AMINA Bank AG

AMINA Bank AG  AMINA UK

AMINA UK  AMINA Hong Kong

AMINA Hong Kong  AMINA EU

AMINA EU Introduction

Ethereum is back in the spotlight.

After years of debate around scaling, value accrual and the growing influence of rollups, the network is entering a new phase defined by the introduction of the Strawmap – a proposed roadmap aimed at restoring Ethereum’s competitiveness, strengthening the economics of the broader ecosystem and bringing renewed focus to ETH itself.

At the centre of this shift is Glamsterdam, the first major milestone that will test whether Ethereum can translate vision into execution. But the Strawmap is only one part of a much larger story. Despite persistent criticism and muted price performance, Ethereum continues to dominate onchain activity, while recent changes at the Ethereum Foundation signal a broader effort to sharpen the network’s strategic direction.

This edition explores the four forces shaping Ethereum’s next chapter: the Strawmap, Glamsterdam, Ethereum’s onchain position and the Ethereum Foundation reset.

Key Takeaways

- Ethereum Foundation reorg raises coordination concerns, but former contributors remain active across Ethereum-aligned research labs and public-goods structures.

- Ethereum still dominates capital-at-rest metrics such as TVL, stablecoins and RWAs, but trails faster chains on active-usage metrics.

- ETH underperformance reflects weak L1 value capture, as more activity moved to L2s while fees and burn declined.

- The Strawmap is Ethereum’s clearest attempt to restore L1 relevance and rebuild the ETH value-accrual story.

- The roadmap has five north stars: Fast L1, Gigagas L1, Teragas L2, Post-Quantum L1 and Private L1.

- Glamsterdam is the first major test, using ePBS and block-level access lists to improve L1 scalability.

- Ethereum’s next phase depends on converting technical upgrades and deep capital liquidity into renewed ETH demand.

Ethereum Foundation Under Pressure

Ethereum enters a new phase amid growing institutional scrutiny and one of the most significant leadership resets at the Ethereum Foundation in recent years.

Hsiao-Wei Wang stepped down last week as the co-executive director and board member of the Ethereum Foundation after returning from sabbatical. Wang joined the Foundation in 2017 and worked across several of Ethereum’s most consequential milestones, including the Beacon Chain, The Merge, Shapella and Dencun. Her exit followed Tomasz Stańczak, who had shared the co-executive director role with her after the Foundation announced a new leadership structure in March 2025.

The list of recent departures extends well beyond the co-executive director’s seat. Carl Beek, also known as Karl Beekhuizen, left after years of work on Ethereum’s proof-of-stake architecture. Julian Ma, a researcher associated with censorship-resistance work and ecosystem strategy, also departed. Josh Stark, one of Ethereum’s most recognisable public communicators and institutional interpreters, moved on. Trent Van Epps, linked to Protocol Guild and core-development funding discussions, resigned. Barnabé Monnot, a key researcher in protocol economics and mechanism design, exited. Tim Beiko, one of the most visible coordinators of Ethereum upgrades, also left his EF role. Alex Stokes took a sabbatical.

The number alone is not a sign of dysfunction. Ethereum’s ecosystem is built around contributors moving across organisations while continuing to support the network. The timing changes the interpretation.

These exits arrived during weak ETH price action, rising frustration over value accrual, and sharper competition from faster execution environments. In that context, every departure becomes a signal. The market wonders whether the exits reflect burnout after years of roadmap intensity, disagreement over the EF mandate, compensation pressure, governance fatigue, internal restructuring, or the pull of better-capitalised external projects. A clear answer may not exist. But the absence of a clear public account leaves room for every camp to project its own explanation.

That communication gap matters because the marginal ETH buyer has changed. Earlier buyers underwrote Ethereum’s developer mindshare and long-term programmable-finance thesis. Today’s allocator compares ETH against Bitcoin’s ETF reserve-asset story, Solana’s high-throughput trade, Hyperliquid’s onchain exchange narrative, stablecoins as payments infrastructure, Zcash as privacy exposure and AI-linked assets as usage-led trades.

Ethereum now faces a more demanding market. Technical seriousness is no longer enough. Investors want clearer answers on roadmap coordination, commercial expansion, ETH value accrual and who responds when confidence weakens.

The Ethereum Foundation’s March 2026 mandate clarifies part of the answer. The Foundation places CROPS at the center of its role: censorship resistance, open source, privacy and security. It frames the EF as one steward among many rather than Ethereum’s parent, ruler or commercial growth arm. The mandate protects the properties that make Ethereum worth using, especially self-sovereignty, credible neutrality and resistance to capture. That stance gives Ethereum its institutional premium.

Large pools of capital trust Ethereum because the base layer does not serve a single company, founder, exchange or jurisdiction. The same stance also limits the EF’s market-facing role. The Foundation will not optimise ETH price, turn the protocol roadmap into an investor-relations machine, or sacrifice decentralisation for speed. That posture creates the central tension of Ethereum’s current moment: the market wants a sharper asset story, while the Foundation wants to preserve the conditions that give the asset long-term relevance.

The Strawmap: Ethereum’s course correction

The Strawmap is Ethereum’s most important roadmap reframing since The Merge. It responds to the weakness that the last cycle exposed: the rollup-centric roadmap expanded the Ethereum ecosystem, but it also pushed activity away from the L1 fee market and weakened direct value capture for ETH.

The 2022 to 2025 cycle proved the benefit and the cost of that design. L2s became real execution venues. Base, Arbitrum, Optimism and application-specific rollups gained users, liquidity and developer attention. Institutions also found L2s useful because they can combine Ethereum settlement with customised execution, compliance features and lower transaction costs. At the same time, Dencun and EIP-4844 reduced L2 data-posting costs dramatically. Users benefited. Rollups benefited. ETH’s fee burn suffered.

We believe this is the core reason Ethereum has underperformed: activity grew across the broader Ethereum stack, but much of the economic value shifted to L2s while the L1 captured less fee revenue and generated less ETH burn.

Our central framing captures the contradiction: Ethereum remains dominant on metrics that measure capital at rest, such as TVL, stablecoins and RWAs, while losing share on metrics that measure active usage, such as network fees, application fees and DEX volumes. The Strawmap tries to close the latter gap without eroding the credible neutrality that anchors the former.

The roadmap organises Ethereum around five north stars.

Fast L1 targets finality in seconds. Ethereum currently runs on 12-second blocks, with full economic finality taking longer. Faster confirmation improves exchange deposits, bridge settlement, payments and institutional workflows. It also reduces one of the most visible UX gaps between Ethereum and faster chains.

Gigagas L1 targets roughly 10,000 transactions per second on the base layer. This is the most important north star for ETH holders. A much larger L1 gives Ethereum a path to host high-value activity at scale again. More L1 activity can restore base-fee burn through EIP-1559, but only if demand fills the new capacity.

Teragas L2 targets around 10 million transactions per second across rollups. This keeps L2s central to Ethereum, but changes the way the market should understand them. L2s no longer need to exist only as cheaper copies of mainnet. They can specialise in compliance, application logic, privacy, institutional execution, consumer UX and high-throughput environments while still anchoring to Ethereum.

Post-Quantum L1 prepares Ethereum for future cryptographic risk. A sufficiently powerful quantum computer could threaten current signature schemes. The timeline remains uncertain, but long-duration financial assets cannot ignore migration risk. Ethereum faces a harder engineering problem than Bitcoin because it must update cryptography across consensus, execution and data layers. It also has stronger upgrade infrastructure.

Private L1 targets privacy as core infrastructure. Public blockchains expose transaction graphs by default. That limits institutional adoption. Banks, funds, corporates and trading desks need privacy-preserving settlement with credible selective disclosure. Ethereum’s privacy work sits across applications, wallets and research groups, with the longer-term aim of making privacy a normal part of the stack rather than a niche tool.

Glamsterdam is the first major execution test of this new direction. The upgrade centers on enshrined proposer-builder separation and block-level access lists, with a proposed post-fork gas-limit floor around 200 million versus the current 60 million reference point. The target does not put Ethereum on par with the highest-throughput chains in one move. It still marks a decisive shift toward L1 scaling.

Glamsterdam Upgrade (H2 2026)

There are 2 headliner upgrades in the Glamsterdam Fork – enshrined proposer-builder separation on the consensus layer and block level access lists on the execution layer.

EIP-7732, enshrined proposer-builder separation (ePBS), restructures Ethereum’s block-production pipeline. Today, validators generally rely on specialised builders and external relays through MEV-Boost. That system improved block-building efficiency and validator profitability, but it also created relay dependency, builder concentration and scaling constraints.

Ethereum’s current block lifecycle forces validators to download, execute and attest to blocks within a narrow slot window. Larger blocks become difficult under that model. ePBS splits the process. Proposers commit to builder bids through a lighter consensus object, while the full execution payload arrives later. This expands the time available for transaction processing from only a few seconds to roughly 9 to 12 seconds. That extra time helps Ethereum raise gas limits and sets up the proving window needed for future zkEVM architecture.

ePBS also brings the builder market closer to the protocol. It reduces reliance on external relays and makes block-building commitments more transparent. It does not eliminate builder concentration by itself. Sophisticated builders will still benefit from better infrastructure, private order flow, MEV algorithms and latency advantages. Ethereum therefore needs the next layer of censorship-resistance work as well.

EIP-7928, block-level access lists, targets execution. Ethereum has historically processed transactions sequentially because validators do not know in advance which accounts or storage slots each transaction will touch. Block access lists require builders to include that information at the block level. Validators can prefetch data, identify independent transactions and execute parts of the block in parallel.

Parallel execution has become a baseline feature for high-performance chains. Ethereum’s design choice keeps the disruption away from users and applications. Builders take on more responsibility, while existing transaction formats remain largely intact. The benefit extends beyond immediate throughput. Block access lists also help the zkEVM path because provers can split witness generation and proof work across independent transaction clusters.

Together, ePBS and block access lists change the shape of Ethereum’s block lifecycle. ePBS expands the processing window. Access lists make that window more productive. The 200 million gas target therefore represents more than a number. It represents a renewed effort to make Ethereum L1 economically relevant again.

Hegotá follows Glamsterdam and focuses more directly on censorship resistance. Its clearest headliner is FOCIL, or fork-choice enforced inclusion lists. FOCIL addresses the risk that concentrated builders can exclude valid transactions.

FOCIL introduces randomly selected inclusion-list committees. Committee members observe the public mempool and publish signed lists of valid pending transactions. Builders then need to include those transactions unless they have a valid reason, such as invalidity or insufficient block space. Attesters check whether the block satisfies those inclusion conditions. The mechanism does not guarantee that every transaction lands immediately. It makes sustained exclusion harder and more expensive.

This matters for Ethereum’s target markets. Stablecoins, tokenised assets, DeFi collateral, institutional settlement and AI-agent infrastructure all require credible access to the base layer. If block production drifts toward censorship or private ordering, Ethereum’s neutrality premium weakens.

Post-quantum work may become Ethereum’s most underappreciated long-term advantage. Bitcoin faces a politically difficult migration problem around exposed public keys and dormant supply. Ethereum faces a broader engineering problem, but it also has the culture and machinery to coordinate live upgrades. As quantum timelines become harder to dismiss, a funded and active post-quantum path could strengthen Ethereum’s institutional case.

The data is better than the mood

At the time of writing (23 June 2026), ETH trades around $1,713, with a market capitalisation close to $206 billion and 24-hour spot trading volume around $13 billion. The asset remains one of the most liquid cryptoassets in the world. But it trades far below its 52-week high and well below levels that investors expected after spot ETFs, staking maturity and institutional tokenisation became mainstream themes.

The Bitcoin comparison tells the cleaner story. On 22 June 2021, CoinMarketCap’s historical snapshot showed Bitcoin at roughly $32,506 and Ethereum at roughly $1,875. That put ETH/BTC around 0.058. On 22 June 2026, Bitcoin trades around $64,000 and ETH around $1,740, placing ETH/BTC near 0.027. Over that five-year window, Bitcoin roughly doubled in dollar terms while ETH sits slightly below its June 2021 level.

The one-year view looks more nuanced. On 22 June 2025, Bitcoin was trading near $99,237 and Ether near $2,199 during a sharp market decline. Compared with current levels near $64,000 for BTC and $1,740 for ETH, both assets have fallen over the past year. ETH has fallen less in dollar terms across that specific date-to-date comparison, and ETH/BTC has improved from roughly 0.022 to roughly 0.027. That does not repair the longer-term damage. The five-year ratio chart still shows the market’s preference for Bitcoin as the cleaner reserve-asset trade.

Chart 1: ETH/BTC is down by 53% in 5Y, although slightly improved in last 1Y

Source: Google Finance

Onchain activity looks better than sentiment suggests. Ethereum recently processed around 2.083 million daily transactions, up from 1.883 million the prior day and 1.361 million one year earlier, a 53% year-over-year increase. The chart below also shows a record high of 3.63 million transactions on 28 April 2026. Average block time remains close to 12 seconds, with roughly 7,171 blocks processed per day. These figures undercut the lazy claim that Ethereum has no usage. The stronger critique focuses on the economics of that usage.

Chart 2: Ethereum Daily Transactions

![]()

Source: Artemis

Network transaction fees tell the harder story. Data shows Ethereum network transaction fees per day near 90.8 ETH, down from 276.2 ETH one year earlier. Defillama shows Ethereum chain fees of roughly $179,000 over 24 hours and chain revenue of roughly $42,000. That fee compression sits at the heart of the ETH value-accrual debate. Ethereum scaled users toward cheaper execution, especially through L2s and blobs, but lower L1 fees weakened the EIP-1559 burn narrative.

Chart 3: Scaling Upgrades on Ethereum have considerably lowered Transaction Fees and Chain Revenue

![]()

Source: Defillama

Staking demand gives the other side of the story. Beaconcha.in shows a deposit queue of 35,353 requests, representing 2.7 million ETH waiting to enter, with an estimated wait of around 46 days. The withdrawal queue sits at 1505 requests and 230,572 ETH, with an estimated wait near four days. Staking data also shows around 39.5 million ETH staked, roughly 32.45% of supply, with annualised staking yield near 2.74%. Ethereum still has a large base of holders willing to lock capital for validator exposure and protocol yield, even during poor price action.

Ethereum also retains its strongest position where capital rests. DefiLlama shows Ethereum stablecoin market capitalisation near $157.0 billion, RWA active market capitalisation near $14.76 billion, and DEX volume around $500 million over 24 hours. These numbers dwarf other L1s.

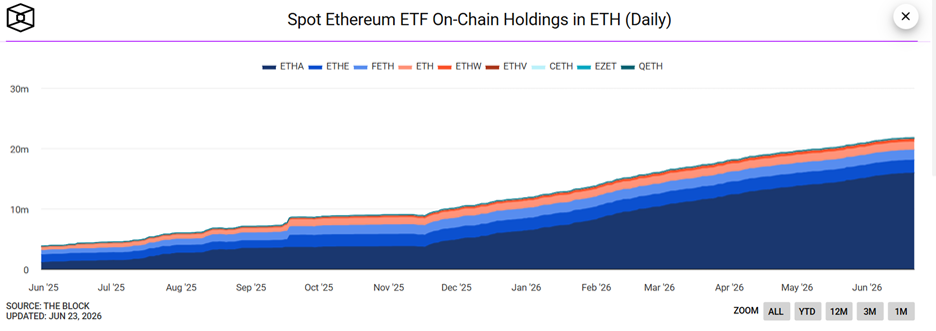

Institutional wrappers have also improved. BlackRock’s iShares Ethereum Trust ETF holds about $4.84 billion in net assets (as on 25.06.2026) , trades on NASDAQ, charges a 0.25% sponsor fee, and offers ether exposure inside traditional brokerage accounts. Spot ETH ETFs give allocators easier access, but access alone does not fix the thesis. Bitcoin ETFs amplified a simple story. ETH ETFs distribute a more complicated one.

Chart 4: Total Ethereum Spot ETFs continue to accumulate more ETH

Source: The Block

The data leaves Ethereum in a split position. It dominates capital-at-rest metrics such as stablecoins, RWAs, staking and DeFi liquidity. It has lost ground on activity-based metrics that drive fees, burns and the speculative perception of momentum. That contradiction explains why Ethereum can remain the default settlement layer for serious crypto finance while ETH trades with persistent doubt.

Conclusion

Ethereum’s roadmap now addresses the supply side of the thesis across every major dimension: L1 capacity, L2 scale, confirmation speed, censorship resistance, proving architecture, quantum readiness and privacy. The demand side remains unresolved. Ethereum needs markets where neutrality has higher pricing power: high-value DeFi, stablecoin settlement, tokenised assets, institutional privacy and AI-native economic coordination.

The roadmap gives Ethereum a clearer technical answer to its critics, but the market will judge it by execution, a standard Ethereum has met across multiple upgrade cycles. If Glamsterdam and the broader Strawmap can reconnect Ethereum’s deep capital base with stronger L1 value capture, ETH’s narrative will shift from underperformance to renewal.

Disclaimer – Research and Educational Content

This document has been prepared by AMINA Bank AG (“AMINA”). AMINA is a Swiss licensed bank and securities dealer with its head office and legal domicile in Switzerland. It is authorised and regulated by the Swiss Financial Market Supervisory Authority (“FINMA”).

This document is published solely for educational purposes; it is not an advertisement nor a solicitation or an offer to buy or sell any financial investment or to participate in any particular investment strategy. This document is for publication only on AMINA website, blog, and AMINA social media accounts as permitted by applicable law. It is not directed to, or intended for distribution to or use by, any person or entity who is a citizen or resident of or located in any locality, state, country or other jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation or would subject AMINA to any registration or licensing requirement within such jurisdiction.

Research will initiate, update and cease coverage solely at the discretion of AMINA. This document is based on various sources, incl. AMINA ones. In preparing this document, AMINA may have made limited use of artificial intelligence–enabled tools to assist with research, summarisation, and drafting, with all content subject to human review and validation.

No representation or warranty, either express or implied, is provided in relation to the accuracy, completeness or reliability of the information contained in this document, except with respect to information concerning AMINA. The information is not intended to be a complete statement or summary of the subjects alluded to in the document, whereas general information, financial investments, markets or developments. AMINA does not undertake to update or keep current information. Any statements contained in this document attributed to a third party represent AMINA’s interpretation of the data, information and/or opinions provided by that third party either publicly or through a subscription service, and such use and interpretation have not been reviewed by the third party.

Any formulas, equations, or prices stated in this document are for informational or explanatory purposes only and do not represent valuations for individual investments. There is no representation that any transaction can or could have been affected at those formulas, equations, or prices, and any formula(s), equation(s), or price(s) do not necessarily reflect AMINA’s internal books and records or theoretical model-based valuations and may be based on certain assumptions. Different assumptions by AMINA or any other source may yield substantially different results.

Nothing in this document constitutes a representation that any investment strategy or investment is suitable or appropriate to an investor’s individual circumstances or otherwise constitutes a personal recommendation. Investments involve risks, and investors should exercise prudence and their own judgment in making their investment decisions. Financial investments described in the document may not be eligible for sale in all jurisdictions or to certain categories of investors. Certain services and products are subject to legal restrictions and cannot be offered on an unrestricted basis to certain investors. Recipients are therefore asked to consult the restrictions relating to investments, products or services for further information. Furthermore, recipients may consult their legal/tax advisors should they require any clarifications.

At any time, investment decisions (including, among others, deposit, buy, sell or hold investments) made by AMINA and its employees may differ from or be contrary to the opinions expressed in AMINA research publications.

This document may not be reproduced, or copies circulated without prior authority of AMINA. Unless otherwise agreed in writing, AMINA expressly prohibits the distribution and transfer of this document to third parties for any reason. AMINA accepts no liability whatsoever for any claims or lawsuits from any third parties arising from the use or distribution of this document.

©2026 AMINA, Kolinplatz 15, 6300 Zug