AMINA Bank AG

AMINA Bank AG  AMINA UK

AMINA UK  AMINA Hong Kong

AMINA Hong Kong  AMINA EU

AMINA EU

Market Overview: Calm Markets, Structural Repricing

Markets rarely announce structural transitions while they are happening.

At a surface level, May 2026 appeared relatively uneventful. Bitcoin traded between approximately US$76,300 and US$82,164, while Ethereum remained between US$2,097 and US$2,369. Market volatility continued to compress throughout the month, reaching some of the lowest observed levels in recent periods.

Historically, periods of compressed volatility in crypto have often been interpreted as signs of declining participation or exhausted momentum. But May 2026 suggested a different interpretation. Despite relatively stable prices, the behaviour of market participants changed materially. Capital became increasingly selective, governance mechanisms became more active, and infrastructure continued attracting attention over consumer-facing applications.

Figure 1: Bitcoin 30-Day Realised Volatility (January–May 2026)

Source: AMINA Bank, TradingView

That shift became increasingly visible across five developments examined in this report: corporate treasury discipline, stablecoin infrastructure growth, Ethereum’s evolving power dynamics, the emergence of crypto-native private market access, and cross-chain security assumptions that may be prove to be the most consequential institutional risk discovery of the year.

From Bitcoin Accumulation to Capital Allocation

Few companies have influenced institutional perceptions of Bitcoin as significantly as MicroStrategy.

Over recent years, the company evolved from a software business into a public market vehicle for digital asset exposure, becoming synonymous with long-term accumulation. Investors were not simply buying Bitcoin exposure. They were buying into the assumption that accumulation itself was the strategy.

May suggested that assumption is being revised.

MicroStrategy redirected attention towards capital structure management through the repurchase of approximately US$1.5 billion of 0% convertible senior notes, while retaining approximately US$6.7 billion in convertible obligations, supported by roughly US$871 million in cash reserves. The company’s holdings reached 843,738 BTC, alongside reported BTC yield generation of approximately 0.7%.

Individually, these decisions likedly resemble prudent treasury management. Collectively, they suggest something more structural. The company increasingly appears to be operating as an active capital allocator rather than a passive accumulation vehicle. Treasury assets become a funding mechanism, liabilities become optimisation opportunities and future Bitcoin purchases become discretionary.

That distinction matters because it changes how markets may evaluate corporate crypto exposure going forward. Capital efficiency increasingly appears to matter as much as asset ownership.

Institutionalisation does not necessarily mean becoming more bullish. More often, it means becoming more disciplined.

Kelp DAO and the Hidden Architecture of Systemic Risk

The most consequential event of May may not have been a price movement.

The US$292 million Kelp DAO exploit drew immediate attention because of the scale of losses involved, but the more significant discovery emerged afterwards. Post-event analysis suggested that approximately 47% of active LayerZero OApp contracts, representing roughly 1,250 applications and more than US$4.5 billion in associated exposure, relied on effectively identical verification assumptions. This revealed a deeper issue than protocol security itself.

Crypto frequently treats composability as evidence of decentralisation. May demonstrated that those concepts are not necessarily interchangeable. Applications that appear independent may still depend on concentrated infrastructure, common validation pathways and shared operational assumptions underneath.

The implications extend directly into how institutional participants evaluate risk. For years, Total Value Locked became shorthand for ecosystem quality and protocol strength because deposited capital appeared to signal confidence and durability. May demonstrated the limitations of that framework. Capital alone reveals little about validator concentration, bridge resilience, or whether liquidity can genuinely exit during stressed conditions.

The lesson from May is not that decentralised finance failed. It is that the industry may need to become considerably more precise about what decentralisation actually means before treating it as a proxy for security or resilience.

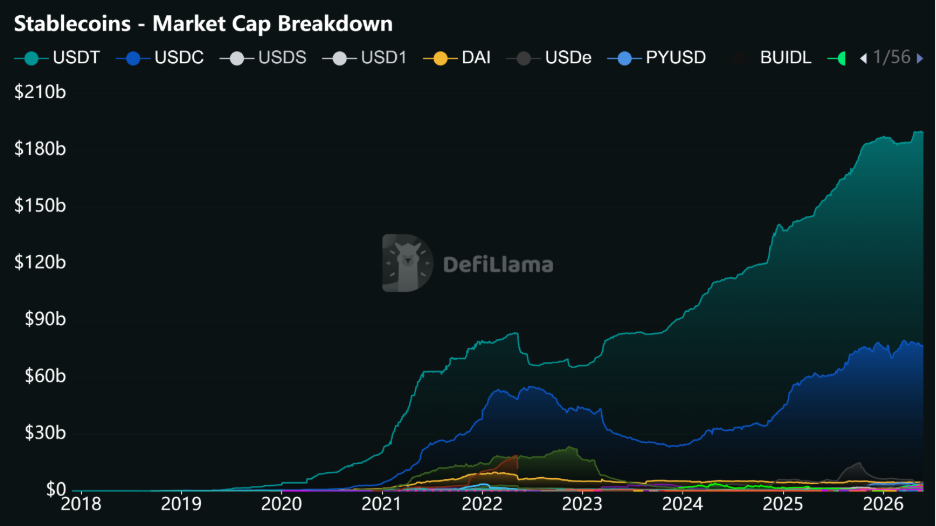

Stablecoins Continued Becoming Financial Infrastructure

The regulatory debate around stablecoins in May centred on the wrong question.

Discussion largely focused on restrictions surrounding stablecoin yield and whether digital dollars would face tighter alignment with banking frameworks. Yet the more important observation was that while direct interest mechanisms faced closer scrutiny, broader economic incentives tied to liquidity provision and participation remained economically viable.

That distinction matters because stablecoins have evolved well beyond trading infrastructure.

Total stablecoin market capitalisation exceeded US$323 billion during May. USDT accounted for approximately 59% of stablecoin supply, while USDC represented roughly 24%. Growth continued despite broader market consolidation and increasingly reflected usage beyond speculative activity.

Stablecoins now function as settlement infrastructure, collateral layers and liquidity engines across both centralised and decentralised markets.

Figure 2: Stablecoin Supply Growth and Market Composition (2018 – May 2026)

Source: AMINA Bank, DefiLlama

The direction of travel appears increasingly clear. Traditional financial institutions are not absorbing crypto wholesale and crypto is not replacing financial infrastructure outright. Instead, both appear to be converging towards a shared operating model in which regulation governs participation while software may continue determining economic behaviour.

If this trajectory persists, stablecoins may become one of the clearest examples of crypto infrastructure integrating into mainstream finance without losing the characteristics that made it useful in the first place.

Ethereum’s Scaling Roadmap and the Redistribution of Power

Ethereum’s roadmap has historically been framed around improving scalability while preserving decentralisation. The developments of May suggested that framing may be incomplete.

Emerging analysis around Enshrined Proposer Builder Separation (ePBS) indicates that while validator concentration may decline, economic influence could increasingly accumulate among specialised block builders with access to private order flow and advanced execution infrastructure.

At the same time, Ethereum’s broader roadmap continues becoming more ambitious. Current proposals point towards eventual block gas expansion approaching 200 million, while modelling suggests transaction fee reductions may approach 78% under certain assumptions.

These improvements are meaningful but they also introduce a broader strategic question.

If execution becomes the dominant competitive advantage, ownership of infrastructure may become more valuable than ownership of applications.

Traditional markets already operate this way. Public access appears open while execution quality remains concentrated among a relatively small number of specialised participants.

Crypto increasingly appears to be moving in the same direction.

Crypto Expanded Beyond Crypto

One of May’s most overlooked developments emerged not from tokens but from market structure.

Tokenisation discussions have historically focused on moving ownership onto blockchain infrastructure. May suggested something different. The emergence of pre-IPO perpetual products linked to anticipated private company valuations introduced a mechanism through which markets can express views on private assets before public listing events occur. These instruments do not provide ownership rights but instead create access to price discovery around private market valuation.

Private market valuation has long remained concentrated among institutional investors and venture firms. These instrucments, if they develop further, challenge that concentration by making valuation itself tradable.

It’s too early to assess whether this model will scale or how regulators will ultimately treat it. But the direction of travel is worth noting: crypto infrastructure is beginning to compete not only with financial products but with financial access itself.

Conclusion

May 2026 did not produce a new bull market thesis.

Instead, it revealed a market becoming more selective.

Capital increasingly rewarded infrastructure over narratives, discipline over accumulation and execution quality over headline growth. That shift does not make markets less volatile or less competitive. It changes what investors choose to value.

If previous cycles priced possibility, May suggested the market may finally be starting to price what crypto has actually built.

Disclaimer – Research and Educational Content

This document has been prepared by AMINA Bank AG (“AMINA”). AMINA is a Swiss licensed bank and securities dealer with its head office and legal domicile in Switzerland. It is authorised and regulated by the Swiss Financial Market Supervisory Authority (“FINMA”).

This document is published solely for educational purposes; it is not an advertisement nor a solicitation or an offer to buy or sell any financial investment or to participate in any particular investment strategy. This document is for publication only on AMINA website, blog, and AMINA social media accounts as permitted by applicable law. It is not directed to, or intended for distribution to or use by, any person or entity who is a citizen or resident of or located in any locality, state, country or other jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation or would subject AMINA to any registration or licensing requirement within such jurisdiction.

Research will initiate, update and cease coverage solely at the discretion of AMINA. This document is based on various sources, incl. AMINA ones. In preparing this document, AMINA may have made limited use of artificial intelligence–enabled tools to assist with research, summarisation, and drafting, with all content subject to human review and validation.

No representation or warranty, either express or implied, is provided in relation to the accuracy, completeness or reliability of the information contained in this document, except with respect to information concerning AMINA. The information is not intended to be a complete statement or summary of the subjects alluded to in the document, whereas general information, financial investments, markets or developments. AMINA does not undertake to update or keep current information. Any statements contained in this document attributed to a third party represent AMINA’s interpretation of the data, information and/or opinions provided by that third party either publicly or through a subscription service, and such use and interpretation have not been reviewed by the third party.

Any formulas, equations, or prices stated in this document are for informational or explanatory purposes only and do not represent valuations for individual investments. There is no representation that any transaction can or could have been affected at those formulas, equations, or prices, and any formula(s), equation(s), or price(s) do not necessarily reflect AMINA’s internal books and records or theoretical model-based valuations and may be based on certain assumptions. Different assumptions by AMINA or any other source may yield substantially different results.

Nothing in this document constitutes a representation that any investment strategy or investment is suitable or appropriate to an investor’s individual circumstances or otherwise constitutes a personal recommendation. Investments involve risks, and investors should exercise prudence and their own judgment in making their investment decisions. Financial investments described in the document may not be eligible for sale in all jurisdictions or to certain categories of investors. Certain services and products are subject to legal restrictions and cannot be offered on an unrestricted basis to certain investors. Recipients are therefore asked to consult the restrictions relating to investments, products or services for further information. Furthermore, recipients may consult their legal/tax advisors should they require any clarifications.

At any time, investment decisions (including, among others, deposit, buy, sell or hold investments) made by AMINA and its employees may differ from or be contrary to the opinions expressed in AMINA research publications.

This document may not be reproduced, or copies circulated without prior authority of AMINA. Unless otherwise agreed in writing, AMINA expressly prohibits the distribution and transfer of this document to third parties for any reason. AMINA accepts no liability whatsoever for any claims or lawsuits from any third parties arising from the use or distribution of this document.

©2026 AMINA, Kolinplatz 15, 6300 Zug