AMINA Bank AG

AMINA Bank AG  AMINA UK

AMINA UK  AMINA Hong Kong

AMINA Hong Kong  AMINA EU

AMINA EU Executive Summary

- Bitcoin is being used as a flight to safety amidst macroeconomic uncertainty. The network’s activity is at an all-time high with increasing daily transaction volume and hash rate.

- Ethereum’s Shanghai upgrade last month went smoothly and the network is getting geared up for the next two – Cancun, and Deneb.

- A financial model was built for Ethereum using a different approach – the Country model.

- Based on the model, Ethereum looks strong which reflects in the robust growth forecasts for the future.

Introduction

In this edition of the Digital Investor, we take a look at the state of the Bitcoin and Ethereum network. Its focus is a financial model analysis of the Ethereum ecosystem which is presented towards the end.

We look at Bitcoin’s on-chain activity, perceived reliability as a store of value and recent market fluctuations owing to activity of wallets linked with the now-defunct crypto exchange Mt. Gox. Right after, we look at the state of the Ethereum network and what lies ahead for the leading layer one blockchain.

Finally, we move to a financial model for the Ether token. The model offers a comprehensive overview of Ethereum’s value flow and uses a different approach to understand the growth potential of the ecosystem using the primary drivers of the ETH token without any intention of calculating the fair price of the token. The intention is to check, keeping in mind the future roadmap and speculative upgrades, whether Ethereum could grow as an ecosystem at a conservative pace.

Bitcoin

Bitcoin is being perceived as a reliable store of value. During times of macroenvironmental uncertainty, investors have off late used Bitcoin as a flight to safety. This was evident during the collapse of Silicon Valley Bank (SVB) and Signature Bank when investors bought BTC (and some Ether too) in exchange for their stablecoin and other altcoin holdings. At the time, even Binance, the largest cryptocurrency exchange, announced that their Industry Recovery Fund would mostly be held in Bitcoin. This show of confidence in the leading crypto asset led to a rally in its price with the currency touching the psychologically key level of USD 30K. It then went through a cooldown period.

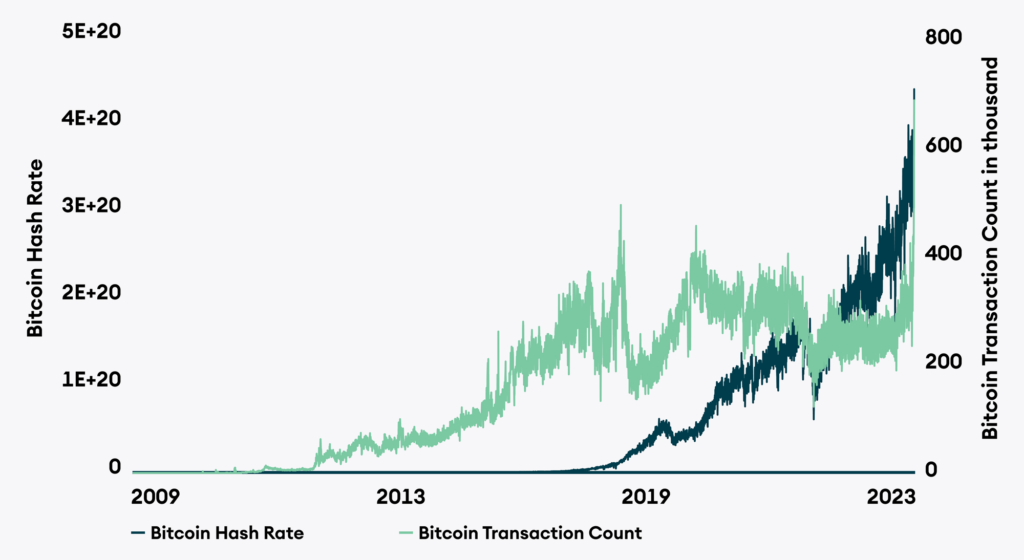

Earlier last week, there were rumours that wallets linked to the defunct crypto exchange Mt. Gox and the United States government were making transactions. Bitcoin’s price soon dropped 8% as the market felt that the sudden blip in activity of long-dormant wallets would be followed by them selling. While the asset still remains volatile, onchain activity is significantly higher than the better part of the past twelve months. Transactions are currently at an all-time high. Hashrate too has been on a commendable run touching its all-time high earlier last month.

Figure 1: Bitcoin Onchain Activity

Ethereum

The Ethereum network recently underwent a hiccup-free Shapella upgrade. It went smoothly with on-chain data showing improved strength for ETH. Ratio of free to staked ETH is the same as before the upgrade. Cancun and Deneb – the next upgrades to the Execution layer and Consensus layer respectively, are in progress. The first implementation of multi-client devnets for the network are expected in early October this year.

A Financial Model for Ethereum

What is Ether (Token)?

Crypto is simple but complex. Ethereum is complex – it displays the properties of all three super asset classes: Capital asset, Consumable/Transformable asset, and Store of value or money asset. Therefore, a simple DCF or a Relative valuation is insufficient in valuing Ethereum. This is because for a relative valuation, for example, we need to find and compare the closest peers. Ethereum is one of a kind, and we can compare it with other blockchains that mostly came after it, or we can compare it with traditional world stocks such as VISA.

To compare in relative valuation, we will have to use a lot of assumptions. For example, in the case of comparison with another blockchain, whether the blockchain is performing fairly/is stable in close to market efficient conditions, or when comparing with VISA, the business of taking cuts (fees) on transactions or nuances like a very high transaction per second (TPS) of VISA is closest to Ethereum which is not the case. Using relative valuation, when investing in a project as a venture capital or a private equity firm, we can take the hint of valuation because it is all about who pays more for the same equity.

A brief about ETH falling into the three super asset classes:

- ETH as a Capital Asset: ETH produces cash flow received by validators/block producers via staking (holding the native token ETH).

- ETH as a Consumable/Transformable asset: Gas is paid in ETH to use the Ethereum services. The higher the demand, higher is the consumption of the token.

- ETH as a Store of value asset: ETH is showing signs of retaining purchasing power like any other store of value asset. Purchasing power increases with an increase in scarcity or demand for the asset.

One of the implied conjectures to understand Ethereum given by Justin DrakeJustin Drakelink1 and also other public platformspublic platformslink1 use is one of them:

- Profit = Fees – Issuance

- Profit = Burn – Issuance

The equations above need to provide the best fit to understand system architecture. After Proof-of-stake (PoS) is introduced in the Ethereum network, holders of the token have an equal right to receive the rewards with validators (also holders of the tokens), unlike Proof-or-work (PoW), where miners are rewarded, and token holders have no right to the rewards. Expense is redistributed from token holders to validators in PoS. In PoS, ETH issuance to validators is at the expense of other token holders. If any other type of issuance is introduced, such as incentive programs, then the comparison of PoW to PoS could be apple to apple, unlike now.

The Country Model

If we ask yourself “What is the valuation of our country?”, the first thing that pops up in our mind is the total value of everything the country produces, aka its Gross Domestic Product (GDP). When we try to find the country’s worth, we measure it relative to the GDP and its growth rate, not the present value of something the country might produce five years down the line.

Similarly, the best attempt to understand the value of Ethereum would be to value everything it produces. The two ways to approach this would be finding the value of all the scaling solutions, like dApps & rollups, at a given time and understanding the growth of each or finding what Ethereum is earning from its services. The latter is easier and more reliable. This is because if we try to find the value of solutions built on top of Ethereum, the number of assumptions taken would look like a Merkle tree and still be far away from the real value.

Ethereum earns revenue for providing its services. The number of assumptions to approximate revenue are few, and it is also directly related to the quality of data available. However, one can question whether the reasoning behind these assumptions might be less justified. If we use a historical approach with bottom-up assumptions taken at conservative levels, it will land us, if not close to the real value, with a much clear view of the growth potential of the ecosystem.

The Revenue Approach

What do the basics tell us when trying to find revenue? We need to understand the revenue drivers. In the case of Ethereum, the primary drivers that bring value to ETH are transaction fees, token issuance, and MEV opportunities for Maximum Extractable Value. Let us understand each of these components separately since they would help us understand the model in one go and how the Ethereum ecosystem works in the simplest possible way.

Transaction Fees

Ethereum’s current pricing mechanism follows EIP-1599EIP-1599link1. It is a transaction pricing mechanism that includes a fixed fee per block, called a Base fee, that is burned and dynamically controls block size within set gas limits to deal with temporary congestion. The current gas limit for the block is 30 million with a target of keeping at 50%, i.e., 15 million gas per block. Gas is the measurement of the network’s resources used.

Currently, the network has only one gas limit and one fee market. It means irrespective of the services you use, whether a Decentralised Exchange (DEX) or a rollup, you will compete in the same market, which sometimes means a congested network. Moving forward, after EIP-4844EIP-4844link1 is implemented, another layer called Data Availability (DA) will be used for “data blobs” – instead of calldata. DA layer will have its gas limit per block and its fee market. You can find a detailed explanation of the DA layer hereherelink1.

Let us have a brief look at the Base and Priority fees:

- Base Fee: It acts as a reserve price for anyone eligible for block inclusion. The offered price per gas must be at least equal to the base fee. The base fee depends on previous blocks in line instead of the current block and is burned once the block is mined. The base fee increases by a maximum of 12.5% per block to maintain the block size.

- Priority fee: It precisely resembles a tip for the services used. As mentioned above, the base fee is burned, meaning validators have no incentives to include your transaction in the block. Whether they validate or not, they will receive the same block reward. A small tip is expected to include your transaction in the block, and you can pay more to execute your transaction before others.

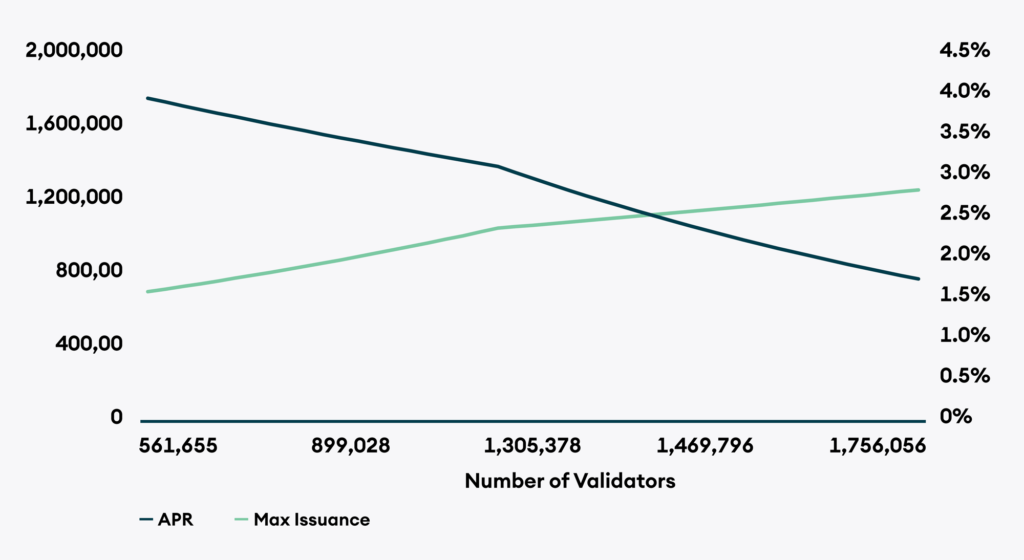

Issuance

Ethereum mints new ETH for each block to pay the validators. It is the incentive the network provides to the validators to secure the network in exchange for staking your ETH. Issuance is stable and low. The higher the staked amount of ETH or the greater number of validators, the higher the issuance. Issuance rate slows, i.e., yield per validator decreases with an increase in the number of validators. You can find the relation in the chart below:

Figure 2: Ethereum Issuance

Maximal Extractable Value (MEV)

It is the maximum value that can be extracted from block production in addition to the block reward and gas fee by controlling the order of the transactions in the block. MEV accrues to the validators as they handle the execution of the MEV opportunity and by other network participants called “searchers.” Searchers run algorithms to find profitable MEV opportunities on the blockchain and use bots to submit those profitable transactions to the network. In exchange for quick inclusion of the transaction in the block, Searchers pay higher gas fees, MEV, to the validators.

Although priority fees paid by the network users also contain a part of the MEV. The higher the tip, the higher the chance of including a transaction in the block and, as a result, more profit for the validator. We will leave further detailed discussion of the MEV for another time. Until then, you can find the doc on MEV hereherelink1 for the curious ones out there.

Model Completion

Now, we understand how the value flows in the Ethereum network. We can implement the model to its completion. The model tries to project the revenue for the next three years. I have divided the model as per flow: Validator yield via issuance, Execution layer revenue via Base fee, Priority fee, and MEV using MEV boost as the data input and proxy for MEV revenue, and finally, the revenue generated in the Data Availability layer via base fee and priority fee.

Projected revenue works on the assumptions keeping upcoming upgrades in mind, such as Proto danksharding (EIP-4844EIP-4844link1). MEV burn, Enshrined rollups, single slot finality, and a few other upgrades are in line, but the research is still ongoing, and the expected timeline is unclear. MEV opportunities in the DA layer are also not considered as it will be too much of an assumption as we have yet to be aware of the working. The fee mechanism for the base fee is also tested only under simulations; you can find the fee market analysis hereherelink1. Since the base fee and priority fee were enough to reflect the revenue growth, we can leave the incorporation of MEV and other revenue possibilities after the upgrade is implemented and runs successfully for some time.

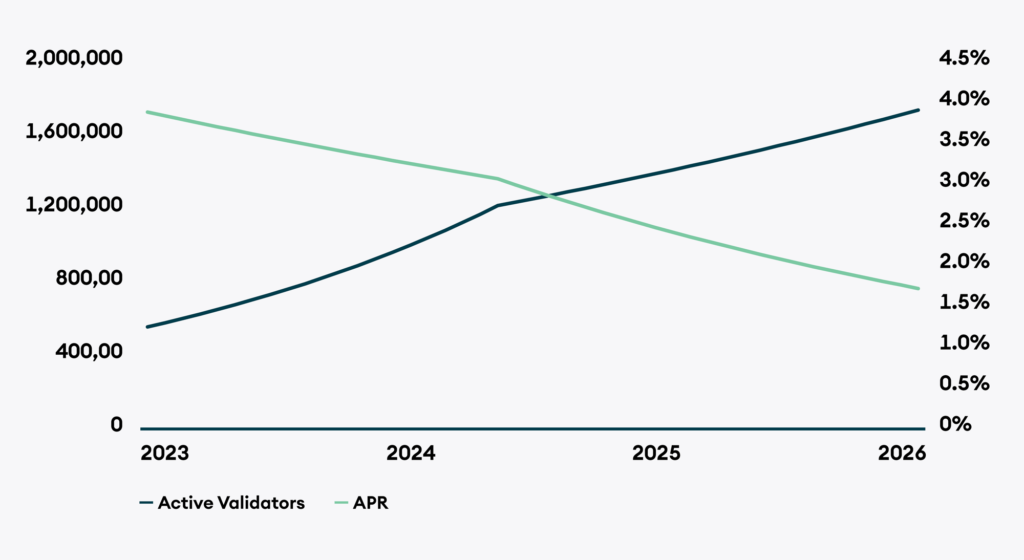

Staking Return

We assume that the number of validators grows at its historical growth rate and that it stabilizes to block growth rate over time to keep the yield per validator attractive. The timeline assumed for growth stabilization is two years. However, it will further depend on the network’s upgrades, but the staking return will look almost the same irrespective of the timeline. We can find the relation between the yield and validators over time.

Figure 3: Staking return (APR) and Number of Validators

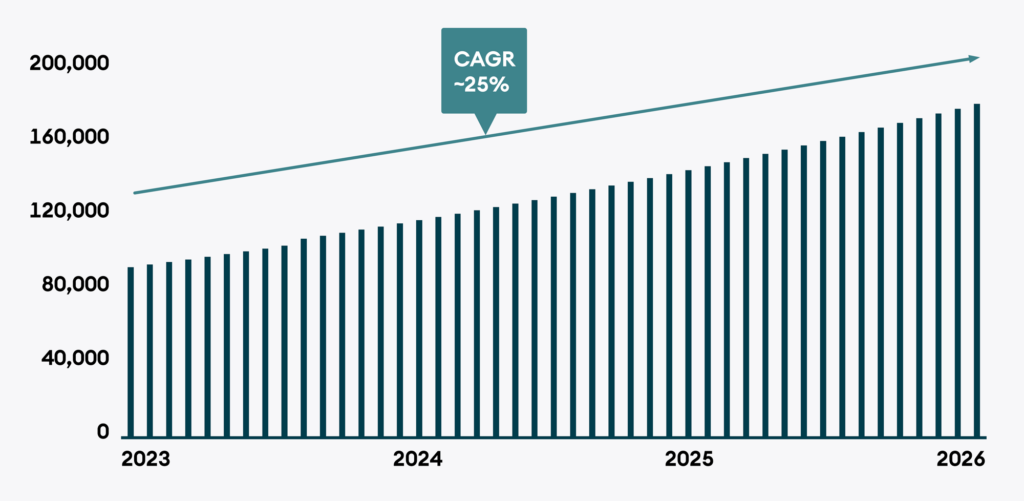

Execution Layer

In this component, the base fee reflects historical data, and the priority fee, for simplicity, is kept constant at the average priority fee paid over the past few months. The base fee is calculated on gas used, keeping 50% block utilization as the target. MEV blocks produced are also taken based on the long-time average block percentage of the total blocks produced, and MEV gas utilization is kept fixed based on the share MEV of the block value over the past 14 days. Deviation from the percentages used is minimal over time, as the historical data attests. You can find the MEV boost dashboard here.

Figure 4: Revenue (ETH)

Data Availability (DA) Layer

DA layer also generates revenue via base and priority fees in this model. We take incremental blob bytes to arrive at the total revenue. Proto-Danksharding introduces data blobs that can be sent and attached to the block. Blob carrying transaction is similar to a regular transaction except that it carries an extra piece of data called a blob. Blobs are measured in bytes. The target size of the throughput is 4 blobs, i.e., 0.5MB, with a limit of 1 MB. The current average block size is 90kb.

Incremental blob bytes measure the gas in the form of bytes, so it calculates over the current block size (90kb) till the target of 4 blobs is achieved.

Finally, the revenue from transactions is the sum of individual components of the Execution and DA layer. Also, the increasing total validator revenue shows growing network security. The higher the revenue, the higher the incentive for validators to participate in the network and, ultimately, the higher the security of the network.

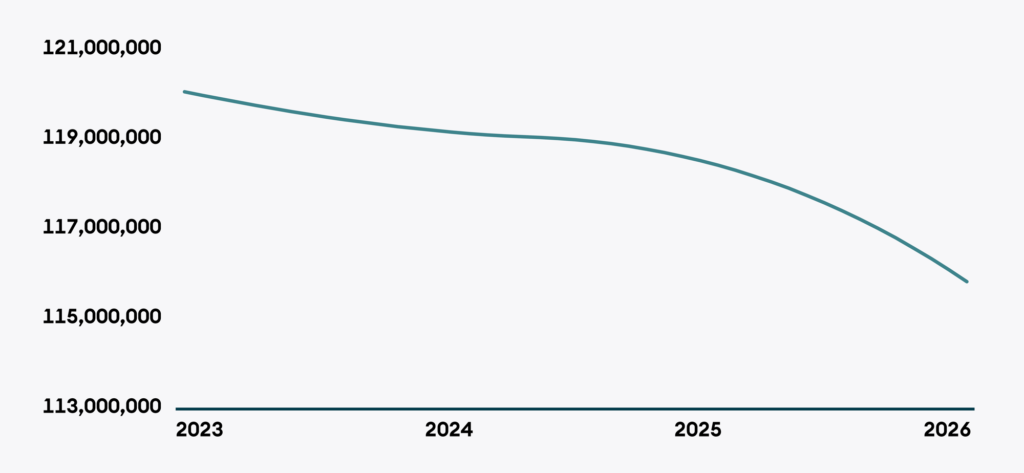

The supply curve also points in the direction of net deflationary hence more demand for the token with time.

Figure 5: Ethereum Supply Curve

Conclusion

There are a lot of other possibilities to introduce in this model, which could paint for us a more accurate picture but simultaneously make the model more complex. However, as mentioned before, this model helps us understand the Ethereum network’s growth potential with an understanding of the ETH value flow. It helps understand the growth potential of the ecosystem irrespective of the dollar value. Based on the above findings and the fundamental understanding, Ethereum looks very strong and reflects robust growth in the future.