AMINA Bank AG

AMINA Bank AG  AMINA UK

AMINA UK  AMINA Hong Kong

AMINA Hong Kong  AMINA EU

AMINA EU Executive Summary

November started strong but macroeconomic factors slowed the progress of the crypto bull market. However, on the fundamental side, there are no worrying signs. The trend of institutional adoption remained strong for Bitcoin in November and will be its biggest driver for growth.

Litecoin looks forward to its protocol upgrade in January 2022 that will bring total privacy as an opt-in feature. Bitcoin had the most significant improvement from a valuation perspective, but Litecoin remains the cheapest.

Ethereum has been an outperformer and remains the dominant platform chain in the face of stiff competition. It also enjoys the narrative of ultrasound money as EIP-1559 has significantly reduced inflation.

Polkadot parachain auctions have gone live and have seen significant participation. The parachains will be going live around 17 December 2021. In recent months, Cardano has been an underperformer as the market waits for decentralised applications to go live on the mainnet.

Decentralised finance continued to underperform. Product innovation to offer better capital efficiency and institutional pools may provide the catalyst for growth.

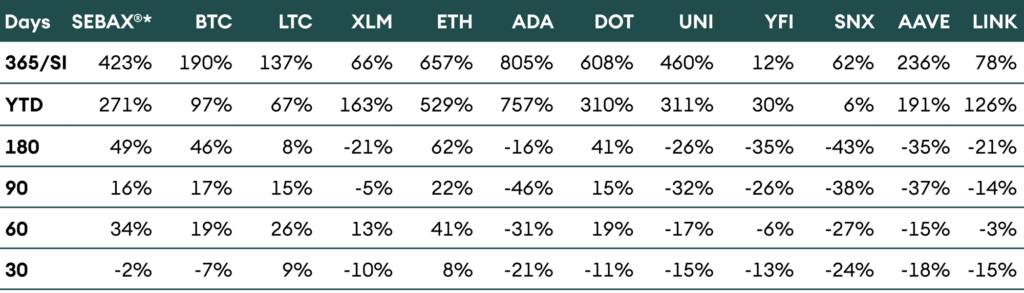

Table 1: Price performance in USD of the assets in coverage universe as of 30 November 2021

Introduction

November was another tumultuous month for the market as multiple events led to sharp movements in price. Early in the month, the market made new highs as bitcoin reacted positively to high inflation reported in the United States and touched an all-time high of USD 69,000.

A sharp sell-off followed, and the “hedge against inflation” narrative took a hit as the markets feared that consistently high inflation might force an end to the expansionary monetary policy being followed by central banks leading to tapering and rate hikes. In this regard, bitcoin and crypto assets behave as a risk-on asset class correcting with other risk markets like equity as the risk-free rate increases.

Fears over the growing spread of the new Covid-19 variant, Omicron, added fuel to the fire and the market continued to bleed and the month ended with only LTC and ETH closing on a positive note. The markets have remained under pressure in the initial days of December as macro events continue to dominate the sentiment. With limited control over these macro events, let us explore what is happening within the crypto universe.

Bitcoin

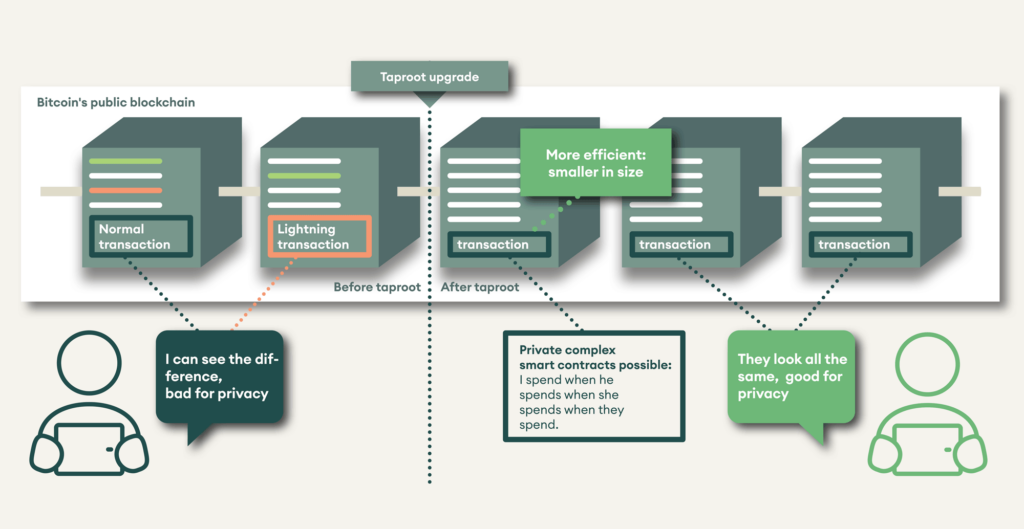

Bitcoin recorded an eventful month with its first significant protocol upgrade in four years going live, nicknamed Taproot. The Taproot upgrade improves the privacy and scalability of the protocol by not requiring conditional, and multi-sig transactions need to print unexecuted information onto the blockchain. Consequently, transactions with different signature types look similar, improving privacy. For more information on the upgrade, please refer to our Crypto Market Monitor on the topic.

Figure 1: The Taproot upgrade improves fungibility and privacy of Bitcoin transactions

For Bitcoin, adoption is one of the critical drivers for growth, and the trend remains positive as large institutions made further forays into bitcoin and the crypto asset class. Large banks are reportedly exploring ways to use bitcoin as collateral in borrowing. Paradigm, a crypto native venture capital firm, announced it had raised USD 2.5 billion for its new venture fund. This made it the largest ever crypto fund, eclipsing Andreessen Horowitz’s Crypto Fund III that raised USD 2.2 billion in June. Fidelity Investments also launched a spot-based Bitcoin ETF in Canada, making it the largest asset manager with a crypto ETF. Perma-bull Michael Saylor announced that MicroStrategy had bought an additional 7,002 BTC, bringing the total holdings by the company to 121,044 BTC or USD 6.9 billion. Such strong momentum in institutional adoption bodes well for the long-term outlook.

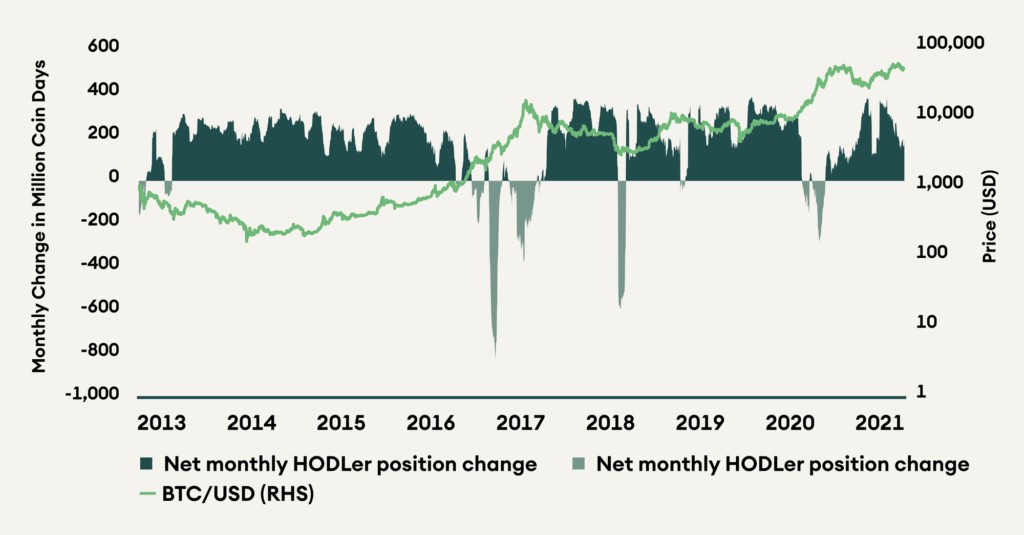

On-chain indicators have improved over the last month. The “net monthly HODLer position change” tracks the number of coin days added or destroyed over a rolling 30-day period. When the indicator is in red or is sloping downwards, it indicates a period of distribution, with coin days being destroyed as new buyers come in. This typically happens before a sharp run-up in price. From the current situation, it seems we may be entering this period, and if not for macro events, the bull market would have been in force.

Figure 2: Net monthly HODLer position indicates that BTC may be entering a period of distribution

Alternative Payment Chains

Litecoin was last month’s outperformer as its own protocol upgrade, MimbleWimble Extension Blocks (MWEB), is expected to go live in January 2022. MWEB will be an opt-in feature bringing full fungibility and privacy to Litecoin. An opt-in model for a privacy feature is ideal as it allows users to enjoy the privacy benefits while also mitigating the risk of adverse regulation. Centralised solutions that do not accept privacy coins may continue to accept Litecoin by opting out of MWEB. For more information on MWEB, please refer to this post by the Litecoin Foundation.

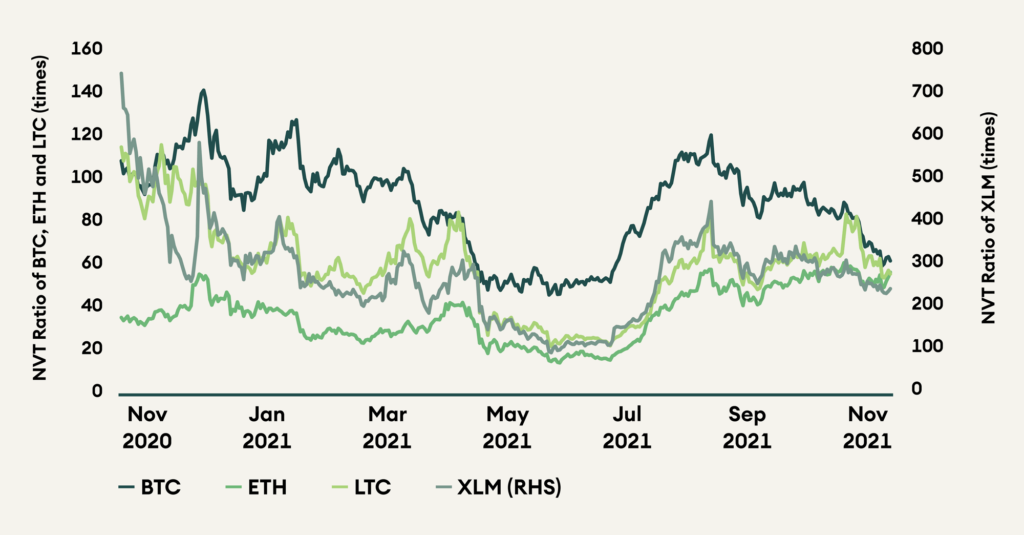

Payment protocols are trading at attractive prices according to valuation metrics. The valuation of the payment protocols can be measured through their network value to transactions value ratio (NVT). BTC saw a 27% decrease in its NVT ratio, falling to levels not seen since the mini bear market in Q2-Q3 2021. XLM and LTC also saw a fall in their NVT ratios of 16% and 12%, respectively, while ETH’s NVT increased marginally by 2%. On an absolute basis, LTC trades at the cheapest NVT of 56, followed by ETH at 57 and BTC at 62. XLM trades at a much higher NVT ratio of 245.

Figure 3: Sharp reduction in NVT ratios of BTC, LTC and XLM in November

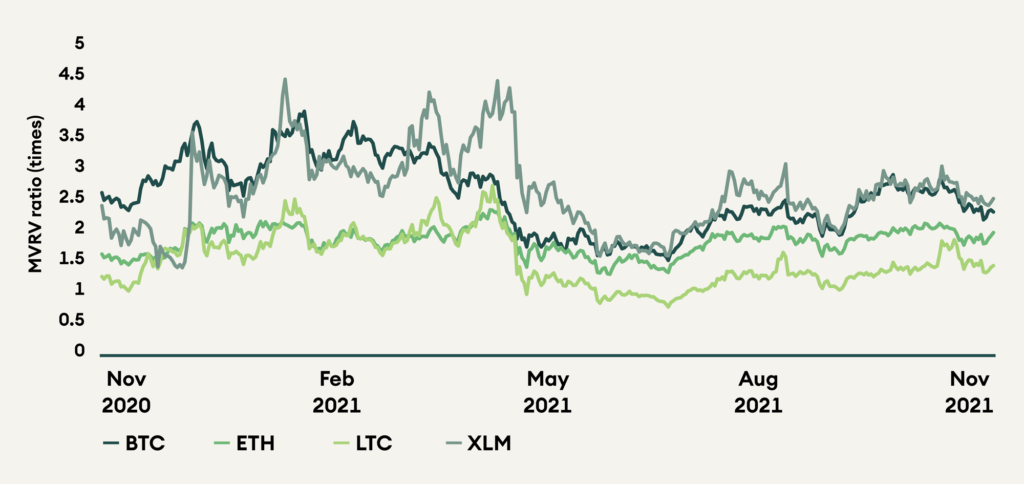

The behavioural indicator, market value to realised value ratio (MVRV), paints a similar picture. BTC’s MVRV reduced sharply in November by 13%, the highest fall of the four payment coins. At an absolute level, LTC trades at the lowest MVRV of 1.4, followed by ETH at 2, BTC at 2.3 and XLM at 2.5.

Figure 4: MVRV ratios for BTC, LTC, and XLM trade below their yearly average

Ethereum

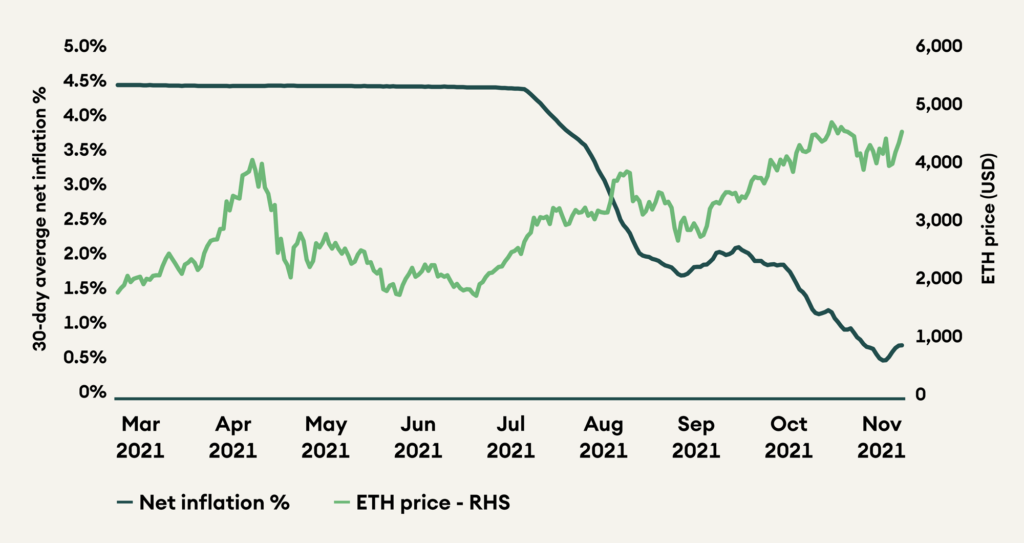

Ethereum price increased strongly in November. It enjoys a unique position in the crypto market as an established platform chain with the properties of a payment coin. Ethereum’s market cap, vintage, and network size allow it to act as a medium of exchange, store of value, and unit of account, second only to Bitcoin. One of the latest protocol updates (EIP-1559) also cemented strong tokenomics for ETH, and the protocol has since burnt more than 1 million ETH or USD 4.7 billion, which would have otherwise increased supply. For November, the average daily net inflation was a mere 0.8%, an >80% reduction since pre-EIP 1559 inflation of 4.5%.

Figure 5: Ethereum inflation has fallen significantly since the implementation of EIP-1559

Competition from newer, faster platform chains represents the biggest threat to Ethereum as transaction costs on the protocol remain high. While Ethereum’s total value locked (TVL) market share is slowly eroding, it remains the dominant platform.

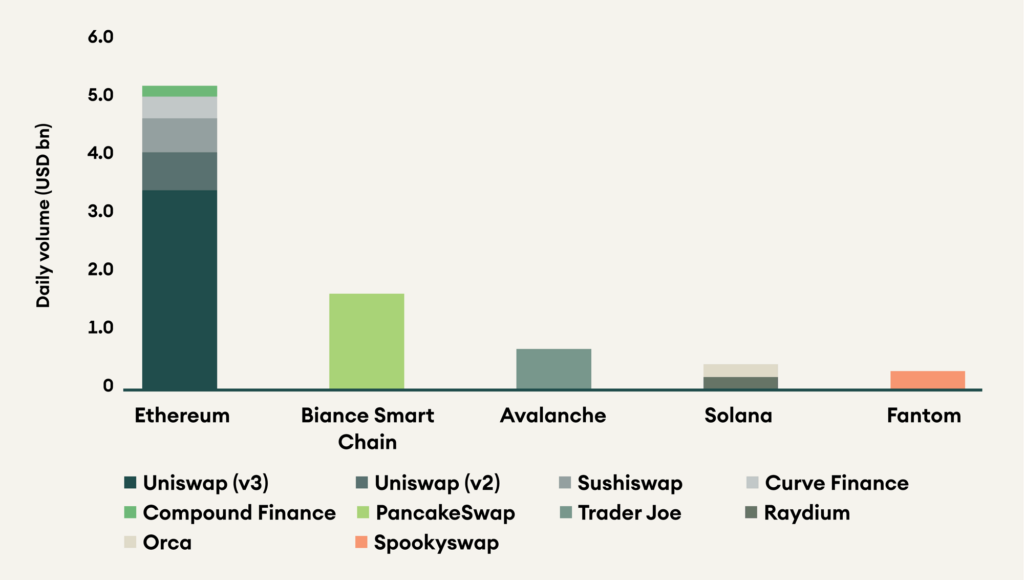

In earlier Digital Investors, we compared various platforms TVL to proxy adoption. However, this metric has its limitation as TVL is denominated mainly in crypto assets, its trend is positively correlated with price. As an additional proxy for usage, we compare the volumes on various decentralised exchanges (DEXes). Of the top 10 DEXes analysed, 5 DEXes were on Ethereum with a combined volume share of 62%. This shows that Ethereum remains the dominant platform chain even with exorbitant gas prices.

Figure 6: Uniswap on Ethereum has the highest market share of all DEXes

Alternative Platform Chains

Polkadot parachain auctions went live in November and generated significant community interest. Three parachain auctions have concluded, with Acala, Moonbeam, and Astar successfully bidding for their slot. The parachains are expected to go live after the first auction batch completes on 16 December 2021. This will finally make Polkadot the layer-0 to various blockchain ecosystems focussing on decentralised finance, NFTs, identity solutions, metaverse, and more.

So far, more than 75 million DOT or USD 2.2 billion have been locked in the three successful parachain bids, accounting for ~8% of the circulating supply. These DOT will be locked for 96 weeks, effectively taking them out of circulation. Two batches of five auctions will take place on Polkadot, and if the current trend continues, more than 20% of DOT may get locked in just the first ten auctions. Kusama, Polkadot’s canary network, is conducting its 17th parachain auction, with 30% of total supply locked.

After its stellar rise in H1 2021, Cardano has been a laggard in the second half of the year. Smart contract functionality went live for Cardano in September; however, the lack of developer tooling and unforeseen issues with the e-UTXO accounting model have slowed the development of applications. November also saw regulatory concerns as eToro, an exchange, delisted Cardano for its US customers. The exchange gave no clear reason, citing only the “evolving regulatory environment”.

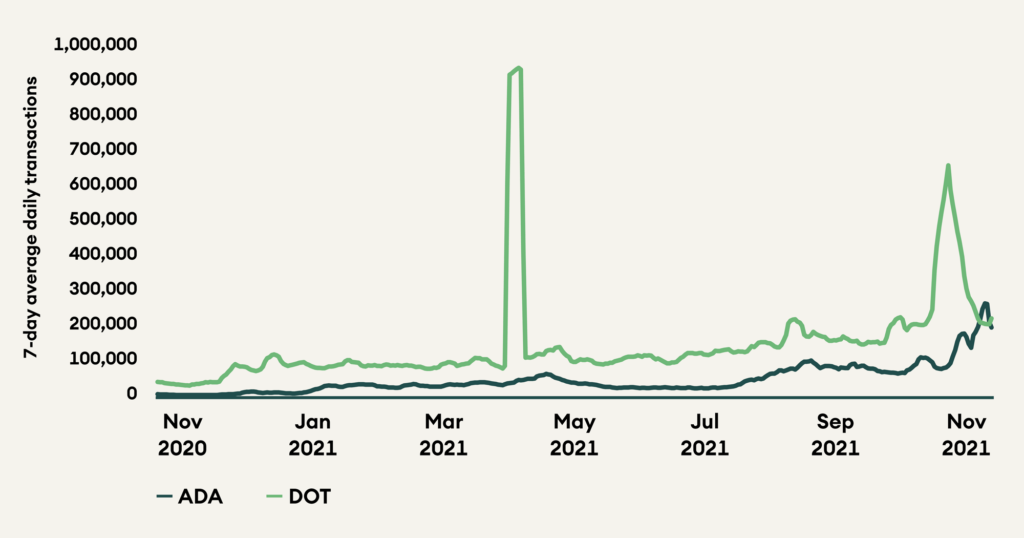

Average daily transactions show the adoption of the networks and saw significant growth for both protocols. Average daily transactions on Polkadot increased by 95% to ~362,000. Cardano also saw an increase of 83% in daily transaction count to ~150,000.

Figure 7: Transaction count on Polkadot is more than two times that on Cardano

Decentralised Finance (DeFi)

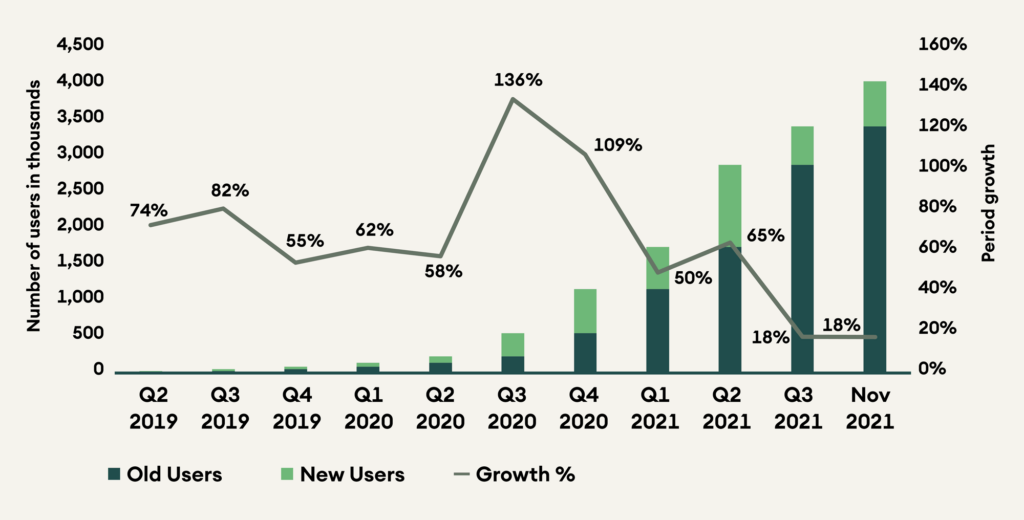

DeFi tokens have underperformed this year as they have suffered from other more dominant narratives taking away the limelight. Q1 2021 started strong for DeFi, but platform chains, meme coins, NFTs, and metaverse projects have dominated the narrative for the remainder of the year. The past two months saw an uptick in user activity, but growth is still lower than in Q1 and Q2.

Figure 8: DeFi user activity has increased in Q4 2021

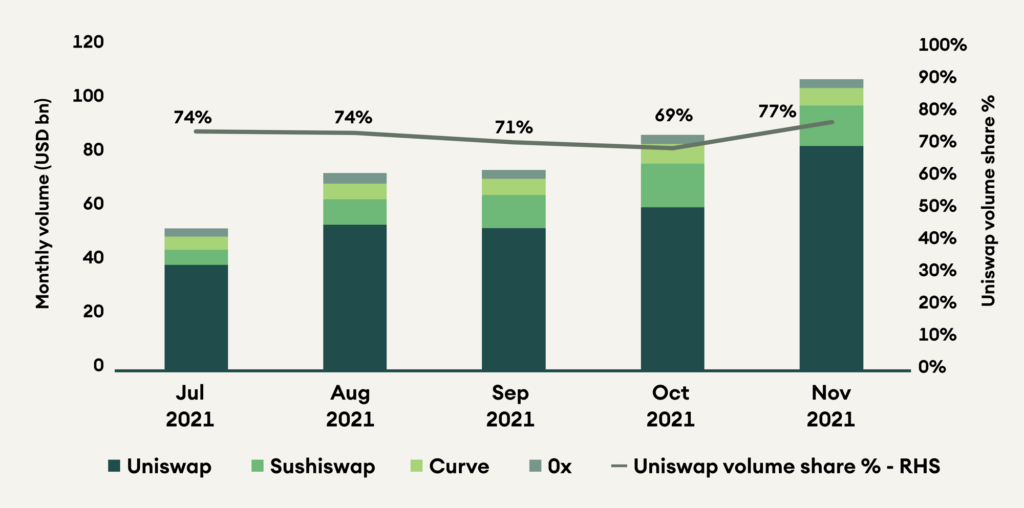

Individually, the protocols under coverage continue to build and innovate. Uniswap volumes have increased month on month since July, and November was the best month for Uniswap both in terms of absolute volume and market share. This is primarily due to the improvements in capital efficiency brought in by Uniswap’s v3 implementation. SushiSwap, a fork of Uniswap, has seen a decrease in market share and faced turnover in team members and allegations of misconduct.

Figure 9: Uniswap volume of USD 84 billion for November was a new monthly high

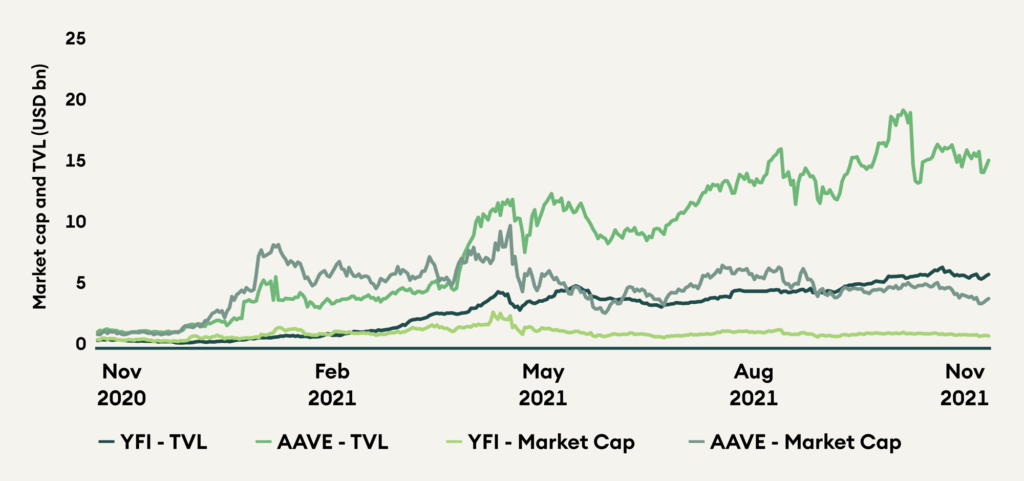

Aave is also preparing a significant upgrade to its protocol, Aave v3. This upgrade will allow for cross-chain DeFi for users, better capital efficiency for borrowers, and improved risk management for the protocol. Aave Arc, the institutional product, added Fireblocks as a whitelister for onboarding KYC/AML approved users, and there is a proposal to adopt Securitise as the second whitelister. Institutional adoption through KYC/AML regulated pools, and better capital efficiency may bring the next leg of growth to the performance starved DeFi space. With valuations falling to yearly lows of 0.2 Market Cap/TVL for YFI and 0.3 Market Cap/TVL for Aave, the space looks attractive.

Figure 10: YFI and AAVE TVL growth has outpaced market cap growth

Conclusion

November was mixed with new all-time highs and significant volatility due to macro events. Whether these events have slowed or stopped the bull market is yet to be seen, but on-chain and fundamental metrics only seem to be improving. The crypto asset class is still young enough that if fundamentals and adoption can improve, it may outweigh whatever impact the worsening macro condition may have. However, it will still be affected by them, at least in the short run, as it continues to be treated as a risk-on asset class. Zooming out, it becomes evident that if crypto even delivers on a fraction of the promise it holds, it has a long way to grow still.

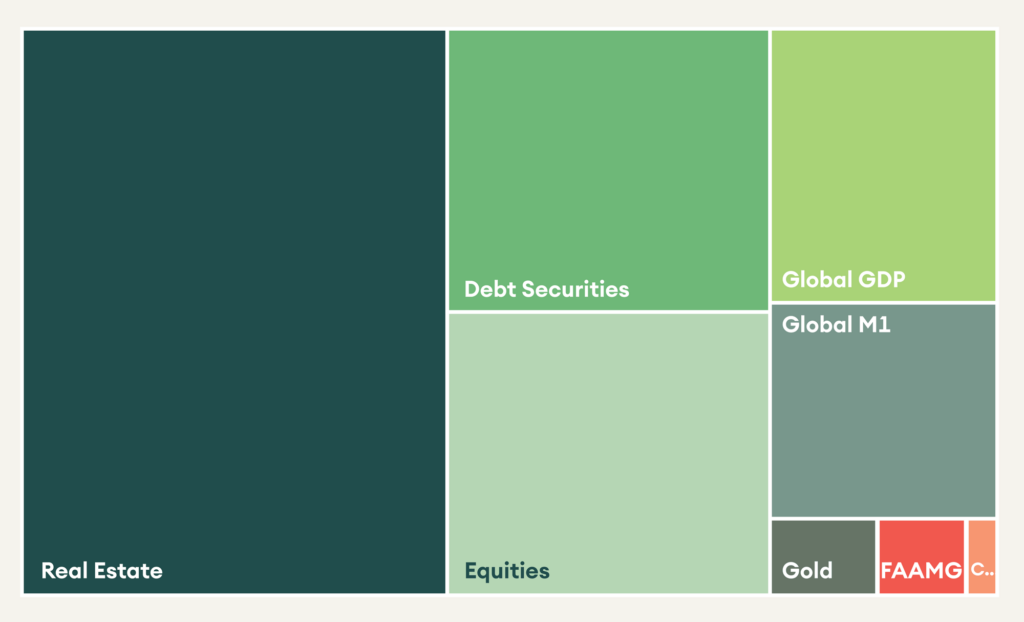

Figure 11: Comparison of the market cap of different asset classes show how young crypto is as an asset class