AMINA Bank AG

AMINA Bank AG  AMINA UK

AMINA UK  AMINA Hong Kong

AMINA Hong Kong  AMINA EU

AMINA EU

Executive Summary

- Ethereum is the world’s most decentralised, permissionless computational layer with ETH at the heart of this ecosystem as its native cryptocurrency.

- Being the birthplace of DeFi, Ethereum houses some of the strongest crypto projects and has over $62 billion in total value locked.

- The historic approval of the US spot Ethereum ETFs cemented ETH’s position as a mainstream investable asset.

- With over 59% market share in the tokenization sector, leading tokenization projects are actively choosing Ethereum as their primary deployment layer.

- With sustained cash flow generation, growing institutional adoption and a vibrant ecosystem of applications, ETH provides a differentiated investment case that complements Bitcoin in a modern digital asset portfolio.

Introduction

Ethereum is the most significant step in the evolution of programmable money and decentralised compute since Bitcoin. It began as a bold idea to build a global computer. Today, it supports a fast-growing digital economy that handles complex financial products and decentralised apps (dApps) at scale. In this edition of The Bridge, we explore why ETH, Ethereum’s native token, stands out as a strong investment opportunity in 2025.

The Ethereum Landscape in 2025

Ethereum is the home of decentralised finance (DeFi). It is where DeFi became more than just theory. DEXes, lending protocols, yield aggregators, memecoins, decentralised physical infrastructure (DePIN) – it all began on Ethereum. It powered the DeFi Summer, the NFT Mania and served as inspiration for a flurry of L1s (like Solana and Avalanche) that followed its footsteps. It is also the birthplace of top NFT (non-fungible token) projects like the CryptoPunks, the Bored Ape Yacht Club and the Milady Maker. Today, Ethereum’s DeFi ecosystem has over $62.13 billion in total value locked (TVL), representing over 55% of the entire DeFi market.

May 2025 was particularly positive for the Ethereum community, with ETH rising by 40.84% and delivering its first positive month of the year. And what sparked this sharp rally? To understand the full picture, we need to look back. In February 2025, hedge funds were heavily short on ETH, as seen in their positions on ETH CME Futures.

This shifted by mid–April, when many of these funds began closing out their short bets. That move eased much of the selling pressure on ETH. Around the same time, two major developments added momentum. Ethereum completed its Pectra upgrade successfully. Shortly after, SharpLink Gaming announced a plan to accumulate $425 million worth of ETH. These events combined to drive ETH’s biggest monthly gain since November 2024. This reflected renewed investor confidence, boosting market sentiment, and reinforcing Ethereum’s position as the leading smart contract layer.

The Case for Permissionless Decentralised Computation

The case for decentralised, permissionless computing becomes clear when we take an honest look at the limits of traditional systems. Centralised platforms create single points of failure, censorship risks, and rent-seeking behaviors that extract value from participants. For instance, web2 giants can sometimes charge up to 30% on in-app purchases.

Ethereum was the first to tackle this by offering a decentralised, permissionless computing layer where anyone can run code for a fee, and the network’s built-in economic system keeps its participants honest. This spurred innovation, especially in finance, where entry barriers are high and removing middlemen brings clear advantages.

Hosting a Vibrant Ecosystem

Traditional businesses have multiple factors eating into profits: fees for middlemen, infrastructure costs, compliance burdens. Onchain models changed this. They shift core operations like payments, governance and value sharing into smart contracts. This drastically cuts costs. dApps give everyone from retail users to investors and institutions a way to benefit.

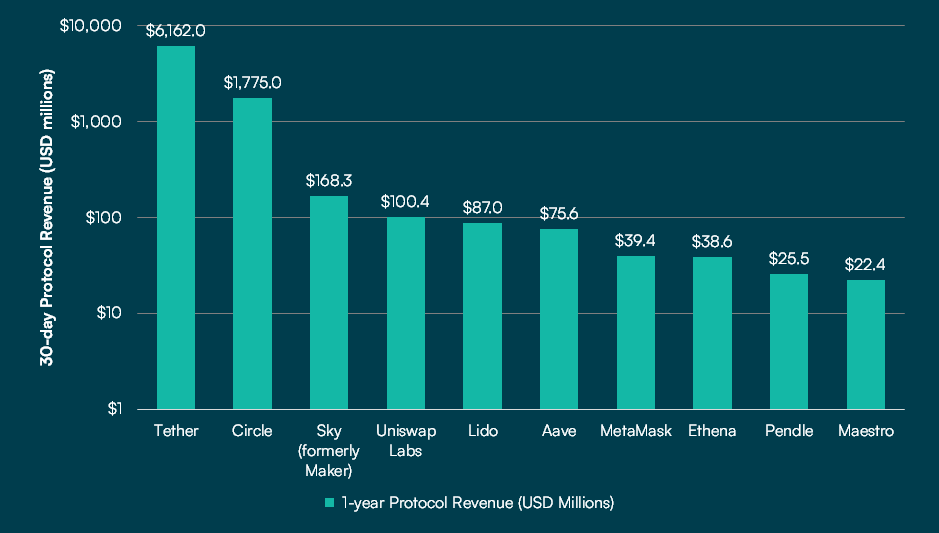

Today, Ethereum is home to some of the most popular dApps. It is an anchor network for major protocols. The network supports a long list of high-volume protocols: Tether’s USDT, Circle’s USDC, liquid staking platform Lido, the Uniswap DEX, the lending market Aave and more. Almost every DeFi primitive originated on Ethereum. From collateralised debt position (CDPs) protocols like Compound (the first one to introduce the concept onchain), to MEV solutions by Flashbots and more, Ethereum was the developer’s playground before other L1s followed. Ethereum brought opportunities for service providers as well. Wallet provider MetaMask, for example, was originally Ethereum-first and it has now evolved into one of the most widely adopted crypto wallets used by developers and users alike.

Figure 1: Top revenue-generating protocols on Ethereum

Source: AMINA Bank, DefiLlama (13 June 2025)

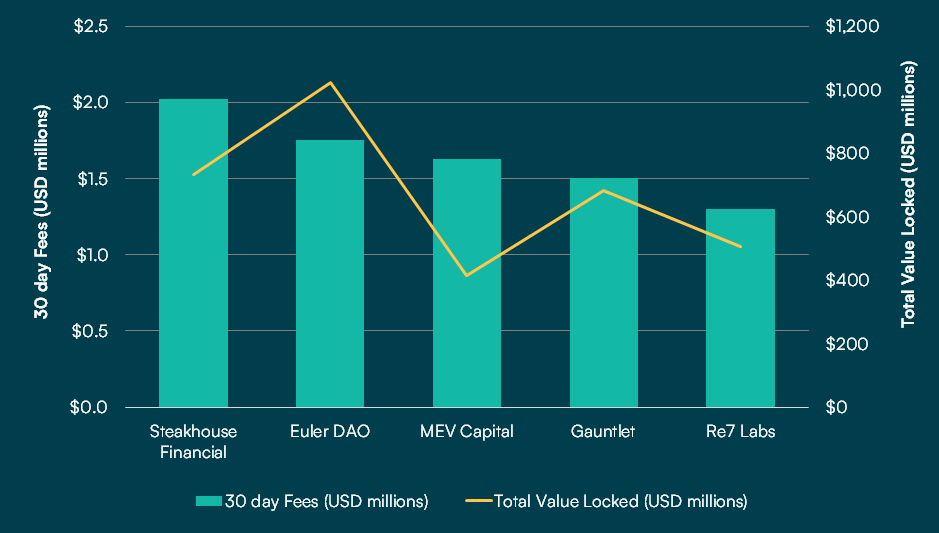

The network also pioneered the service provider industry in crypto. Alongside DeFi, we saw the spawning of specialised firms like Gauntlet (risk management and analytics) and Steakhouse Financial (DeFi advisory bringing TradFi expertise) which support crypto project operations. Such players earn millions servicing an industry hungry for niche talent. The chart below showcases some of these numbers that indicate strong demand for risk curation services onchain.

Figure 2: Highest earning DeFi protocol risk curators

Source: AMINA Bank, DeFi Llama (13 June 2025)

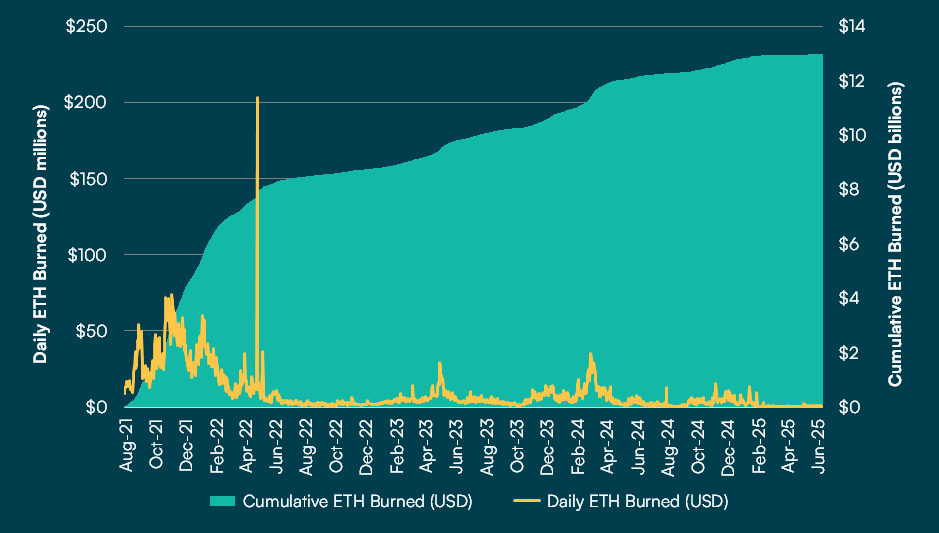

The more useful apps that run on Ethereum, the more activity they create. Every transaction includes a base fee which isn’t paid to validators but is permanently removed from circulation. As more apps grow and attract users, they use more gas. This leads to more ETH being burned over time, gradually reducing its total supply.

At the time of writing, close to $13 billion in ETH have been burned. Over time, this steady burn has (and continues to) put downward pressure on ETH supply while demand for block space continues to go up. This can be considered analogous to a share buyback program for traditional companies. The more Ethereum is used, the more ETH gets burned and as a result, more value flows back to holders.

Figure 3: ETH Burn post EIP1559

Source: AMINA Bank, Glassnode (13 June 2025)

ETH: The Smartest Play in Digital Assets?

Ethereum currently stands as one of the strongest investment opportunities in crypto. Earlier this year, Solana drew attention with strong activity, capturing 52% of DEX volumes in January. But since then, Ethereum has regained its lead. This comeback shows the strength of its core infrastructure and its ability to stay ahead in the long run.

Recent leadership changes at the Ethereum Foundation (EF) too have helped build confidence in the project’s direction. From its new leadership structure to the establishment of the Silviculture Society (to guide internal decision making), the EF has strongly signaled to the developer community that they remain grounded in its original cypherpunk ideals.

Regulatory Clarity

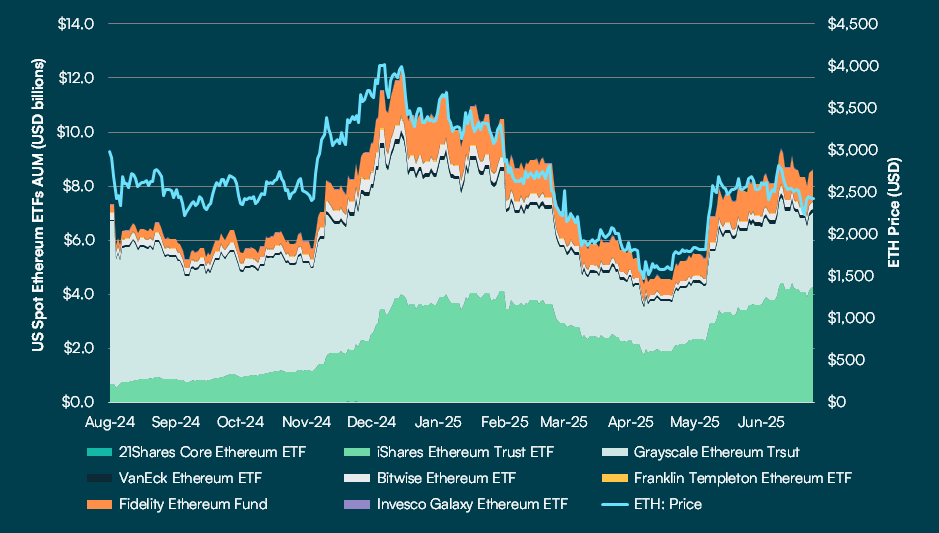

For almost ten years, Ethereum grew in the shadow of regulatory uncertainty. That picture has now changed. Just like it was for Bitcoin, the launch of the US Ethereum ETFs was historic for ETH. A year post launch, these spot ETFs in the US currently have combined assets under management (AUM) of over $9.3 billion and cumulative trading volumes have exceeded $85 billion as of 13 June 2025. This helped cement ETH’s position as a mainstream investable asset alongside BTC.

Figure 4: Spot Ethereum ETF AUM

Source: AMINA Bank, Glassnode (13 June 2025)

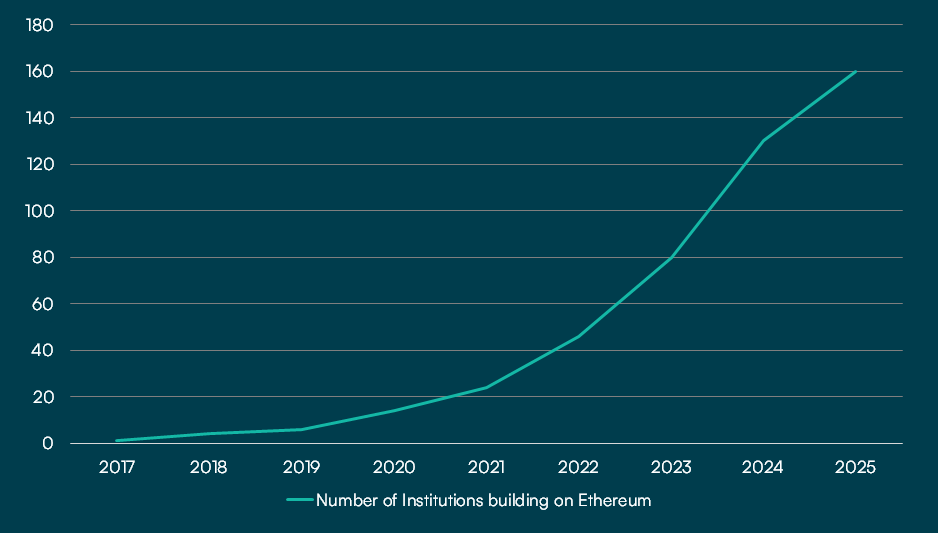

It’s not just investors, even traditional businesses are joining in. Shopify’s partnership (with Coinbase and Stripe) to bring stablecoin payments to merchants, Deutsche Bank’s ZKsync partnership to launch its own Memento ZK Chain, Stripe’s stablecoin payments product for businesses and Visa’s partnership with Bridge (to bring stablecoin-linked cards to the masses) are a few examples. These web2 giants are building atop Ethereum’s base layer infrastructure. Currently, over 160 institutions are building on Ethereum, ultimately driving economic value to ETH.

Figure 5: The number of institutions building on Ethereum currently stands at 160

Source: AMINA Bank, EthereumAdoption.com (13 June 2025)

Tokenizing RWAs

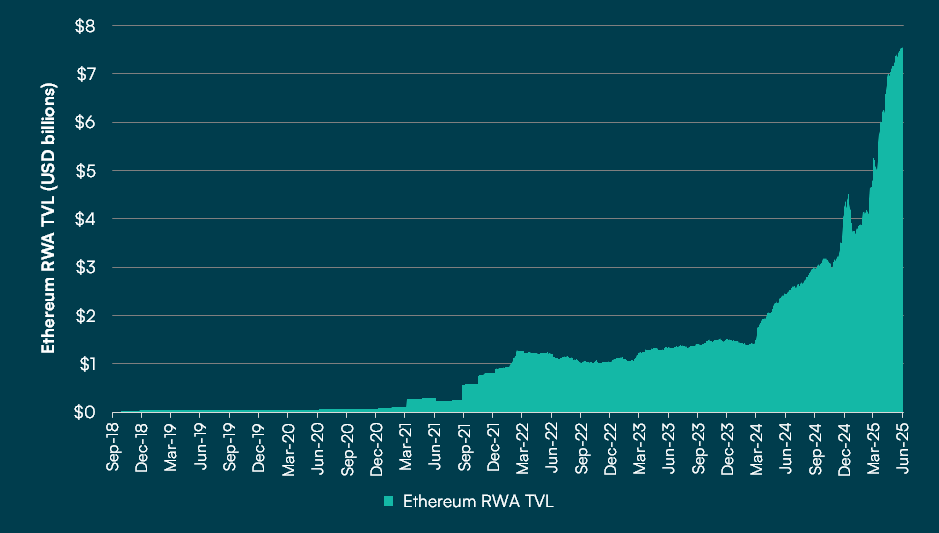

From treasuries to private credit, leading tokenization initiatives are actively choosing Ethereum as their deployment layer. More than $7.43 billion (roughly 59%) of all tokenized non-stablecoin real world assets (RWAs) including treasuries, credit markets, and yield-bearing funds, have been issued on Ethereum.

Figure 6: Total onchain RWA value stands at over $7.43 billion for Ethereum

Source: AMINA Bank, RWA.xyz (13 June 2025)

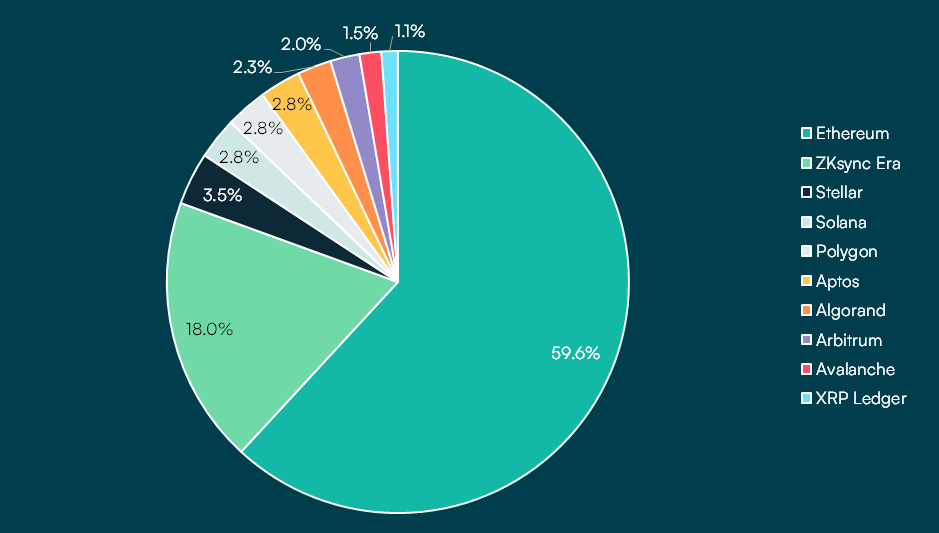

Figure 7: Ethereum dominates the onchain RWA market across blockain networks with a 59.58% market share

Source: AMINA Bank, RWA.xyz (13 June 2025)

Future Roadmap

Over the next few years, upgrades like the Scourge, the Verge, and the Purge will focus on fairness, decentralisation and reducing technical complexity. And the long-term vision for Ethereum? The Beam Chain. This brings key changes like simplifying validator operations, supporting massive L2 growth through advanced data availability solutions, and reducing reliance on full nodes.

Ethereum is transitioning from the Beacon Chain to the proposed Beam Chain, a redesigned consensus layer to support long-term scalability and efficiency. This transition will occur incrementally over 4-5 years (2025-2029). All this to make one thing possible: making Ethereum the de facto settlement layer of the global financial system. And one avenue to capture this growth? ETH.

Conclusion

ETH presents a compelling asymmetric upside. If BTC is digital gold, ETH is digital oil. ETH is the native asset of the world’s most decentralized, permissionless computational layer. With sustained cash flow generation and a vibrant ecosystem of applications, ETH provides an investment case that complements Bitcoin in a digital asset portfolio. Ethereum offers investors something unprecedented: programmable, yield-bearing money backed by the world’s most decentralized, permissionless computing platform.

—

Disclaimer – Research

This document has been prepared by AMINA Bank AG (“AMINA”) in Switzerland. AMINA is a Swiss bank and securities dealer with its head office and legal domicile in Switzerland. It is authorized and regulated by the Swiss Financial Market Supervisory Authority (FINMA).

This document is published solely for educational purposes; it is not an advertisement nor is it a solicitation or an offer to buy or sell any financial investment or to participate in any particular investment strategy. This document is for distribution only under such circumstances as may be permitted by applicable law. It is not directed to, or intended for distribution to or use by, any person or entity who is a citizen or resident of or located in any locality, state, country or other jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation or would subject AMINA to any registration or licensing requirement within such jurisdiction.

No representation or warranty, either express or implied, is provided in relation to the accuracy, completeness or reliability of the information contained in this document, except with respect to information concerning AMINA. The information is not intended to be a complete statement or summary of the financial investments, markets or developments referred to in the document. AMINA does not undertake to update or keep current the information. Any statements contained in this document attributed to a third party represent AMINA’s interpretation of the data, information and/or opinions provided by that third party either publicly or through a subscription service, and such use and interpretation have not been reviewed by the third party.

Any prices stated in this document are for information purposes only and do not represent valuations for individual investments. There is no representation that any transaction can or could have been effected at those prices, and any price(s) do not necessarily reflect AMINA’s internal books and records or theoretical model-based valuations and may be based on certain assumptions. Different assumptions by AMINA or any other source may yield substantially different results.

Nothing in this document constitutes a representation that any investment strategy or investment is suitable or appropriate to an investor’s individual circumstances or otherwise constitutes a personal recommendation. Investments involve risks, and investors should exercise prudence and their own judgment in making their investment decisions. Financial investments described in the document may not be eligible for sale in all jurisdictions or to certain categories of investors. Certain services and products are subject to legal restrictions and cannot be offered on an unrestricted basis to certain investors. Recipients are therefore asked to consult the restrictions relating to investments, products or services for further information. Furthermore, recipients may consult their legal/tax advisors should they require any clarifications.

At any time, investment decisions (including whether to buy, sell or hold investments) made by AMINA and its employees may differ from or be contrary to the opinions expressed in AMINA research publications.

This document may not be reproduced, or copies circulated without prior authority of AMINA. Unless otherwise agreed in writing AMINA expressly prohibits the distribution and transfer of this document to third parties for any reason. AMINA accepts no liability whatsoever for any claims or lawsuits from any third parties arising from the use or distribution of this document.

Research will initiate, update and cease coverage solely at the discretion of AMINA. The information contained in this document is based on numerous assumptions. Different assumptions could result in materially different results. AMINA may use research input provided by analysts employed by its affiliate B&B Analytics Private Limited, Mumbai. The analyst(s) responsible for the preparation of this document may interact with trading desk personnel, sales personnel and other parties for the purpose of gathering, applying and interpreting market information. The compensation of the analyst who prepared this document is determined exclusively by AMINA.