AMINA Bank AG

AMINA Bank AG  AMINA UK

AMINA UK  AMINA Hong Kong

AMINA Hong Kong  AMINA EU

AMINA EU Abstract

Our analysis shows that increased bitcoin mining equipment efficiency has reduced the time it takes to breakeven, even at lower bitcoin prices. Sensitivity to operational conditions such as bitcoin price and electricity cost has been reduced at the cost of increased capital expenditure. Investors should bear in mind that despite the attractiveness of acquiring bitcoin at a cheaper-than-market cost, bitcoin mining has many nuances and is a full-time business. Our discounted cash flow analysis shows that starting a bitcoin mining business may be a lucrative decision at this stage.

Introduction

Bitcoin mining has come a long way since it launched in 2009. The cumulative revenue from bitcoin mining as of 4 August 2020 was just shy of USD 19 billion, with approximately USD 2.8 billion in revenue to date in 2020 alone. As bitcoin mining becomes increasingly sophisticated, our article investigates the viability of a mining business in the future. To do that, we first examine the development of mining profitability since the industry’s inception.

The first section of this article analyses how the mining industry has evolved to tackle high sensitivity to bitcoin price. In the second section, we present different ways of gaining exposure to bitcoin mining. Finally, the last section of the article examines the viability of a bitcoin-mining business using discounted cash flow analysis.

Why should investors care about bitcoin mining or the hashrate of the bitcoin network?

Investors who are long on gold tend to explore ways to gain exposure to gold mining. Similarly, investors who are long on bitcoin have begun to explore ways to gain exposure to the hashrate of the bitcoin network, as hashrate measures mining activity. Note that hashrate also indicates how secure a blockchain is; a higher degree of security increases the value of bitcoin (BTC). The higher the hashrate, the costlier it is to attack the network.

How did we get here?

In the early days of bitcoin, you could mine bitcoin on any computer. Those who mined a block received 50 BTC as a reward. Bitcoin is a proof of work system; probabilistically, those who put in the most work receive reward. As bitcoin began to gain traction, miners devised more efficient ways of mining bitcoin, meaning that everyone had to work harder to obtain the same number of bitcoins. As stated in our piece Digital Investor – Bitcoin halving: The battle of hard and soft money, bitcoin halvings occur approximately every four years. Mining efficiency needs to double to ensure that profitability remains the same (ceteris paribus). GPU mining replaced CPU mining1, the latter was replaced by FPGA mining2. The first ASIC3 mining machine was launched by Canaan in 2013 and had a 130-nm chip. Recent ASICs have a chip size of approximately 7 nm4. As some miners employed specialised machines to mine bitcoin, others had to evolve as well. Increasing efficiency meant not only improving mining machines but also optimising operations to keep costs in check. Thus, hobbyists lost their share to sophisticated miners. New ways of mining rendered the old ways obsolete, and the entry barrier for solo miners grew.

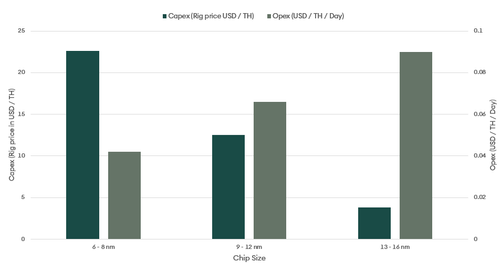

BTC is often the only source of miners’ income. As operational expenditure (Opex) is in fiat currencies, miners are heavily reliant on BTC price to continue supporting the bitcoin network. Gradually, mining equipment manufacturers and miners have optimised equipment and operations to reduce price sensitivity. As a result, capital expenditures (Capex) have increased and operational expenditures have decreased as shown figure 1.

Figure 1: Decrease in operational expenditure at the cost of increasing capital expenditure

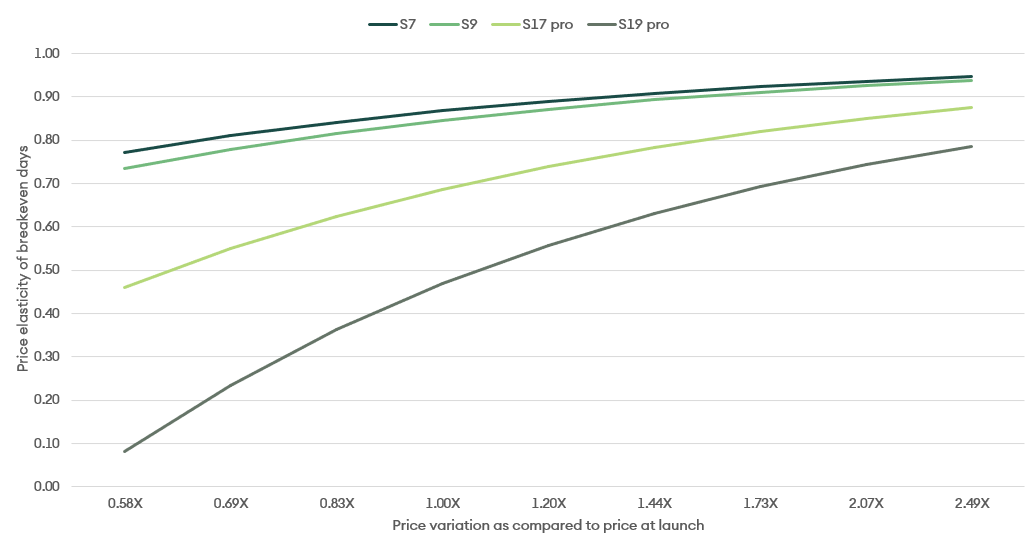

As bitcoin price volatility is detrimental to miner revenue, the mining industry has made efforts on all fronts to reduce the sensitivity of BTC price, endeavouring to make the break-even on capital and operational expenditure as early as possible. To understand how mining equipment has evolved over the years, we need to examine how the sensitivity of break-even days to bitcoin price has evolved with new equipment. We consider four benchmark pieces of mining equipment—Bitmain’s S7, S9, S17 pro, and S19 pro—and analyse the sensitivity around the launch of all four series. Interested readers can see the calculations used for this exercise in the Appendix..

What interests us in this Digital Investor is the relationship between break-even days (BED) and the price of bitcoin for different generations of equipment. Figure 2 presents this sensitivity with an elasticity of BED to price.

Figure 2: Price elasticity of break-even days

As can be observed in Figure 2, newer equipment’s price elasticity of breakeven days is lower than that of earlier generations, indicating that newer-generation machines are less sensitive to price. This finding is observable for any price. For any given technology, the higher the price is relative to where it is at launch, the more sensitive it becomes meaning the breakeven is achieved quickly. Intuitively, if the price of BTC doubles the day after launch, BED is achieved much more rapidly than before. However, if price declines immediately after launch, it takes more time to achieve break even, but the sensitivity is less. The reason is that the operational break-even price of bitcoin for new-generation machines is lower than that of older-generation machines.

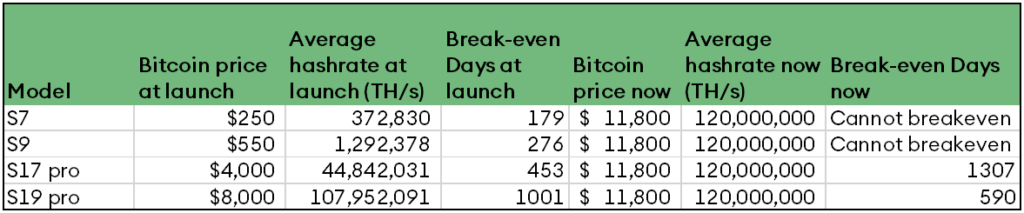

In the last column of Figure 3, we see that in the current environment (hashrate and price as of August 2020), only the newest generations of equipment survive. This result reveals both the competition pressure miners feel and why miners are forced to upgrade technology regularly to optimise their operations. The result also indicates that mining is becoming an industry where only well-organised, large players survive.

Figure 3: Break-even days for different equipment at launch and today

Ways to gain exposure to bitcoin mining

Having sufficiently established how bitcoin mining equipment has changed over the years, we next discuss how investors can gain exposure to bitcoin mining.

- Equity route The easiest way for traditional investors to gain exposure to bitcoin mining is to go through stocks of companies involved in the mining business. Some of the listed players include mining companies such as HIVE Blockchain Technologies, Hut 8 Mining, Marathon Patent Group, etc. as well as mining equipment manufacturers such as, Canaan, and NVIDIA, among others.

- Hashrate futures A more specific way to gain exposure to hashrate or bitcoin mining activity is to use hashrate futures offered by some of the exchanges. For example, FTX has quarterly Futures that settle based on average difficulty during the quarter.

- Cloud mining Investors can buy hashrate using cloud mining. In this case, the hosting company provides the infrastructure for investors. Investors are paid according to their shares in the mining operations. Though it is a convenient way to gain exposure to hashrate, this route has been used by fraudulent companies to swindle investors in the past and, therefore, is not a recommended way to gain exposure to mining.

- Mining bitcoin Mining bitcoin allows investors to remain in control and tweak mining conditions as and when required. It remains the cleanest way to gain exposure to bitcoin mining but requires constant oversight.

Mining as a business

Now that we understand the journey, we can explore the viability of the mining business using an example based on the current environment.

The first question to answer is why anybody should bother mining bitcoin when you can simply buy bitcoin at market price. For investors who are bullish on bitcoin in the long term, mining does allow them to acquire bitcoin at a price that is cheaper than market price. For example, at the time of writing this, bitcoin price is approximately USD 12,000. However, the cost to mine bitcoin as per our assumptions (total hashrate = 130 nm TH/s; 96% utilisation; electricity cost = USD 0.06 per kWH) is approximately USD 6,500. Thus, the mining business currently allows investors to acquire bitcoin at roughly a 45% discount. (See Part A of the Appendix of this article for details about our assumptions.)

Bitcoin mining has three major drivers: electricity cost, capital expenditure (purchase of machines and set-up costs), and bitcoin price. For our example, we performed discounted cash flow (DCF) analysis on a bitcoin mining business for a 36-month time horizon (the expected lifetime of a machine) with initial capital expenditure of USD 1 million.

Performance of the mining business

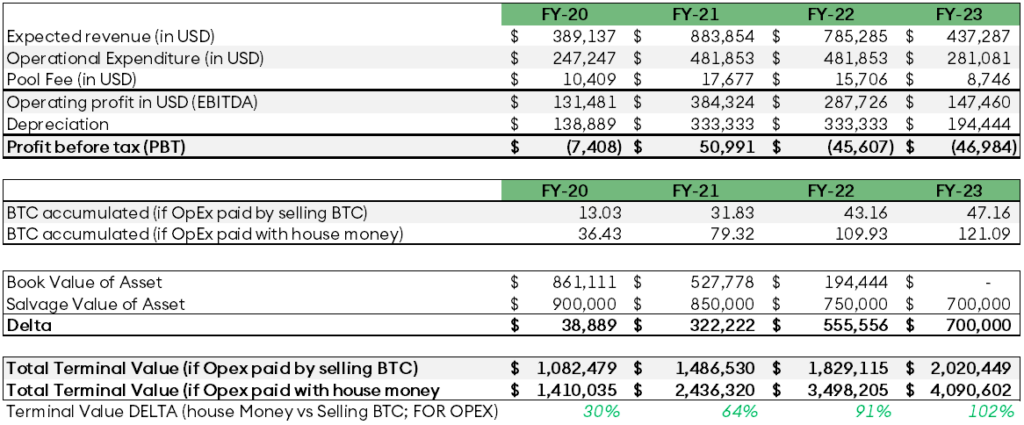

For the given assumptions (again, detailed in the appendix), net present value (NPV) is highest if the business is terminated at the end of the tenure (in this example, 36 months). This assertion is subject to change if the business environment changes. For example, if BTC price is not as high as assumed, NPV may reach a maximum earlier than anticipated. Figure 4 shows the results of our calculation.

Figure 4: NPV, EBITDA, and Salvage Value

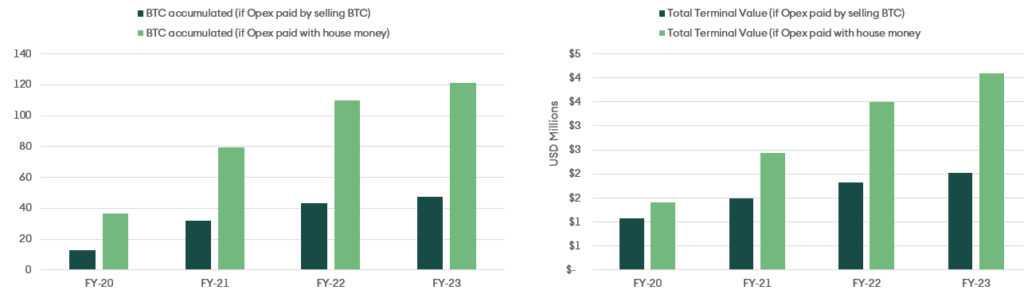

Opex can be covered either by selling earned BTC or through existing cash. Both strategies are prevalent among miners. However, if the assumption is that BTC price will have an ascending trajectory, using existing cash to pay for running costs make more sense.Figures 5 and 6 compare cash flow and terminal value changes resulting from different opex strategies.

Figure 5: Cash flow and terminal value difference with different Opex strategies

Figure 6: Differences in total BTC accumulated and in terminal value with different Opex strategies

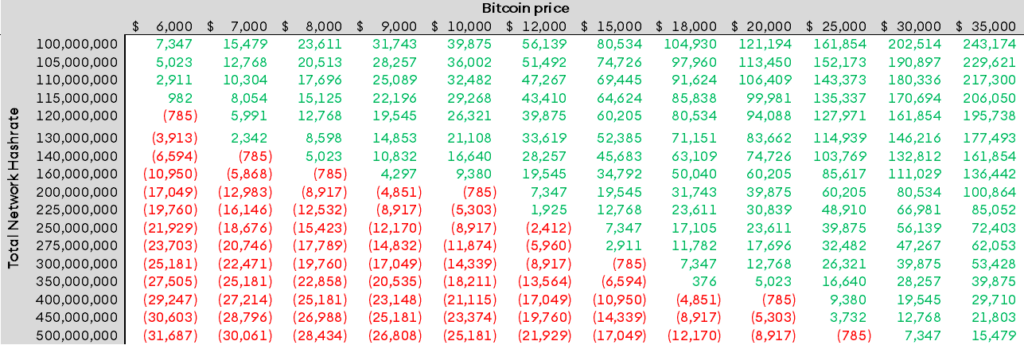

At the current-day total network hashrate, monthly operating profit is calculated to be approximately USD 33,600. Figure 7 demonstrates how a business’ monthly operating profit changes when the total network hashrate and the bitcoin price change.

Figure 7: Monthly operating profit sensitivity analysis based on bitcoin price and total network hashrate

For the given set of assumptions, the mining business example appears to be viable even if the hashrate grows rapidly and the bitcoin price grows moderately.

Business defensibility

As stated earlier, mining simply allows investors to acquire bitcoin at a cost cheaper than the market price. Though the number of break-even days is less sensitive to bitcoin price than earlier, price does have a significant impact on the business.

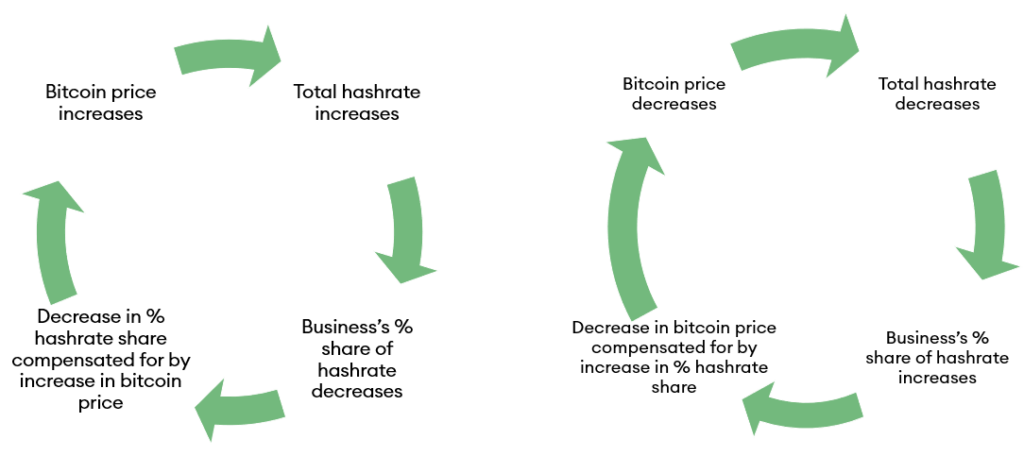

The share in total network hashrate determines the profitability of a mining business. Thus far in the example, we have assumed that the hashrate of the business remains constant. Two possibilities emerge: the total hashrate increases or the total hashrate decreases. What happens in each case?

The total hashrate increases significantly

The total network hashrate tends to increase exponentially in lockstep with the price. Therefore, it is likely that significant increases in price will drive up the total hashrate. In a case where the business’s share of the total hashrate increases, an increase in bitcoin price makes up for the fallen share of total hashrate. For example, if both bitcoin price and the hashrate double to USD 24,000 and 260 million TH/s, respectively, the monthly operating profit of the business remains at approximately USD 33,000.

The total hashrate decreases significantly

When bitcoin price drops, miners with high operating costs due to higher electricity costs are forced to halt their operations. As a result, the total hashrate drops and the remaining business’s share of total hashrate increases.

For example, if bitcoin price drops by 50% to USD 6,000 and the total hashrate drops by 50% to 65 million TH/s, monthly operating profit remains intact.

Figure 8: Mining business defensibility

Risks

Bitcoin mining is a full-time business. There are many nuances that investors should be aware of and pay attention to, including selecting a mining pool, negotiating electricity contracts, choosing the geographical location of the facility, and more. If investors are not prepared to allot full-time attention to a bitcoin-mining business, there are other routes to consider, such as hashrate futures or dollar-cost averaging in bitcoin itself.

If bitcoin price does not increase significantly, it can be difficult to recover the capital expenditure.

As has happened in the past, disruption in mining-equipment manufacturing can usher in new-generation mining equipment that has the potential to make the current generation of equipment obsolete5.

Conclusion

Bitcoin mining has become a sophisticated industry over the years. Miners and equipment manufacturers have managed to reduce reliance on price and electricity costs to a certain extent. Given the current environment, our analysis indicates that bitcoin mining could be a lucrative business for the next three years.

Appendix: Part A - Assumptions

The assumptions used in our example analysis are as follows:

- No machine upgrades for the duration and no new capital expenditures. Therefore, as the total hashrate increases, the mining business’s share in the total hashrate decreases; thus, revenues fall over time.

- Financial Year (FY) is the same as Calendar Year.

- Straight line depreciation for 36 months.

- Calculation of the discount rate: The beta in this example is the average adjusted beta of Canaan, Hut 8, and Riot. The risk-free rate is the average of the United States’ and China’s 10-year bonds, as the majority of bitcoin mining takes place in China and as there has been a gradual shift from China to the United States. Similarly, risk premium is the average of the equity risk premiums of the United States and China. With these assumptions, we arrive at a discount rate of 8.61%.

- In our hashrate projection, we assume elevated growth at the beginning of the time period and a slowdown as time passes. The rationale for this assumption is that new-generation machines were launched recently by various mining equipment manufacturers and chips are already at the 6-8 nm range. To reduce chip size further will become increasingly difficult. There will need to be a breakthrough for the hashrate growth to sustain the momentum. Bitcoin halving took place recently; miners tend to upgrade equipment after the halving and then wait for significant improvements in machines before upgrading again.

- Growth rate is conservative so that the total hashrate beats the hashrate estimated by hashrate futures.

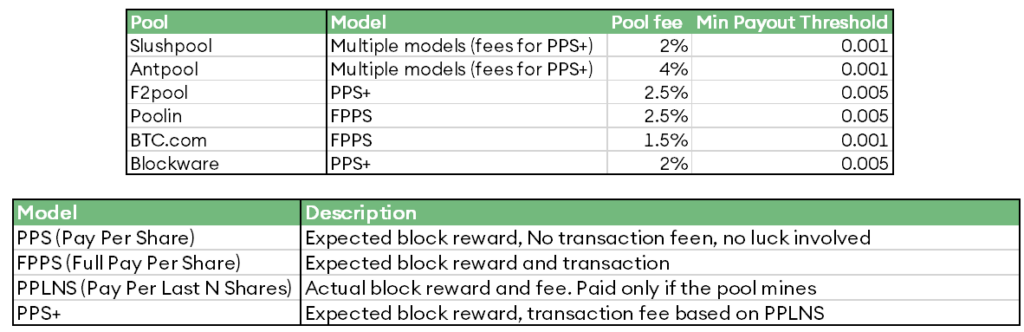

- The decision to choose a mining pool depends on various factors, ranging from a pool’s location to the different pay-out methods used by pools. A miner with sufficiently large operations can choose not to join a pool. However, for a smaller miner, joining a pool offers steady rewards. Different pools and their pay-out methods are listed in figure 9. In our example, we assume that the miner joins a pool with a 2% fee.

Figure 9 – Mining pools and their payout methods

- 100-day moving average (since halving) of fee revenue as a percentage of total issuance is approximately 8%. To be conservative, transaction fee revenue is assumed to be 6% of revenue from block rewards.

- Electricity cost is assumed to be USD 0.06 per KWH.

- Machine ratings = 3.25 kW; 110 TH/s; 96% utilisation; total number of machines = 286.

- Cost of one S19 pro chip is assumed to be USD 3,490, which is about 40% premium above the price listed on Bitmain and approximates the average price quoted by variousdistributors. The set-up cost is assumed to be approximately USD 50,000 per MW. For 286 machines, the set-up cost is USD 46,475.

- Average bitcoin price for FY20 = USD 14,000, FY21 = USD 20,000, FY22 = USD 25,000, and FY23 = USD 28,000.

- Salvage value of the equipment for FY20 = 90%, FY21 = 85%, FY22 = 75%, and FY23 = 70%. These are conservative estimates as the salvage value of mining equipment has been more than 100% on occasion.

Appendix: Part B - Calculation of Price elasticity of Break-even Days (BED)

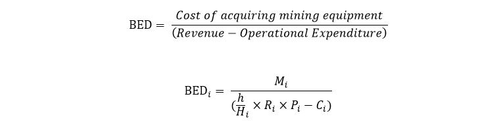

In general, break-even days (BED) can be defined as follows:

where H = total hashrate, h = miner’s hashrate, R = BTC reward, P = BTC price, M = Capex, and C = Opex. The subscript i denotes time at which new-era mining equipment was launched.

Taking the partial derivative with respect to price:

Price elasticity to break-even days can be calculated as follows:

1GPU stands for Graphical Processing Unit. GPUs are better at performing dedicated tasks repeatedly compared to CPUs. ↵

2FPGA stands for Field Programmable Gate Array. FPGAs have more on-chip cache memory that reduces latency compared to GPUs. FPGAs are more power-efficient compared to GPUs. ↵

3ASIC stands for Application Specific Integrated Circuit. As the name suggests, ASICs are designed for specific purposes. For example, ASICs designed for bitcoin mining are extremely good at bitcoin mining but cannot perform other functions. ↵

4The smaller the chip size, the greater the efficiency. ↵

5Historically, just over two years elapse before the appearance of equipment that demonstrates any material improvement over equipment released after a halving. The most recent halving occurred on 11 May 2020. ↵