AMINA Bank AG

AMINA Bank AG  AMINA UK

AMINA UK  AMINA Hong Kong

AMINA Hong Kong  AMINA EU

AMINA EU

Executive Summary

- In April, the crypto market witnessed significant events and developments across various fronts. Total crypto market capitalization declined by 16% over the month.

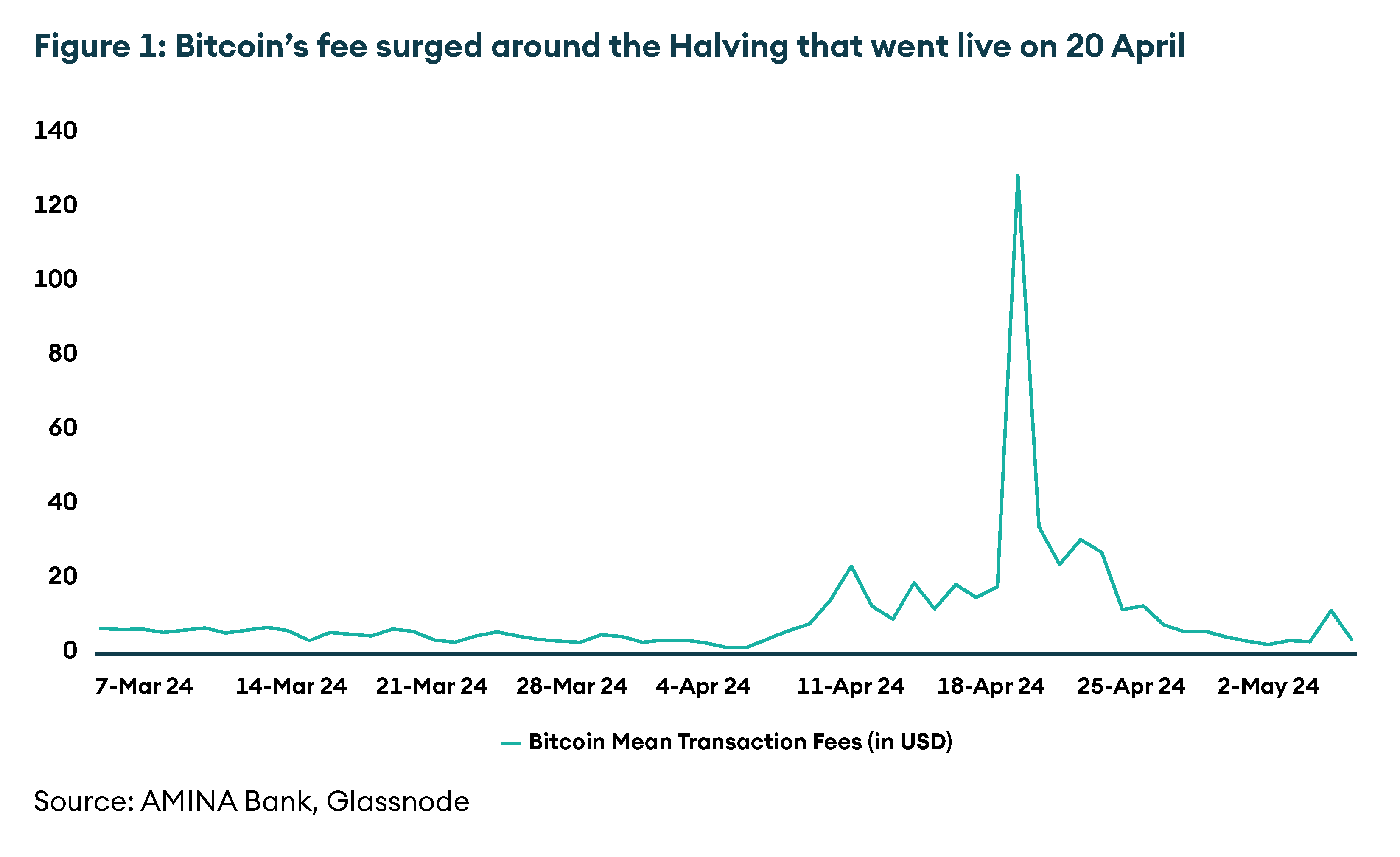

- Bitcoin’s fourth Halving event that occurred on 20 April led to a surge in transaction fees as demand for blockspace intensified, driven by the Runes upgrade.

- However, US spot Bitcoin ETFs experienced a noticeable decrease in inflows compared to the previous month, with industry giant BlackRock even encountering its first net outflow day.

- Ethereum’s ecosystem continued its robust growth, propelled by layer-2 solutions following the Dencun upgrade in March, which significantly reduced transaction fees.

- Solana maintained its position as the leading alt-layer 1 (L1) network, although it experienced congestion amid a frenzy of memecoin trading.

- Regulatory scrutiny also looms as the US SEC issued a Wells Notice to Uniswap in April.

- Looking ahead, historical trends suggest a potentially silent May for the digital assets market. We expect macroeconomic factors such as interest rates, consumer price index inflation and unemployment data to exert considerable influence alongside developments in bitcoin spot ETF flows, shaping market sentiment and price action.

Bitcoin

Bitcoin went through its fourth Halving on 20 April 2024 – an event that halves the miner block rewards every 210,000 blocks. The recent halving decreased the reward from 6.25 BTC to 3.125 BTC per block.

However, Bitcoin’s price plunged towards the end of the month, briefly dipping below the USD 57K mark. Post halving, the leading cryptocurrency is down 5.2% on the 30-day timeframe and is trading around the USD 64K mark.

The market saw a spike in transaction fees around the event due to increased demand for blockspace. This is because with the Halving, the network underwent the Runes upgrade that enable users to issue fungible tokens on the blockchain.

Runes offers improvements over the BRC-20 standard, notably reducing the creation of UTXOs and mitigating the issue of on-chain UTXO bloat or junk transactions.

While BRC-20 tokens are currently the predominant focus of inscription activity, the landscape could experience a rapid shift if Runes begins to gain traction and becomes the favored token standard within the Bitcoin community.

Runes could gain dominance on the Bitcoin network once demand is strong. This has been observed with Inscriptions in the past as they gained prominence and activity flowed in waves.

For instance, September 2023 saw Inscriptions accounting for over 58% of all transactions on the Bitcoin blockchain network – a level not seen since. As the market improves and we start to see more inflows into the Bitcoin ecosystem, this may repeat itself.

Investors can also expect Bitcoin-based solutions and decentralised finance (DeFi) to gain traction as the cycle moves further along. For example, just like EigenLayer kicked off the restaking narrative on Ethereum, Babylon is a protocol working to create Bitcoin staking.

This would allow BTC holders to share economic security with other networks in exchange for staking yield. Others include Stacks and Merlin which are building layer-2s on top of Bitcoin. Citrea is another scaling solution and is the first zero knowledge based L2 on Bitcoin.

Currently, according to L2 watch, the total number of Bitcoin solutions is almost 70. However, there’s a looming question on how Bitcoin Layer 2s compare with those from other L1 ecosystems, given its counterparts’ relative speed in adopting major protocol upgrades.

The US spot BTC ETFs are currently seeing limited inflows compared to March. BlackRock also recorded its first ever net outflow day in April.

The launch of Spot Bitcoin and Ethereum ETFs in Hong Kong also posted disappointing figures, with a mere $15 million in trading volume and $8.5 million in inflows on the first day. Amidst these disappointing developments, Greyscale’s GBTC spot bitcoin ETF witnessed its first ever net inflows day on 3 May.

However, the overall ETF flows have reduced, and market sentiments are neutral at best since the ETFs have driven the market narrative since their launch in January this year.

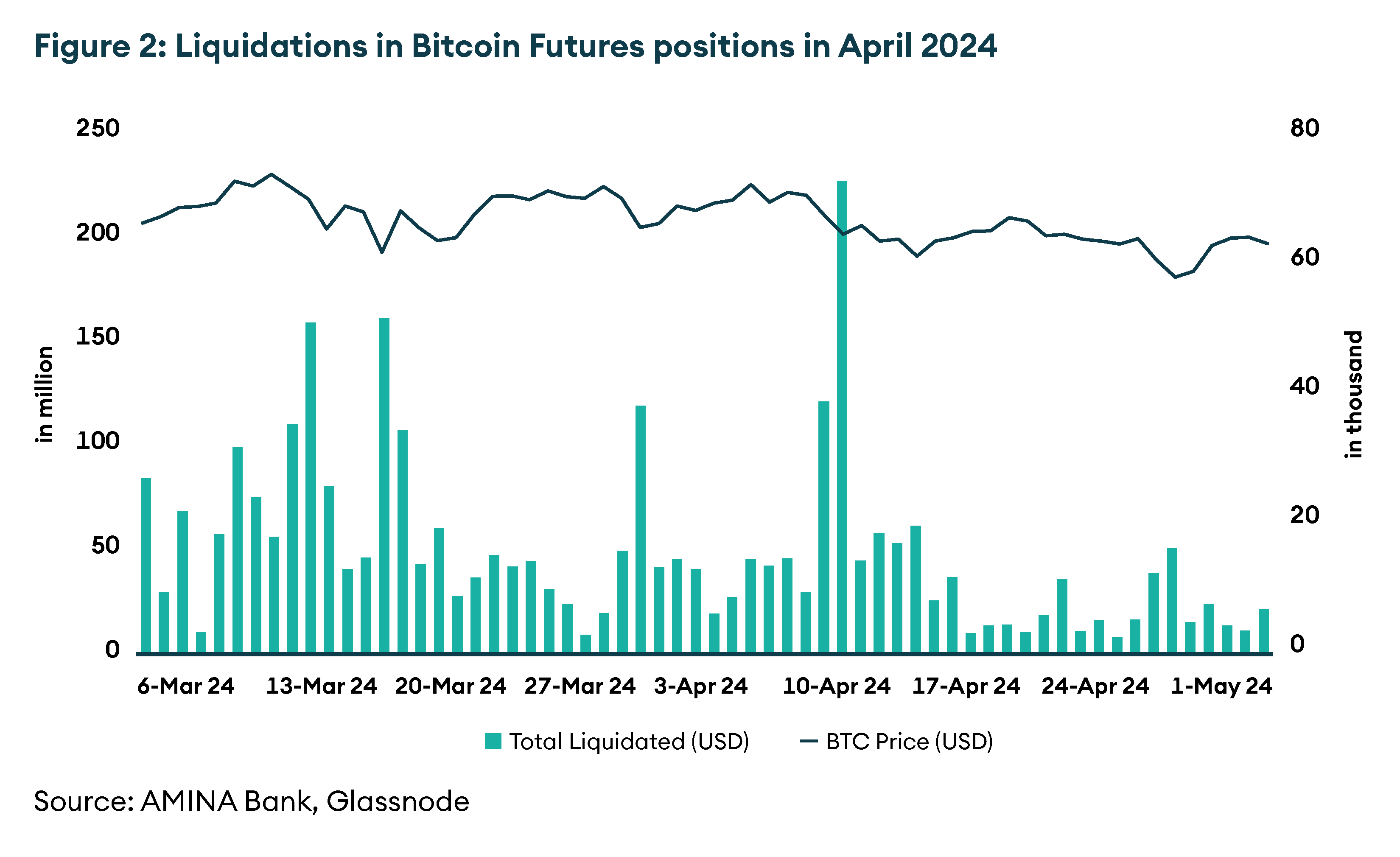

April saw major liquidations in the derivatives market. According to Coinglass, the largest liquidation happened on 12 April – close to USD 880 million across centralised exchanges.

Out of this, close to USD 225 million was in Bitcoin futures. Following a rather negative month for Bitcoin, the options Put/Call ratio has dropped by roughly 23% and is currently at 0.45 at the time of writing according to data from Glassnode.

Futures open interest too has seen a decline over the month. Overall, there is less leverage in the system and a marginal improvement in trader sentiment that is reflected in improved funding rates, although lower compared to levels seen in early April. Single day cumulative futures liquidations reached USD 125 million.

Ethereum

Ethereum is down 5% on the 30-day timeframe and trading at USD 3,175 at the time of writing. During the market-wide crash that ensued towards the end of April, Ether’s price dipped to around USD 2800 before recovering.

Onchain, layer-2s continue to move strong. Since the Dencun upgrade went live in March, transaction fees have become a fraction of what they used to be and this may have led to this growth in demand on L2s.

The average daily transaction count on OP Mainnet has shot up by 79%, on Arbitrum by over 90% and on Base by over 400%. However, the total value locked (TVL) on Ethereum L2s in April remained relatively flat, currently hovering around the USD 40 billion mark according to L2Beat.

This is roughly 70% of Mainnet TVL which is at USD 56 billion at the time of writing. In terms of net inflows in April, OP Mainnet tops the list with approximately USD 474 million in net inflows over the past one month, followed by Base (USD 287 million) and Arbitrum (USD 207 million). These inflows can be considered as indicators as to where we can expect retail interest in DeFi on Ethereum.

The main development for Ethereum in April was the airdrop and tokenomics announcement of EigenLayer – the largest restaking protocol in the cryptocurrency market.

EigenLayer has quickly grown to become the largest protocol by TVL across all chains and platforms (excluding liquid staking tokens), with USD 14 billion in ETH restaked. They recently announced the EIGEN token and its distribution to EigenLayer’s points holders in phase-1 of the airdrop.

Compared to Bitcoin, trader sentiment is better when we look at Ether traders. This is reflected in the consistently positive funding rates observed since the beginning of April.

However, leverage in the system has reduced despite this optimism which is reflected in the declining futures open interest. Put/Call ratio too has seen a significant decline over the month and is currently at 0.4 according to data from Glassnode. The day with the highest cumulative liquidations for Ether was 13 April and was worth over USD 125 million in futures positions.

As mentioned earlier, the month of April for Ether derivatives was quite like Bitcoin except for the relatively higher number of days with positive funding rates across centralised exchanges towards the end of the month.

Solana

Solana continues to be the leading alt-layer 1 network. In the month of April, Solana witnessed an 11% growth in stablecoin market capitalisation onchain. It continues to be retail’s favourite chain due to its high speed and low fees.

However, it was not all smooth sailing for Solana this past month. On the back of memecoin trading frenzy, the network saw congestion and caused a bump in user activity.

This led to significantly high demand for the network. As a result, this lack of block space led to a lower success rate for transactions on the network. At the peak of this frenzy, over 70% of transactions failed which led to frustration among Solana users.

Soon enough, Solana developers released a software upgrade to handle this network congestion issue and users are now able to transact as usual.

Uniswap

In April, the US Securities and Exchange Commission issued a Wells Notice to Uniswap. Wells notices are preliminary warnings that inform respondents of the charges the regulator is considering bringing against them.

They usually lead to enforcement actions. Uniswap’s native token, UNI, dropped 9.5% immediately after the news. It has traded flat since and is currently hovering around the USD 8 mark.

On the short term monthly timeframe, we observe a small decline in the number of active traders and trading fees on Uniswap.

This has come after Uniswap announced that they would increase their swap fee (if swapped through their interface) from 0.1% to 0.25%. While this is not expected to make a big difference for retail traders, whale trading activity may see a slight drop.

However, Uniswap continues to be the leading onchain decentralised exchange (DEX) on Ethereum. April saw Uniswap’s DEX trading volume dominance increase marginally from 69% to 71%. It is followed by Pancake Swap (17%) and Curve Finance (8%).

Conclusion

April brought a significant correction across the entire crypto market. With the Bitcoin Halving event unfolding successfully and block rewards reducing to half, miners will now hope for onchain activity to pick up and for transaction fees to increase.

If not, miner profitability may be at risk in this post hlaving era with the proportion of revenue coming from block rewards now having dropped significantly.

Among Ethereum L2s, Base may be poised for heightened adoption, potentially serving as a gateway for new users entering the crypto space via platforms like Coinbase.

Looking ahead, Bitcoin’s price trajectory hinges on two pivotal factors: the consistent inflow into spot Bitcoin ETFs, which significantly influences market sentiment and price dynamics, and the US Federal Reserve’s monetary policy stance.

A dovish Fed, characterized by reduced interest rates and ample liquidity, could lead to a wave of new users seeking exposure to riskier assets like cryptocurrencies.

As we anticipate the next market cycle, The Digital Investor invites readers to stay tuned for our upcoming edition, where we will delve deeper into market insights and provide a sneak peek into the evolving market outlook for the coming month.