AMINA Bank AG

AMINA Bank AG  AMINA UK

AMINA UK  AMINA Hong Kong

AMINA Hong Kong  AMINA EU

AMINA EU Executive Summary

- High inflation and a tight labour market force the Fed to maintain a hawkish stance

- Global liquidity conditions have deteriorated as major central banks have raised rates and the US dollar appreciated

- High correlation between cryptocurrencies and traditional assets shows that they react to the same data, i.e., macro and global liquidity

- According to our central scenario, global liquidity will not improve soon as inflation is above the central bank’s target level and the labour market is robust. As a result, we keep a cautious stance on crypto, as we have had for several months

- In crypto, our preference remains for blue-chips cryptos, namely BTC and ETH

- The Merge went through successfully and smoothly on 15 September 2022, preparing the Ethereum network for the future

- Bitcoin’s hash rate reached an all-time high putting the miners under pressure

- DeFi tokens and alternative network coins performed poorly, with the cryptocurrency market capitalization losing over USD 80 billion in September

Introduction

Historically, September has not been the best month for growth assets, and this year was no different. Bitcoin price ended the month 4% lower than it started, while Ether fell by more than 15%.

The correlation between the S&P500 and the cryptocurrency market has remained elevated. It shows that both traditional and crypto markets react to similar macroeconomic developments.

In the crypto verse, The Merge was the highlight of the month. Having gone through it successfully, many in the space consider it a historic event for the industry. The Merge transitioned Ethereum from Proof-of-Work to Proof-of-Stake with more than a 99% reduction in energy consumption to run the network. Traders FOMO’ed into Ether before the transition, and the price rallied, leading to the Merge. It resulted in a sell-the-news behaviour, and Ether fell by 5% on the day of The Merge and continued to drift lower during the month.

Table 1: Performance of AMINA Bank universe coins as of 12 October 2022

Macroeconomics

According to the latest report, unemployment rates in the United States fell to 3.5% in September, lower than expected (3.7%). At the same time, payrolls rose by over 260,000 during the month. In conjunction with high inflation and the indication of a tight labor market, the expectation of a Fed pivot has been postponed again according to market-implied rate hike expectations. The Fed fund rate has increased five times this year to 3.25%, and more tightening will come.

Global monetary conditions are tightening as all major central banks are raising rates. The direct consequence has been a massive repricing of the bond market. The most shocking development occurred in the UK, where the Gilt market was on the brink of collapse, forcing the Bank of England (BoE) to intervene. In late September, bond yields rose by more than 100 basis points due to anticipated interest rate hikes, unfunded tax cuts, and an abrupt depreciation of the British pound. UK Pension funds struggled to raise cash to meet margin calls and started selling gilts.

The yield on 30-year bonds soared 68 basis points MoM. On 27 September, it spiked 76 points, the highest one-day increase in history. The BoE stepped in to avert a financial market collapse and said it would buy up to GBP 65 billion bonds, with a limit of GBP 5 billion daily.

Bitcoin’s correlation with traditional financial markets remained elevated, signaling Macro’s importance in both markets. The 30-day correlation with the NASDAQ stood at 0.77, and with S&P500 stood at 0.75 as of 1 October 2022.

Global liquidity conditions have deteriorated with the rise of interest rates, the repricing of the equity risk premium, and the strengthening of the dollar to its highest level in more than two decades.

Cryptocurrencies are frontier assets and are sensitive to global liquidity conditions. According to our central scenario, we expect these conditions to weigh further on cryptocurrencies and keep a cautious stance. For several months, we have maintained a general careful stance towards cryptocurrencies and prefer Bitcoin and Ethereum over other coins.

Bitcoin (BTC)

In contrast to the volatile stock, credit, and currency markets, bitcoin has remained remarkably stable in recent weeks. This is rare for Bitcoin and is usually followed by a sharp rally or significant decline. According to our central scenario, the probability of another correction increases in the coming weeks.

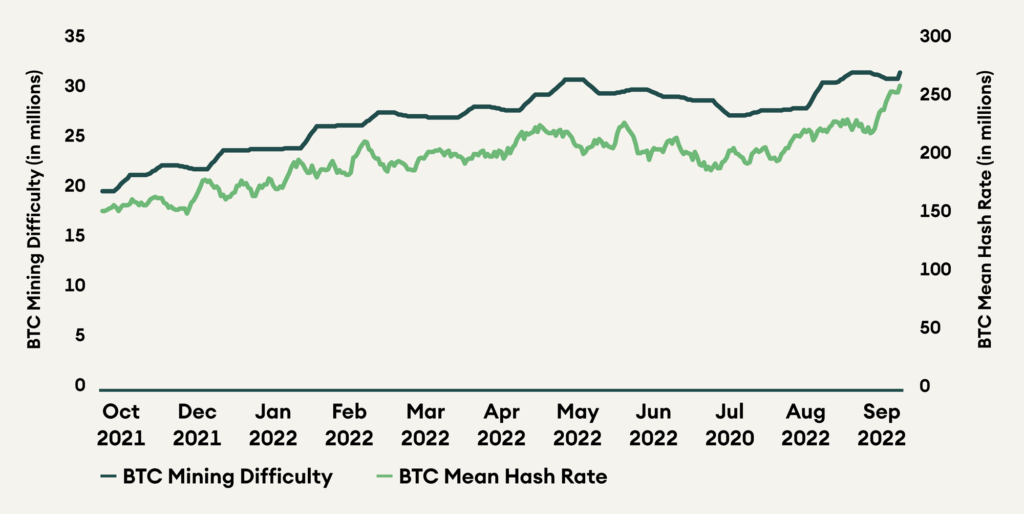

Since May 2022, the value settled on the Bitcoin Network has declined, signaling lower activity and demand for the digital asset. The network is holding up well because the hashrate has reached a new all-time high, adding security to the system and indicating the strong commitment of the miners’ community.

According to Glassnode, Bitcoin hashrate has reached a new all-time high. As a result, the revenue earned per hash, a proxy for miners’ income, has trended downward to reach an all-time low. Said differently, the cost of mining has increased, and it is currently about USD 19.7k per Bitcoin, according to external sources. Since the bitcoin price is trading at USD 19k, miners are producing at a loss. This increases selling pressure as miners are forced to sell Bitcoins to cover their running costs.

Figure 1 – Bitcoin Hash Rate and Mining Difficulty

Recent developments in the Lightning Network (LN) are ambivalent. On the one hand, its capacity has increased and is now over 5k BTC, a 6% MoM increase, but on the other hand, the number of nodes and channels has decreased since their respective peaks in March this year (from 20k nodes to 17k nodes and from 87k channels to 86k channels).

A study of the correlation between realized price and bitcoin supply in profit shows that bitcoin may be in a late bear market as hodlers are not moving their funds. Historically, this situation signaled that the market was close to an inflection point.

In summary, challenging macroeconomic conditions, low global liquidity, and mixed on-chain activity data make us cautious about Bitcoin. However, there are indications that the bear market is extended, and any improvement could lead to a relief rally.

Ethereum (ETH)

Ether’s price trajectory looks like a rollercoaster in September as it ended up 15% lower than it started despite a 17% increase in the first few days of the month. This volatile behavior is the result of The Merge.

In a typical buy-the-rumors, sell-the-news pattern, traders participating in the speculation activity surrounding the hype exited before The Merge on 13 September 2022. The sell-the-news activity drove prices way lower than where the rally started, USD 1,250 and USD 1,400, respectively.

The crypto community celebrated The Merge by issuing the first-ever PoS NFT, which represents a time capsule of the moment The Merge occurred. This NFT bore the iconic panda face and was sold for 36 ETH soon after. People also created a Merge-inspired illustration of a large, slowly forming Ethereum logo supported by scientists.

However, The Merge is the first step in the network upgrade process. According to Vitalik Buterin, The Merge brought Ethereum to 55% completion, meaning there is more to come.

The next upgrade will be the Shanghai Upgrade, allowing network’s validators to withdraw a portion of their staked Ether and rewards. Staked Ether and rewards are currently worth over USD 19 billion. This upgrade will also lower transaction costs on layer two chains like Optimism and Arbitrum by reducing data costs on the main chain.

Later, other upgrades will take place– the Surge, the Verge, the Purge, and the Splurge – ultimately leading Ethereum to full completion. According to Vitalik Buterin, when all five phases of upgrades are complete, Ethereum will process up to 100,000 transactions per second at a low cost.

Development in the Ethereum network is dynamic, and if all the upgrades are implemented reasonably, Ethereum is likely to strengthen its position as a top layer one solution. The current macroeconomic conditions affect Ether as any other cryptos. However, the long track record of the network and its popularity and vitality make it an attractive asset, in our opinion.

Polkadot (DOT)

The Polkadot network architecture allows parachains to interoperate with each other, enabling cross-blockchain transfers of any information or asset. A cross-consensus message (XCM) is required to do so, and this has spurred growth within the ecosystem, increasing parachain adoption. In addition to this, parachain auctions continue successfully through this bear market. Each of these auctions leads to locking up more DOT for two years, reducing the DOT supply in circulation.

Also, recently, Tether announced that they would be integrating with Polkadot by launching USDT stablecoin support for the ecosystem. USDT being the largest stablecoin by market capitalization, this partnership will push growth on the network.

Challenges in front of the team are mainly regarding competition, marketing, and user experience. Cosmos, Avalanche, Polygon, and Solana are the biggest competitors to Polkadot as alternative chains, and they are growing bigger. User experience is probably the most critical concern, and the Polkadot interface is not appealing to many. Chains like Solana and layer 2’s like Arbitrum offer top-notch user experience. If DOT wants to compete in the space, the user experience will need to be a priority for its developers.

Stellar (XLM)

Stellar rose by over 20% during the month, riding on the recent update, allowing users to send and receive XLM through email. Tildamail is a decentralized email and storage platform that recently integrated with the Stellar Lumens network. This functionality is a step forward in improving technological flexibility concerning cryptocurrencies and makes it easier for users to operate their native XLM coins.

Even though XLM price-performance was positive in September, the overall network health is not good. The ecosystem’s revenue is about USD 8k a month despite a 200% increase last month.

Looking at the distribution of coins, we observe that the entire locked supply (49% or 24 billion XLM tokens) is controlled by Stellar Foundation, raising severe concerns about its decentralization. These coins were minted at the genesis, and the foundation uses the tokens for the platform’s growth. Notice that the coins do not reward network participation since there is no node operating rewards, and the node count stands at 23.

Cardano (ADA)

On 23 September, the Cardano blockchain successfully deployed the Vasil hard fork. It improved Cardano’s transaction speed from 1tps (transactions per second) to 5 tps. The upcoming Hydra upgrade will increase the throughput of each staking pool to process 1,000 tps. This will scale the blockchain by reducing latency and increasing throughput.

Cardano recently deployed Initial Staking Pool Offerings (ISPO). The goal is to increase validator and user participation.

Cardano remains behind its competitors in terms of innovation and upgrade deployments. Its first-generation DeFi activity has not picked up while other blockchains are building for DeFi 3.0. The total value locked on Cardano fell by 75%, and the price of ADA fell by 50% since March 2022.

There are serious concerns that the network is unsuitable for DeFi or NFTs, considering it has a 20-second block interval and is slow presently.

Avalanche (AVAX)

Avalanche recently integrated with Boba Network – an Ethereum scaling solution – to increase its throughput on the C-chain. While this is positive for users, it shows a pivot in the team’s stance on a rollup-centric future. The Ava Labs team has publicly stood against rollups and prefer the subnets concept due to a few technical issues encountered in rollups. This move challenges the core fundamentals of Avalanche.

The user activity on the DeFi Kingdoms subnet has doubled over the past two months. It is also worth noting that in September, Avalanche tied up with Securitize to tokenize the private equity firm KKR’s Health Care Strategic Growth Fund II (HCSG II). The tokenization enables KYC-d investors to own a piece of the USD 4 billion healthcare-focused funds.

Avalanche’s fully diluted valuation stands at USD 13 billion, similar to companies like Reddit, Grammarly, and Airtable.

Solana (SOL)

Solana’s biggest strength is its NFT community, the second largest after Ethereum. SOL price shows a high correlation with ETH despite the very difference in the status of both these currencies. It is surprising as Solana is a new generation blockchain with repeated downtimes, while Ethereum is an established blockchain with a long track record.

Recently, Coinbase announced that users could access Solana Dapps using their Coinbase wallet. This is significant news for the Solana ecosystem and its participants since it reduces network friction.

Solana is known for reliability issues, as many downtimes mark its history. After three months without problems, a new downtime paralyzed the network for 3 hours on 30 September. There are also concerns regarding some applications, as some are closed source, leading to more vulnerability.

Litecoin (LTC)

For Litecoin, there has been a slow and gradual adoption of private transactions, which coincides with the ethos of cryptocurrencies. Also, its price has been close to its historical bottom since 2017. The long-term sustainability of the ecosystem is worrisome as most of the miner rewards on the network come from fresh issuance of USD 4 million per day. To go with this, it also has annual inflation of 3.41%. Both these factors weigh on the coin price.

Tezos (XTZ)

Tezos’ Kathmandu upgrade went live on 29 September 2022, bringing an optimistic rollup functionality to the network. While activity on Tezos remains low, it may be fundamentally strong since it has prominent players validating the network. For instance, 76% of the supply is staked by large validators like Binance, Coinbase, and Kraken.

As on-chain activity is low, a single play-to-earn NFT or gaming application can boost the token’s price due to the increase in daily wallets it would bring with it.

However, there are challenges before the network can grow. For starters, it is not EVM-compatible and so struggles to onboard developers into the space. As a result, the DeFi activity on Tezos is small, only 0.01% of that on non-EVM chains. In addition, whales have been steadily dumping the token, and their holdings are currently at the lowest levels they have been in the past three months.

Aave (AAVE)

Aave is a Defi blue-chip, continuously building new features. In addition to developing its social networking project, Lens Protocol, Aave is bringing reputation based NFTs via Orange Protocol. It is an exciting development as web3 identities could be a part of the next big thing.

Currently, there is a low demand for short-term leverage as speculative trading is modest. The Aave token offers limited utility except for governance and staking. It also faces competition from Compound Finance, which has recently launched its V2 that introduces single-sided liquidity and borrowing. Lastly, with the recent layer2 boom, borrowing and lending APY is extremely low on Aave, and so users presently prefer to farm GMX, LDO, or CRV rewards.

While AAVE price fell in line the with the market, there is a direct correlation between the Aave treasury and its market capitalization. The treasury fell by 90% from its ATH in March 2021 and AAVE price by 89%. When DeFi activity recovers, Aave treasury will grow, and so will its market cap. Aave is a blue chip DeFi token with most of the token emissions out already and is well positioned for the future, waiting for the next bull run.

Chainlink (LINK)

Recently, Chainlink made upgrades for the network and its token holders. Apart from Chainlink 2.0, the major announcement is the collaboration of Chainlink and SWIFT, the international payment backbone of traditional finance. They are developing interoperability standards called CCIP for the Cross Chain Interoperability Protocol. The goal is to use Chainlink to facilitate business interaction and communication across numerous chains by partnering with SWIFT. As a result, trading will be cheaper and faster, increasing further integration with traditional finance.

Staking for LINK tokens was also mentioned by the Chainlink team. The estimated APY on LINK is 5%, and the tentative date for betting LINK tokens is December 2022.

Uniswap (UNI)

The Uniswap community was mulling a proposal to turn on the fee switches on two widely used pools – the ETH/USDC pool and the USDT/USDC pools. While this would reduce the fees paid out to liquidity providers after the fee switch is switched on, the treasury value will increase, and so will the demand for UNI tokens.

However, UNI is currently a governance token with no value accrual, and the issue of impermanent loss has not yet been solved. It is to be seen how the team tackles this challenge to come out on top.

Yearn Finance (YFI)

Yearn finance’s TVL has been stagnant at USD 500 million in the past 30 days, and this might be a cause of concern since activity has remained low. Another cause of worry is that the realized market capitalization of long-term holders has declined, which may be signaling profit-taking behavior. In the list of liquidity pools with high TVL, Yearn Vaults rank at #92, which is lower than expected since it is considered a top DeFi protocol. Investors in the token need to pay attention since YFI is a low-liquidity token. Low liquidity tokens with higher volatility in subject to sharp price movements.

Synthetix (SNX)

There has been a low demand for SNX products – sUSD and sETH due to a decline in on-chain activity across blockchains. However, adopting perp and futures trading on platforms like Kwenta, 1inch, and Lyra Finance will boost demand for synths, increasing demand for SNX. These platforms could gain more users in the upcoming months since they facilitate trading on synthetic forex tokens, which might look attractive due to the macro environment and the current geopolitical scenario.

Conclusion

While the markets are moving sideways, innovation and development within crypto are on the rise. These innovations include

1. The development of interoperability protocols like CCIP, IBC, and XCM. These protocols allow transfer and communication between different blockchains.

2. The development of Byzantium, a new protocol that improves the security of blockchain networks.

3. The development of zero-knowledge proofs allows users to conduct transactions without revealing their identity or other information.

4. The development of blockchain-based identity management systems like Kilt and Litentry protocols on Polkadot.

5. The development of blockchain-based marketplaces like Sudoswap.

6. The development of blockchain-based voting systems like Snapshot.

7. The development of blockchain-based cybersecurity solutions.

8. The development of blockchain-based logistics solutions.

Cryptocurrencies are still in their early stages, and they are still subject to a lot of volatility. However, they are definitely worth watching.