases, DeFi matured with institutional features, and stablecoins achieved unprecedented scale. The year delivered the structural groundwork that will define what institutional digital asset markets look like in the years ahead. The developments of 2025 form the foundation upon which 2026 will build.

Regulatory Inflection Points

2025 marked a turning point in crypto regulation, creating momentum that will carry into 2026. In the United States, political changes led to a friendlier stance. New leadership at the U.S. Securities and Exchange Commission (SEC) and the Congress passing landmark bills signaled a pivot to pro-crypto regulation. Notably, the House and Senate advanced legislation to define digital assets and stablecoins, finally culminating in the signing of the GENIUS Act in July 2025. This federal clarity (after years of enforcement-only approach) has been encouraging for the industry.

In parallel, the European Union’s comprehensive regulatory framework, MiCA (Markets in Crypto-Assets), began implementation. MiCA Phase 1 (stablecoin rules) took effect in mid-2024 and Phase 2 (broader crypto-asset service provider rules) by end-2024. Throughout 2025, EU regulators and national authorities worked through licensing hundreds of firms under MiCA. The EU now leads in regulatory harmonisation, providing a single rulebook across 27 countries. This has reduced uncertainty for European crypto ventures.

Asia-Pacific saw intense hub competition. Hong Kong emerged as a major contender for global crypto hub status after launching a new licensing regime for exchanges (VATPs) in 2023. In 2025, Hong Kong doubled down and rolled out a stablecoin licensing framework with high standards for reserves and auditing.

Meanwhile, Singapore continued issuing licenses under its Payment Services Act (over 30 by 2025) and fine-tuning stablecoin rules and the UAE expanded its crypto-friendly regulatory sandbox. These jurisdictions are now vying to attract exchanges, asset managers, and fintech firms in 2026, marketing themselves as the safest havens for digital asset innovation.

Together, these regulatory inflection points (clearer U.S. and EU frameworks and competitive licensing in Asia) set the stage for more institutional participation in 2026. However, uneven approaches (e.g. strict bans or restrictions in certain countries) mean that a lot hinges on continued international cooperation to avoid a patchwork of rules. The trend is towards clarity and legitimacy. Crypto is increasingly being treated as part of the financial system, with all the oversight that entails.

Institutional Use Cases

One of 2025’s defining shifts was the move by institutions from blockchain proofs-of-concept to real production deployments. After years of small pilots, we saw tangible adoption of tokenisation and significant capital flowing into institutional crypto custody solutions – developments that will drive further growth in 2026.

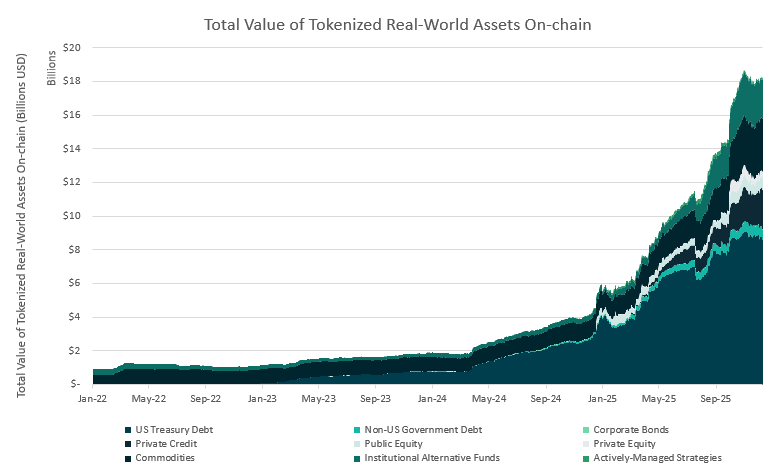

Total value of tokenised real-world assets (RWA) onchain reached new highs in 2025, hitting $18.6 billion in October. No longer confined to experiments, tokenisation had practical deployments across government bonds, money market funds, real estate, private credit, carbon credits, and even art.

Figure 1: Total value of tokenised RWAs onchain exceeded the $18 billion mark in 2025

Source: RWA.xyz, AMINA Bank

Major asset managers contributed to this surge. In 2025, BlackRock expanded its tokenisation work after the success of its spot Bitcoin ETF, conducting pilots using tokenised money-market funds on public chains for faster settlement and exploring stablecoin-based subscription/redemption flows. Franklin Templeton continued scaling its onchain U.S. Government Money Fund (FOBXX) on Stellar and Polygon, which surpassed $600 million in tokenised AUM. In Europe, Amundi and UBS Asset Management conducted MiCA-aligned pilots with tokenised fund shares on Ethereum. In Asia, HSBC ran trials on HSBC Orion, its tokenisation platform, issuing digital bond structures and enabling institutions to test programmable settlement.

Hand-in-hand with tokenisation, institutional custody and trading infrastructure matured. As more funds and assets went onchain, institutions demanded enterprise-grade custody and the market responded.

Additionally, companies began leveraging crypto beyond investments. More than 280 public companies adopted digital asset treasury (DAT) strategies in 2025, holding Bitcoin or other crypto on their balance sheets as reserve assets. Collectively they held over $115 billion in crypto, often to hedge inflation or diversify reserves. This mainstreaming of crypto in corporate finance indicates that, going forward, CFOs could treat tokenised cash and crypto assets as part of the standard corporate finance toolkit.

The Institutionalisation of DeFi: Solving for Governance, not Technology

The 2025 narrative around DeFi shifted. DeFi protocols demonstrated resilience (92 incidents, $470M losses vs. CeFi’s $1.9B in breaches). But institutional adoption isn’t just driven by comparative safety statistics. It is driven by risk assessment frameworks that institutional investment committees can actually use and evaluate. Only through these frameworks can decision-makers begin to justify DeFi allocations using familiar risk evaluation methods.

We saw DeFi protocols implement more institution-friendly features while retaining the open innovation that drives this sector. For example, Aave announced native isolation modes for lending positions and compliance-ready pool configurations with its V4 (currently in testnet). This allows regulated entities to deploy liquidity in segregated environments while still tapping into Aave’s broader liquidity architecture. Uniswap v4’s production rollout saw the first institution-oriented hook modules launched by regulated market participants, including KYC-gated liquidity pools, limit-order hooks, and transaction-monitoring hooks. Meanwhile, Synthetix v3 adoption accelerated with institutions testing permissioned liquidity vaults for onchain derivatives exposure, separating regulated flows from the public pools while preserving the protocol’s composability.

The institutionalization of DeFi isn’t about protocols becoming “safer.” It’s about bridge infrastructure that translates DeFi primitives into TradFi risk language.

Consider the operational challenge: a European asset manager wants to deploy liquidity into Aave to generate yield on stablecoin holdings. Their risk committee needs:

- Counterparty risk assessment (but DeFi has no counterparties—it has protocol risk)

- Custody controls (but DeFi requires wallet interactions, not traditional custody)

- Regulatory classification (but MiCA doesn’t neatly categorize DeFi lending)

Audit trail (but on-chain transparency doesn’t match existing reporting systems)

Stablecoins

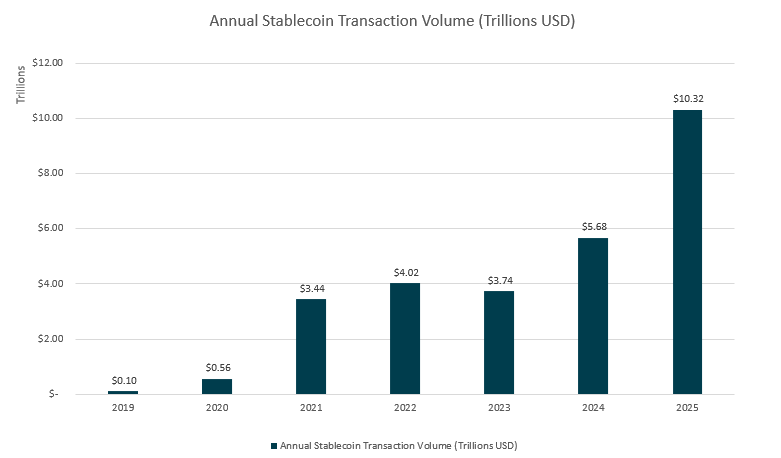

2025 was the year stablecoins went mainstream. Stablecoins became the hot topic in both crypto circles and policy debates. Stablecoin usage metrics shattered all records, firmly establishing the sector as a critical piece of the global financial plumbing.

Stablecoins proved their utility at scale with total stablecoin transaction count hitting 1.9 billion in 2025, total supply exceeding $229 billion and volumes exceeding $10.66 trillion. This has been driven by everything from crypto trading liquidity to remittances and merchant payments. Tether’s USDT still remains the largest stablecoin, doubling down on its dominance with a market cap over $185 billion and heavy usage in Asia and emerging markets. Circle’s USDC holds the second spot with roughly $75 billion market cap with strength in the US. Several new players entered the stablecoin market this year. Multiple banks including Standard Chartered and Bank of America announced plans for their own stablecoins.

Figure 2: Annual Stablecoin Transaction Volume

Source: VISA, AMINA Bank

In short, stablecoins in 2025 transitioned from a niche crypto convenience to a global financial phenomenon. As we enter 2026, stablecoins are effectively critical financial-market infrastructure. Policymakers have moved from debating whether stablecoins should be allowed to focusing on how to use them productively while keeping risks under control. The dominance of USD-backed tokens will be tested by new regional stablecoins (for local currency settlement) and possibly by CBDCs if they launch. But given the network effects and head start, USD-pegged stablecoins are likely to remain on top. The record usage levels and integration of stablecoins into everyday economic activity form a strong tailwind for the crypto industry going forward.

2026: From Frameworks to Execution

As the digital assets industry enters 2026, the focus shifts from proving concepts to executing at scale. Regulatory frameworks set in motion during 2025 now move into implementation, banks and asset managers begin integrating onchain rails into core workflows and tokenisation is poised for broader commercial adoption. The coming year will test whether the infrastructure, governance and institutional appetite developed so far can translate into sustainable growth. 2026 will be shaped not by speculation, but by the practical alignment of regulation, technology and institutional demand.

Regulation: U.S. Enforcement and APAC Hub Competition

In 2026, we expect regulatory evolution to once again be the most important determinant of crypto market progress. We expect a year focused on implementing the big frameworks set in 2025 and dealing with jurisdictional competition.

The U.S. enters 2026 with a mix of optimism and uncertainty. On one hand, 2025 saw positive signals when the SEC under a new Chair dialed back its explicit scrutiny of crypto in exam priorities and the administration actively promoted digital asset innovation as part of economic strategy. On the other hand, comprehensive crypto legislation (beyond the stablecoin law) has yet to pass the Senate, meaning many questions (security vs commodity classification, DeFi oversight, etc.) remain unresolved in law. Heading into 2026, we expect continued enforcement as a policy tool. The SEC and Commodity Futures Trading Commission (CFTC) will still pursue high-profile cases in 2026 (e.g. exchanges accused of listing unregistered securities, DeFi protocols facilitating illicit finance, etc.). The difference is, with a more industry-friendly political climate, we might see more settlements and guidance rather than pure litigation.

In APAC, 2026 will likely see an intensified competition among financial hubs to attract crypto business. Hong Kong is a focal point as it aims to prove that its regulated regime can thrive. If HK’s crypto reforms succeed in boosting domestic volumes and innovation, it could increase competition for other hubs in the region to keep up.

The Next Leg of RWA Tokenisation

All signs point to 2026 being another year to remember for tokenised real-world assets, as the pilot projects of past years scale up and new major players enter the fray. We anticipate rapid growth particularly in tokenised cash instruments (like Treasury bills) and deeper corporate adoption of blockchain-based assets for treasury and financing purposes.

Treasury-backed tokens going mainstream

Governments and corporates alike are realising the efficiency gains of onchain bonds and money market instruments and a significant fraction of the U.S. T-bill market could be mirrored on public/private blockchains within the next year. This growth will be driven by products like tokenised Treasury bill funds (several like Franklin Templeton’s, and BlackRock’s pilot BUIDL tokenised money market fund already exist) which allow near-instant settlement and 24/7 trading of TradFi assets.

The appeal to institutions is clear: instead of parking cash in bank deposits, a corporation could hold a tokenised T-bill yielding 5%, redeemable or tradeable at will. Such programmable money market tokens can integrate into DeFi or be used as collateral across crypto markets, blurring lines between traditional and crypto liquidity. Regulators have warmed to this concept (the U.S. OCC gave banks the green light to custody stablecoin reserves in 2025, which is analogous to tokenised cash). We expect major banks and fintechs in 2026 to either partner with existing tokenisation firms or launch their own tokenised cash products (possibly under regulatory sandboxes).

Private markets

2026 will likely see tokenisation move from PoCs to routine use in private capital markets. Standard Chartered, HSBC, and SGX’s Marketnode, among others, have been building infrastructure for tokenised bond issuance and distribution. We also foresee private equity funds and real estate trusts expanding tokenised share classes for investor access.

The narrative is shifting with tokenisation no longer being just about exotic assets but also about bread-and-butter financial assets (loans, invoices, leases). For instance, there’s buzz about trade finance wherein companies may issue tokens representing invoice payments or warehouse receipts to raise working capital onchain at lower cost. Infrastructure financing might also get a boost via security tokens (e.g. renewable energy projects issuing tokenised revenue-share instruments to global investors).

Infrastructure to support scaling of Tokenisation

The scaling of tokenisation will be underpinned by robust marketplaces and interoperability. We anticipate the rise of tokenised asset exchanges (both centralised and decentralised) that specialise in RWAs. Already, platforms like ADDX, Securitize, and multi-bank consortia (Switzerland’s SDX, Singapore’s 1X) are active and 2026 could see consolidation or growth of a few as leaders. These platforms will emphasise compliance (only verified investors can trade certain assets) while offering near-24/7 liquidity.

Adoption, however, will hinge on trust. Therefore, regulatory acceptance, user-friendly platforms and continued proof of successful case studies will be key in 2026. Successful scaling will require custody integration. Trusted custodians (banks, for example) could expand their services to handle not just crypto but tokenised traditional assets, providing insurance and reporting that institutions require.

The Institutional DeFi Stack

While 2025 showed that the pieces of an ecosystem to establish institution-friendly DeFi exist, 2026 will be about putting them together into a usable stack. We anticipate progress on several fronts: identity and compliance layers for DeFi, direct integration of banks and traditional infrastructures, and enhanced risk management tooling.

KYC-embedded DeFi

One major development will be the proliferation of KYC-gated smart contracts. Instead of purely permissionless pools open to anyone, we may see more DeFi pools where every participant’s wallet is verified. Using primitives like soulbound tokens or the ERC-725 token standard, institutions can whitelist wallets that have undergone KYC/AML checks. In 2026, blue-chip DeFi platforms like Aave and Compound could launch lending and trading pools specifically for banks, hedge funds and accredited investors (this is already seen with platforms like Maple Finance and Ondo). These pools will maintain the transparent and programmable nature of DeFi but with participant criteria.

Projects such as Polygon ID, Chainlink’s DECO, Fireblocks’ off-chain verification tools are enabling this by letting users prove identity attributes to contracts without revealing private data onchain. The result could be, for example, a syndicated loan market onchain where only KYC’d institutional lenders can participate and borrowers’ identity is known to facilitators even if not public. By tackling the compliance requirements head-on, these gated systems aim to make traditional finance players comfortable interacting with DeFi protocols.

Bank integration and onchain finance

Another exciting frontier is connecting banks directly to DeFi rails. Notably, as part of Project Guardian in Singapore, DBS Bank and JPMorgan simulated FX and bond trades on modified versions (for compliance purposes) of Aave and Uniswap. In 2026, such pilots will expand and some could go live in limited fashion. For example, we could see a bank-led trading platform that uses an automated market maker (AMM) under the hood but with a bank front-end and compliance controls. Some large banks might integrate stablecoin usage into their core banking apps (for instance, allowing customers to hold and transfer tokenised bank deposits or approved stablecoins seamlessly). Cross-chain and cross-platform integrations are also likely.

This requires backend integration and legal structuring, but the incentive is there: DeFi can offer better yields and 24/7 liquidity, which banks can package for clients if they solve the trust factor. Custodians and prime brokers will play a big role here, bridging between off-chain assets and onchain contracts.

Despite the tech readiness, a major question remains: will institutions actually jump in with real size? If in 2026 regulators give a nod (say, the U.S. SEC provides guidance that participating in permissioned DeFi lending is not forbidden, or EU regulators explicitly allow banks to use DeFi under MiCA compliance), we expect at least a few trailblazer institutions to publicly announce usage. Those proof points would be game-changing, opening the door for peers to follow.

The technical work is largely done and the heavy lifting in 2026 is coordination. This involves aligning regulators, getting legal clarity for participants and demonstrating to institutions that these systems are not only higher-yielding but secure and trustworthy. If accomplished, this will unlock a wave of new liquidity and use cases, blending the best of DeFi innovation with the scale of traditional finance.

Emerging Themes

Beyond the core focus areas, 2026 will likely introduce or accelerate several emerging themes that could shape new narratives and opportunities in the crypto industry. Below, we focus on two very interesting narratives: the intersection of crypto with AI, and the advent of derivative markets for real-world assets.

Crypto + AI convergence

The past year saw an explosion in interest in artificial intelligence (AI), and there’s growing recognition of synergies between AI and blockchain. In 2026, we expect to see more progress in autonomous AI agents using crypto rails. The idea is that as agentic AI systems proliferate, they will need a way to own and transfer value, pay for services and enter contracts without human intermediaries. Cryptocurrency is the natural financial layer for this because it’s digital-native and permissionless.

In 2026, we might see prototypes of machine wallets or protocols tailored for machine-to-machine payments. A standout example is the x402 protocol, an open standard developed by Coinbase and now supported by a foundation including partners like Cloudflare. x402 enables seamless, instant micropayments over the web (often in stablecoins like USDC) without accounts, subscriptions or human intervention. It acts as a chain-agnostic middleware layer, allowing AI agents to autonomously pay for API calls, data access, compute resources (e.g., per-second GPU rentals) or even agent-to-agent services. And it uses blockchain settlement for trust and finality.

Blockchains provide trust and audit trails for AI. For example, recording how an AI model was trained (to prove it wasn’t trained on copyrighted data) or using non-fungible tokens (NFTs) to authenticate AI-generated content are some application of this tech. While these use cases will still be early, 2026 could mark the start of real experiments. We may hear of collaborations between AI labs and crypto teams to manage AI agent interactions.

RWA Perps

One emerging institutional use case are RWA Perpetuals, which are perpetual futures for real-world references. For example, it could be a perpetual swap tracking the price of a U.S. Treasury bond or a commodity like gold, but settled in crypto. We already saw Chainlink partner with ApeX Exchange to launch tokenised treasury perps in late 2025, enabling synthetic exposure to TradFi assets.

This matters less as a new product category and more as evidence of liquidity infrastructure maturing around tokenised assets. Institutional adoption requires not just spot markets but derivatives, options, and structured products.

In 2026, more of these could appear, potentially including perp markets for stock indices, commodities, or credit spreads on decentralised venues like Hyperliquid and Lighter. If liquidity builds, it effectively means a parallel derivative market for traditional assets, operating 24/7 and globally accessible, which is quite a paradigm shift.

Why does this matter? For one, it increases crypto capital efficiency. Crypto holders can trade and hedge non-crypto risks without off-ramping. It also invites traditional investors who might want to use DeFi to get exposure to something like the S&P 500 over the weekend when traditional exchanges are closed. However, it will draw regulatory attention. Offering derivatives of securities or commodities ventures into regulated territory.

Conclusion

The foundations laid in 2025 in regulation, infrastructure and institutional participation gives plenty of reason for optimism heading into 2026. Clearer laws are reducing legal risks, new technologies are making the system safer and more efficient, and big players are bringing stability and liquidity. The industry is maturing, with crypto assets increasingly treated as a legitimate part of the financial ecosystem rather than a renegade fringe.

2026’s trajectory is clear for institutions that have already built the right infrastructure. The question isn’t whether tokenization scales, but which players have positioned themselves to capitalize on it. Regulatory clarity must translate into fair and consistent enforcement. If unexpected crackdowns or onerous rules emerge, momentum could stall. Crypto is no longer isolated from macro swings, so a sudden liquidity drain could test its new resilience. And the industry must continue to court institutional trust and public trust, which means delivering on promises (like DeFi efficiencies, or stablecoin reliability) and self-policing bad actors.

For AMINA, the message is clear. The market needs bridge infrastructure. Institutions that can operate with banking-grade risk management while executing at crypto-native speed. This isn’t a temporary arbitrage opportunity. It’s the permanent operational layer between traditional finance and digital asset rails.

The long-term trend of increasing maturity and utility seems intact. As long as stakeholders maintain focus on security, liquidity and prudent innovation, the crypto industry can approach 2026 with justified optimism. Cautious, yes, but optimism nonetheless that the trajectory is upward and forward.

Disclaimer

This document has been prepared by AMINA Bank Ltd. (“AMINA”) in Switzerland. AMINA is a Swiss licensed bank and securities dealer with its head office and legal domicile in Switzerland. It is authorized and regulated by the Swiss Financial Market Supervisory Authority (“FINMA”).

This document is published solely for educational purposes; it is not an advertisement nor a solicitation or an offer to buy or sell any financial investment or to participate in any particular investment strategy. This document is for publication only on AMINA website, blog, and AMINA social media accounts as permitted by applicable law. It is not directed to, or intended for distribution to or use by, any person or entity who is a citizen or resident of or located in any locality, state, country or other jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation or would subject AMINA to any registration or licensing requirement within such jurisdiction.

Research will initiate, update and cease coverage solely at the discretion of AMINA. This document is based on various sources, incl. AMINA ones, and was generated using artificial intelligence (“AI”). No representation or warranty, either express or implied, is provided in relation to the accuracy, completeness or reliability of the information contained in this document, except with respect to information concerning AMINA. The information is not intended to be a complete statement or summary of the subjects alluded to in the document, whereas general information, financial investments, markets or developments. AMINA does not undertake to update or keep current information. Any statements contained in this document attributed to a third party represent AMINA’s interpretation of the data, information and/or opinions provided by that third party either publicly or through a subscription service, and such use and interpretation have not been reviewed by the third party.

Any formulas, equations, or prices stated in this document are for informational or explanatory purposes only and do not represent valuations for individual investments. There is no representation that any transaction can or could have been affected at those formulas, equations, or prices, and any formula(s), equation(s), or price(s) do not necessarily reflect AMINA’s internal books and records or theoretical model-based valuations and may be based on certain assumptions. Different assumptions by AMINA or any other source may yield substantially different results.

Nothing in this document constitutes a representation that any investment strategy or investment is suitable or appropriate to an investor’s individual circumstances or otherwise constitutes a personal recommendation. Investments involve risks, and investors should exercise prudence and their own judgment in making their investment decisions. Financial investments described in the document may not be eligible for sale in all jurisdictions or to certain categories of investors. Certain services and products are subject to legal restrictions and cannot be offered on an unrestricted basis to certain investors. Recipients are therefore asked to consult the restrictions relating to investments, products or services for further information. Furthermore, recipients may consult their legal/tax advisors should they require any clarifications.

At any time, investment decisions (including, among others, deposit, buy, sell or hold investments) made by AMINA and its employees may differ from or be contrary to the opinions expressed in AMINA research publications.

This document may not be reproduced, or copies circulated without prior authority of AMINA. Unless otherwise agreed in writing, AMINA expressly prohibits the distribution and transfer of this document to third parties for any reason. AMINA accepts no liability whatsoever for any claims or lawsuits from any third parties arising from the use or distribution of this document.

©AMINA, Kolinplatz 15, 6300 Zug