AMINA Bank AG

AMINA Bank AG  AMINA UK

AMINA UK  AMINA Hong Kong

AMINA Hong Kong  AMINA EU

AMINA EU Abstract

This article fulfills two objectives. First, it analyses the historical performance of gold amidst major crises and draws parallels with bitcoin’s response to the current situation. Second, it spots similarities between current and historical fundamentals when bitcoin had found a local bottom.

Introduction

While the second largest economy in the world was busy fighting the coronavirus, the US stock market was making new all-time highs, utterly unconcerned about the havoc wreaked by the virus in the other part of the world. Soon, the virus made inroads into the West and markets began to tumble. The fall was steep, as if markets had hit a wall. Everything fell as if there was no future.

To eradicate the virus, governments have taken drastic measures that are essentially leading to the shutting down of the world economy, as The Economist shockingly illustrated in its 19 March edition: Planet earth is shutting down.

The Coronavirus has caused unprecedented economic and financial shocks. Never in human history has a shock been so swift, violent and global. The shock has been so severe that it has dragged all assets in its wake, including supposedly safe assets such as gold and bitcoin.

To get an initial grasp of the magnitude of the shock, one needs to realise that one week of activity is equivalent to 1.9% of GDP (100%/52 weeks). In other words, based on this crude metric, one week of shutdown is equivalent to a GDP loss of 1.9%. And to give some context, advanced economies grew by 1.7% last year according to the IMF.

The cumulative cost of an extra week grows exponentially as the very survival of many companies is seriously impaired. Chinese industrial production fell by 13.5% in the first two months of the year.

To lessen the economic and financial costs, governments have launched huge fiscal stimuli. In the US for instance, President Trump signed a USD 2 trillion stimulus, about 10% of GDP. It is the largest stimulus of modern history – or put differently, it is at best just five weeks of GDP!

In this issue, we analyse the coronavirus asset price action in the light of a selection of historical sell-offs to gain an insight into bitcoin’s behaviour. We also portray how some of the current bitcoin fundamentals resemble conditions pertaining to previous bitcoin bottoms.

What has happened in the markets?

In the recent crash, the independence of bitcoin relative to other assets has been challenged as it dropped by more than the S&P500 index. Many are tempted to conclude by saying the diversification argument does not hold anymore. We have a different opinion, and this article is about why we think bitcoin remains attractive in the portfolio context.

Despite the uniqueness of the current situation, history offers parallels that help us better understand financial market behaviours in periods of acute stress and what we can expect once the shock is absorbed.

Gold's behaviour in past crises

We analyse three examples of financial stress with a focus on gold, an asset revered as a classic diversifier and one that is close in spirit to the notion of outside money, of which bitcoin is part. We presented this in the previous Digital Investor: Bitcoin is dead, long live bitcoin.

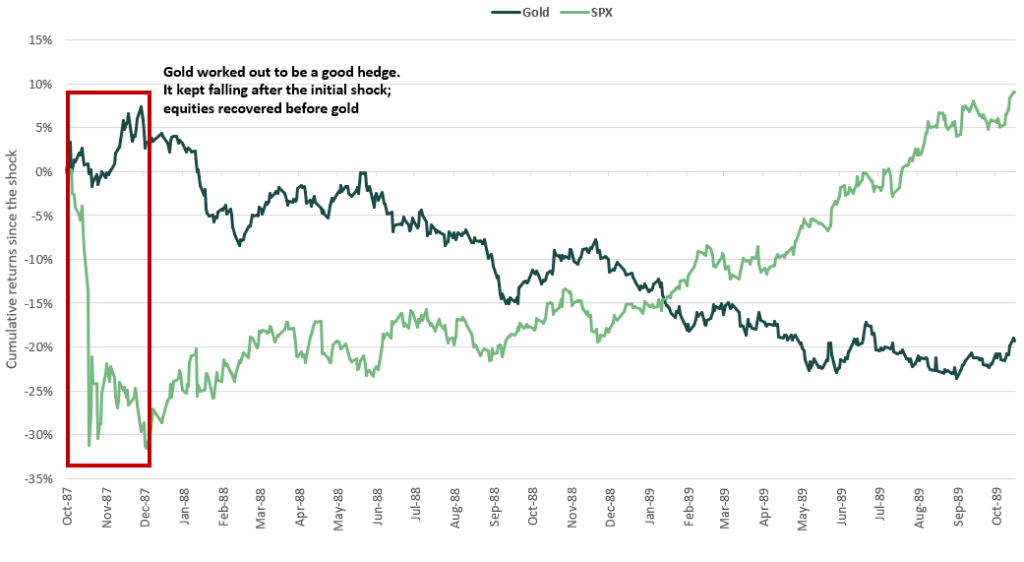

Black Monday, Oct 1987

Figure 1: Black Monday (gold remained a hedge throughout)

In this case, during the initial phase gold rallied as equities fell, and when equities started recovering, gold fell again. Gold worked as a hedge around the Black Monday crisis.

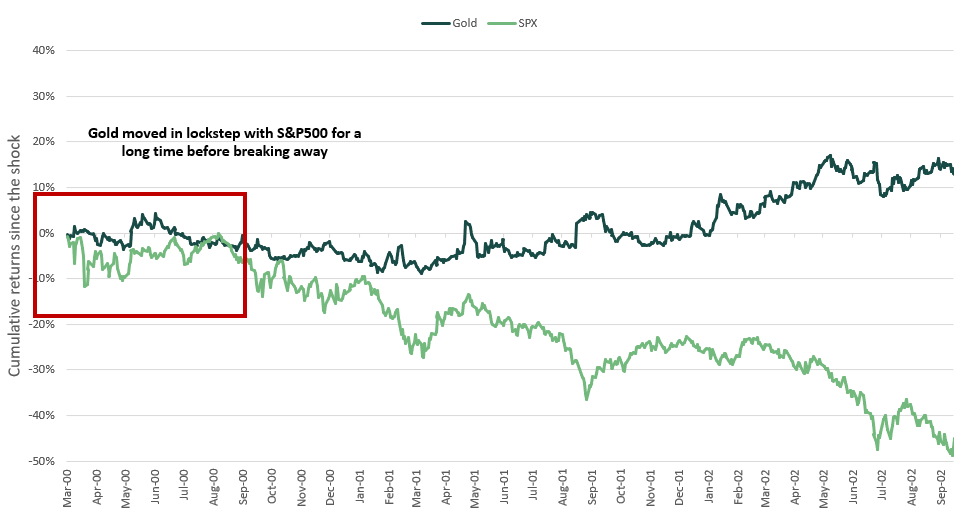

Dot-com bubble burst, 2000-2002

Figure 2: Dot-com bubble (gold moved in lockstep with equities before breaking away)

During the dot-com bubble burst, though gold behaved as a hedge at the beginning, it also had periods of extremely high correlation with equities.

Global financial crisis, 2007-2008

Figure 3: Global financial crisis (gold followed the same directional pattern as equities)

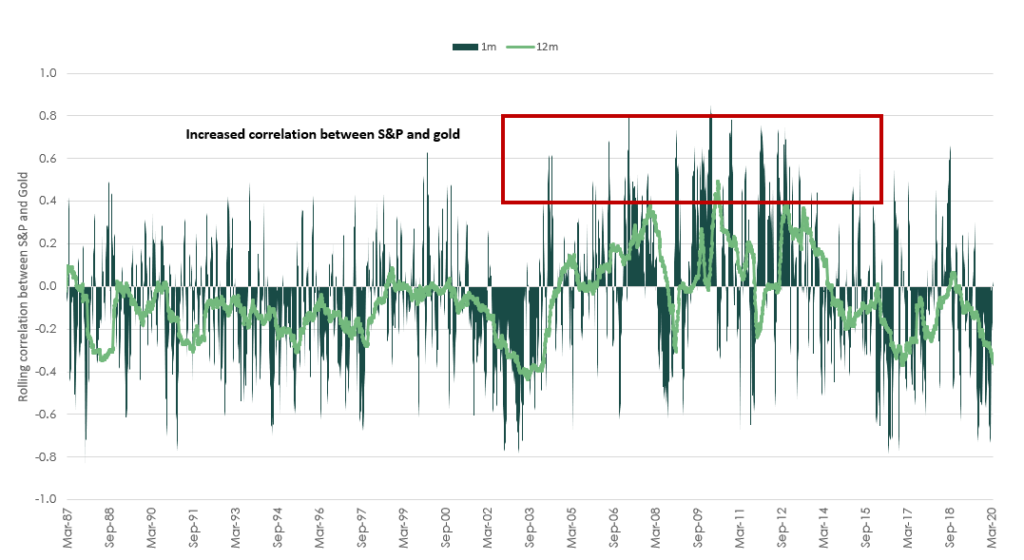

Gold performed differently in the three crises. Gold’s correlation with S&P saw sharp spikes during crisis periods, however, over the longer term, there are no doubts regarding gold’s position as a diversifier. Over the past 30 years, the correlation1 between gold and S&P500 averages -0.05.

Figure 4: Rolling correlations of S&P vs gold

COVID-19 crisis

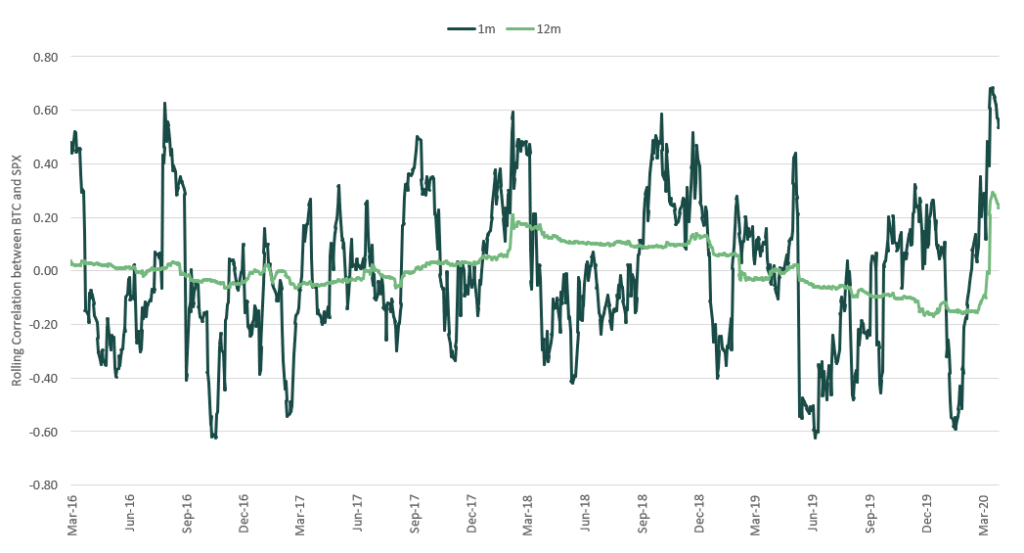

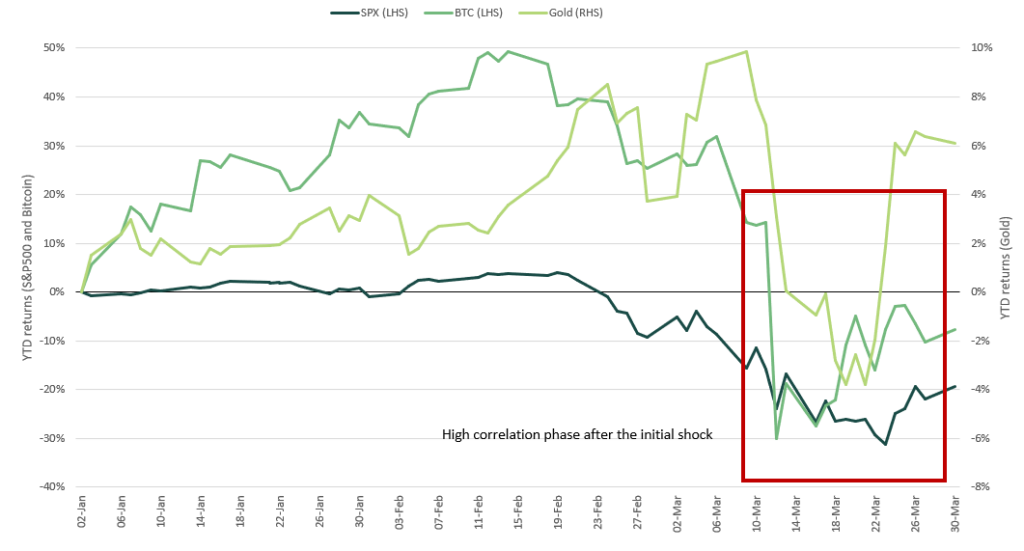

Bitcoin was born after the global financial crisis (GFC) and is now experiencing its first global crisis. When the crisis hit, we observed a typical flight to liquidity as investors sold everything they could. Crypto-investors seem to have acted accordingly. This article shows that the sell-off was driven by short-term holders, which could mean that it was driven by leveraged retail investors or institutions. As we can see in figure 5, the 1 month and 12 month rolling correlations between bitcoin and SPX shot above 0.65 and 0.25 respectively, the first time in both cases.

Figure 5: Rolling correlations of BTC vs S&P

We think that one of the major reasons for the correlation spike is the rate at which markets fell. To put this in context, we looked at historical crises. As shown in figure 6, the rate at which markets have fallen during the current crisis is unprecedented. S&P registered the top on 19 February and it fell by 30% in 19 working days versus 40 days for Black Monday, and almost a year for the GFC. The rapid fall illustrates how surprised markets were and the reading of this chart underscores the sense of panic that lead investors to sell what they could, resulting in high correlations among asset classes.

Figure 6: Comparison of S&P 500 performance during major crises

We think that cryptocurrencies fell more than other broader markets because of multiple factors. Governments intervene in traditional markets by employing various methods such as circuit breakers, rate cuts, repo facilities, commercial papers, bailouts, helicopter money and so on. Cryptocurrencies have none of these.

The aforementioned measures reduce the pain in the short term. In our view, they affect the price discovery mechanism and do not let the free markets do their job. The actual problem is only masked and the inevitable is just delayed, not avoided.

Figure 7: Performance of different assets during the COVID-19 crisis

Our analysis shows that this phase of high correlation could be an exception over the long-term trend. Just like gold, bitcoin is also a form of outside money, a type of asset that is the liability of nobody and cannot be manipulated by anyone.

After the recent sell-off, the correlation has shrunk. This behaviour is similar to what we have observed with gold and S&P 500 during the dot-com bubble burst. Therefore, dismissing that bitcoin offers diversification based on short bursts of high correlation is not a good strategy in our view.

Analysis of previous bitcoin bottoms

Now, if the correlation is shrinking, does it mean bitcoin has bottomed at around USD 3,800? We can only make an educated guess whether the bottom is already in. We look at the history of bitcoin bottoms and try to draw parallels from fundamental perspectives.

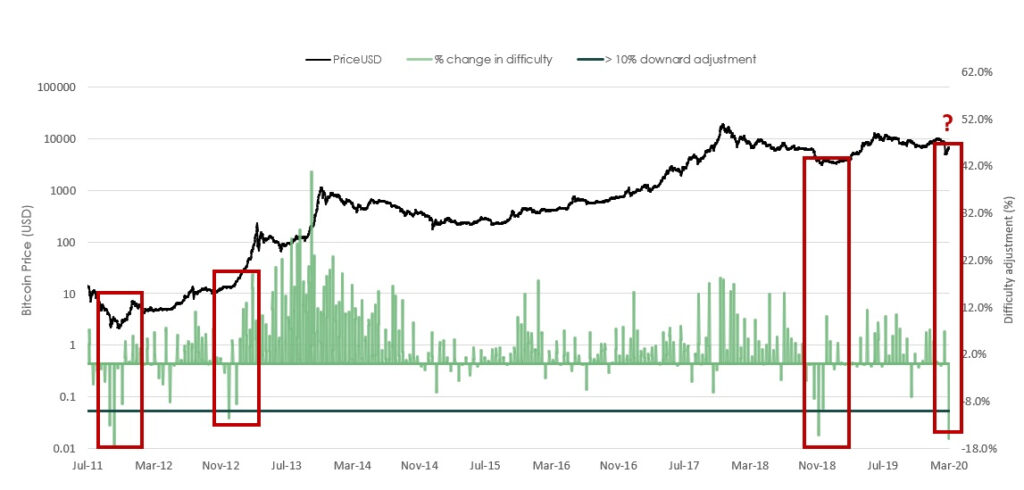

One of the best things about bitcoin is arguably its difficulty adjustment algorithm2, which is a self-stabilising mechanism. The difficulty is adjusted about every two weeks. If more miners are plugged in, i.e. the hashrate is increasing, the difficulty increases and vice-versa.

Downward difficulty adjustments of higher magnitudes have historically marked local bottoms for bitcoin. On 26 March, the difficulty adjusted downwards by 16%, making this the second-largest drop in history. Reduced difficulty demands less energy, thereby reducing the cost of mining bitcoin and increasing miners’ profitability. As a result, more miners join, and the hashrate climbs again.

Typically, the hashrate drops after sudden drops in prices as marginal miners start running losses. This is what happened after the recent price crash as well. The hashrate, a measure of mining activity, dropped to about 75 million TH/s from about 100 million TH/s. After the difficulty was adjusted, the hashrate jumped back to 111 million TH/s, signalling strong support by the miners.

Figure 8: Bitcoin bottoms (difficulty adjustment vs price)

Stablecoin market cap shows that space is far from dead

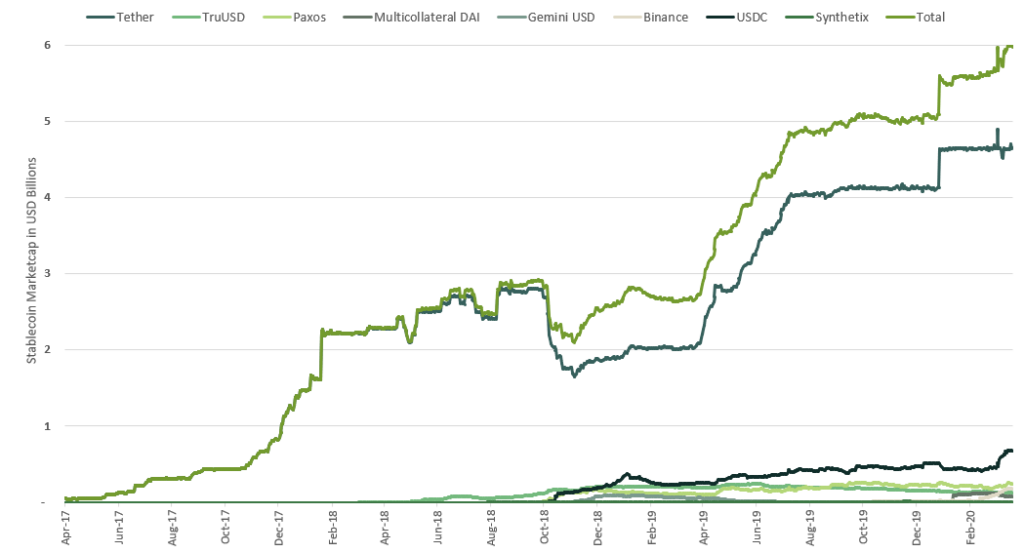

The market capitalisation of stablecoins has been increasing steadily. In 2020 stablecoins saw a steady rise of 20%, and during the recent sell-off, the demand for stablecoins has remained solid. Stablecoins offer easy convertibility into other cryptocurrencies compared to fiat on-ramps.

Stablecoins are built on top of existing blockchains. The growing demand for stablecoins gives us confidence that space is, in fact, thriving.

Figure 9: Stablecoin market cap shows steady growth

Conclusion

Observations of gold’s performance as outside money in the past few crises suggests that measuring correlation or diversification over a short period is not wise. Bitcoin’s design allows it to continue operating in phases where the price drops drastically.

The outside money characteristics of bitcoin coupled with bitcoin’s ability to continue to operate in phases where the price remains low, and unaffected demand for stablecoins even after the recent crash suggest that the long-term future of the field is intact.

Does this mean that we know for certain that bitcoin is going to bounce regardless of what happens to other asset classes? Absolutely not. Only it is premature to conclude that diversification does not work. Bitcoin had been pronounced dead 380 times before the recent crash by prominent personalities. This will be bitcoin’s 381st death, and it will be resurrected for the 381st time.

11 month rolling correlation ↵

2For every 2,016 blocks, bitcoin adjusts the difficulty at which blocks can be mined. If 2,016 blocks are mined sooner than the anticipated time of two weeks, the difficulty is adjusted higher and vice-versa. For more details, please refer to Mining: The essence of proof of work (https://aminagroup.com/research/Mining-the-essence-of-proof-of-work/) ↵