AMINA Bank AG

AMINA Bank AG  AMINA UK

AMINA UK  AMINA Hong Kong

AMINA Hong Kong  AMINA EU

AMINA EU

Crypto assets do not fit into traditional valuation frameworks.

They do not produce stable cash flows, do not represent enforceable ownership, and rarely offer a clear terminal value. Yet, trillions of dollars are allocated to them across institutional portfolios. This creates a contradiction. If these assets cannot be valued using the tools of traditional finance, what exactly are investors pricing?

The problem is not that crypto is hard to value. The problem is that it is approached with the wrong assumptions.

Crypto is not mispriced. It is misunderstood.

Crypto assets are not valued in the classical sense. They are bid based on their ability to attract, retain, and compound capital within a reflexive system. To understand this, valuation must be reframed. Not as intrinsic value, but as a function of monetary gravity.

The framework that follows redefines crypto valuation not as a function of intrinsic worth, but as a question of which systems can attract, retain, and compound capital — and which cannot.

Why Traditional Valuation Models Fail in Crypto

Traditional valuation models rely on enforceable claims on future earnings. Discounted cash flow assumes that an asset produces predictable cash flows and that investors have a legal claim over them. Crypto assets do not satisfy these conditions.

Even when protocols generate revenue through fees, those revenues are distributed across validators, liquidity providers, and network participants rather than accruing cleanly to token holders. There is no shareholder structure, no guaranteed distribution, and no mechanism that ties ownership directly to earnings.

Tokens behave differently. Depending on their technical feature and local regulatory classification frameworks, they may function simultaneously as commodities, capital assets, and monetary instruments. Applying equity frameworks to them does not produce rough estimates. It produces misleading conclusions that appear analytical but lack real explanatory power.

The concept of terminal value also breaks down. Traditional finance assumes persistence and relatively stable business models. Crypto operates in an environment of rapid iteration where protocols evolve, fragment, or become obsolete at a pace that makes long-term projections unreliable.

The more relevant question is not what a crypto asset is worth. It is why capital flows into it and, more importantly, why it stays.

A New Framework for Valuing Crypto Assets

Value in crypto is not derived. It is captured.

Crypto assets do not compete on earnings. They compete on their ability to pull capital toward themselves and retain it. This dynamic can be understood through what can be described as monetary gravity.

Monetary gravity is the force that determines whether capital accumulates around an asset or disperses away from it. It emerges from the interaction of liquidity, economic activity, attention, and value capture. Together, these forces define how value forms and persists in crypto markets.

Liquidity: The Primary Driver of Crypto Prices

Liquidity is the base layer of crypto valuation.

Without liquidity there is no price formation. Without price formation there is no narrative. Without narrative there is no adoption. Crypto markets are highly sensitive to the availability of capital, particularly in the form of stablecoins, leverage, and institutional inflows.

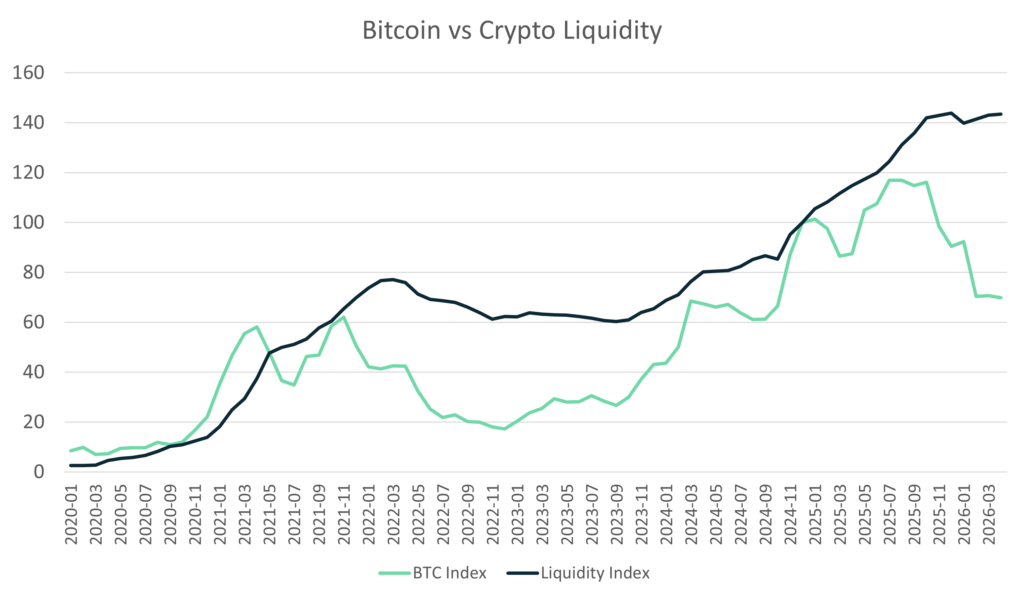

Bitcoin provides the clearest example of this dynamic.

Figure 1: Bitcoin vs Crypto Liquidity (Indexed to 100, 2020–2026)

Source: AMINA Bank

When both Bitcoin and crypto-native liquidity are normalised to a common starting point, their trajectories move closely together over time. Periods of expanding liquidity have aligned with sustained price appreciation, while contractions in liquidity have coincided with periods of weakness or consolidation.

This relationship does not prove strict causality, but it highlights a potential structural dependency. Bitcoin does not operate independently of capital flows. It may responds to them, often with amplification.

Liquidity does not follow value in crypto. It defines it.

Does Network Activity Actually Create Value?

In traditional systems, increased usage generally translates into increased value. Higher demand leads to higher revenues, which in turn supports higher valuations. In crypto, this relationship is far less stable.

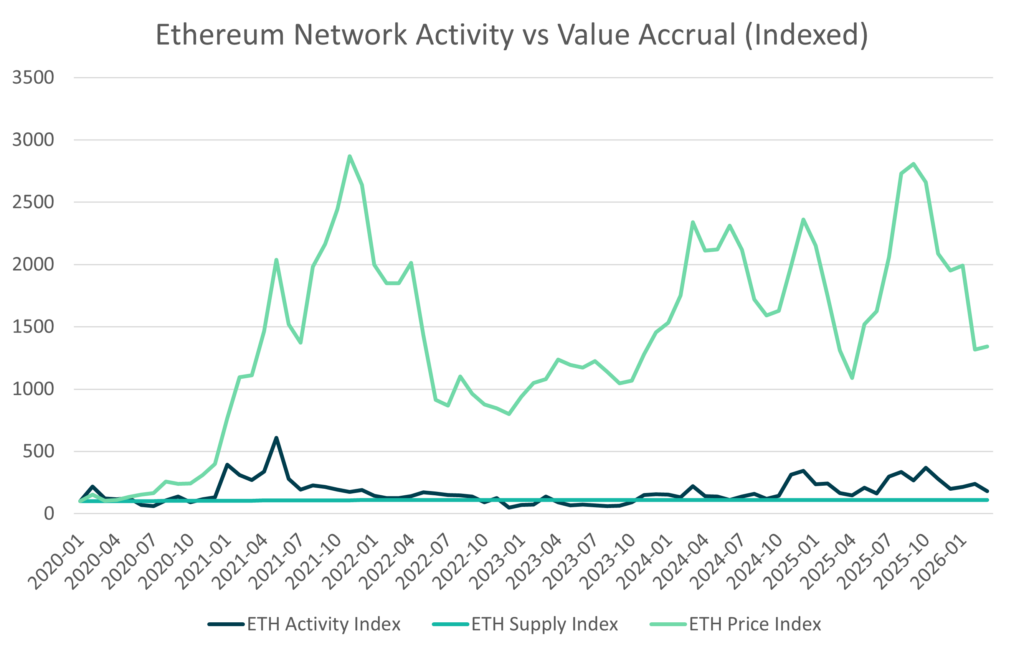

Ethereum illustrates this clearly.

Figure 2: Ethereum Activity vs Supply (Indexed to 100, 2020–2026)

Source: AMINA Bank

Despite substantial growth in on-chain activity, Ethereum’s supply and price have not moved in lockstep with usage. While price has at times risen alongside activity spikes, the correlation is inconsistent and supply remains relatively stable over time. This creates a visible divergence between usage and value accrual.

The underlying reason is structural. Improvements in scalability reduce transaction costs, which lowers fee pressure on the base layer. The network becomes more efficient and more usable, but the mechanisms that translate usage into scarcity weaken.

This creates what can be described as a scaling paradox. Better technology improves the network while simultaneously reducing the direct economic pressure that might otherwise support token value.

Usage can grow significantly without producing a proportional increase in value.

The Role of Attention in Crypto Markets

In a system where the number of assets is effectively unlimited but capital is constrained, attention becomes a critical resource.

Crypto markets operate differently from traditional financial systems in that narratives are not merely reflections of price. They actively shape it. Attention directs capital, and capital reinforces attention in a reflexive loop.

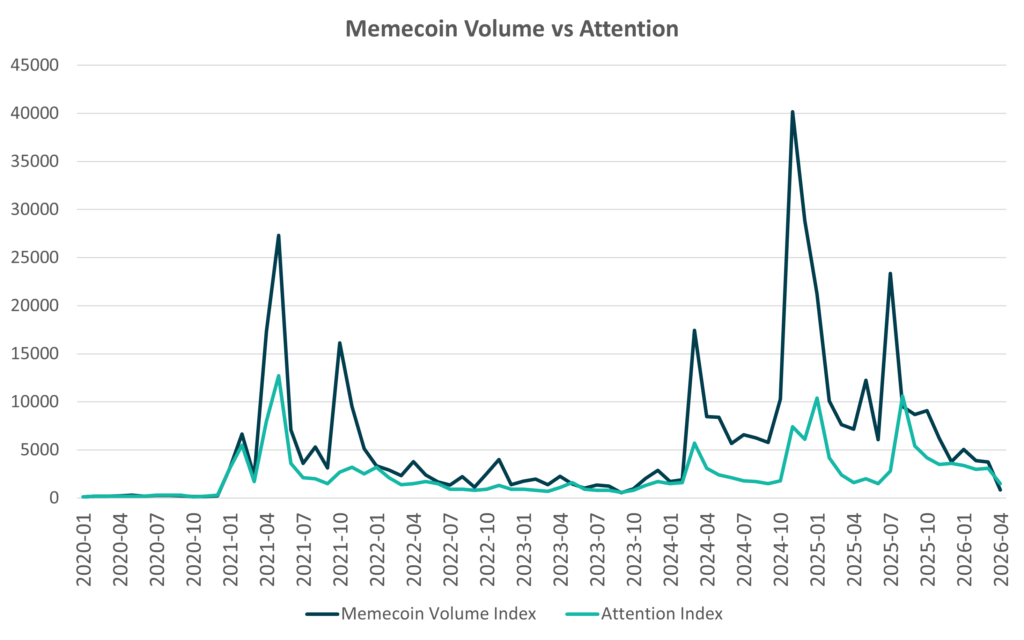

Memecoins provide the clearest example of this mechanism.

Figure 3: Memecoin Volume vs Attention (Indexed to 100, 2020–2026)

Source: AMINA Bank

Trading activity in memecoins closely tracks shifts in attention. When attention rises, participation increases. As participation increases, liquidity deepens and price movements accelerate.

These assets do not derive value from utility in the traditional sense. They derive value from coordination. Attention becomes the mechanism through which capital is directed and concentrated.

In this context, attention is not a secondary factor. It functions as a core input into price formation.

Where Does Value Actually Accrue in Crypto?

Attracting liquidity and activity is only part of the equation. The more difficult question is where value ultimately settles.

Crypto ecosystems are increasingly modular. Base layers provide security and settlement. Execution layers handle transactions. Applications interface with users and capital.

As blockspace becomes more abundant and transaction costs decline, scarcity shifts away from infrastructure and toward layers that directly engage users and capital. This changes where value is captured.

The assumption that value automatically accrues to the base layer is no longer reliable. In many cases, value migrates toward applications and interfaces that control distribution and user interaction.

Crypto assets do not compete for market share in the traditional sense. They compete for the ability to attract and retain capital within their own ecosystems.

Key Takeaways for Evaluating Crypto Assets

Valuing crypto requires a shift in perspective.

The focus should move away from estimating intrinsic value and toward understanding the forces that drive capital flows. Liquidity determines how much capital enters the system. Economic activity determines where that capital moves. Attention determines what assets capital concentrates around. Value capture determines whether that capital stays.

This framework does not produce a single number. It produces a way of thinking about how value forms in a system that does not behave like traditional markets.

Conclusion

Crypto valuation is not about estimating intrinsic value.

It is about understanding which systems can attract, retain, and compound capital within a reflexive environment.

Liquidity determines how much capital enters. Activity determines where it flows. Attention determines what it concentrates on. Value capture determines who retains it.

The question is no longer what an asset is worth.

The question is whether it can sustain monetary gravity.

In a market defined by uncertainty and rapid change, that is the closest approximation to value.

Disclaimer – Research and Educational Content

This document has been prepared by AMINA Bank AG (“AMINA”). AMINA is a Swiss licensed bank and securities dealer with its head office and legal domicile in Switzerland. It is authorised and regulated by the Swiss Financial Market Supervisory Authority (“FINMA”).

This document is published solely for educational purposes; it is not an advertisement nor a solicitation or an offer to buy or sell any financial investment or to participate in any particular investment strategy. This document is for publication only on AMINA website, blog, and AMINA social media accounts as permitted by applicable law. It is not directed to, or intended for distribution to or use by, any person or entity who is a citizen or resident of or located in any locality, state, country or other jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation or would subject AMINA to any registration or licensing requirement within such jurisdiction.

Research will initiate, update and cease coverage solely at the discretion of AMINA. This document is based on various sources, incl. AMINA ones. In preparing this document, AMINA may have made limited use of artificial intelligence–enabled tools to assist with research, summarisation, and drafting, with all content subject to human review and validation.

No representation or warranty, either express or implied, is provided in relation to the accuracy, completeness or reliability of the information contained in this document, except with respect to information concerning AMINA. The information is not intended to be a complete statement or summary of the subjects alluded to in the document, whereas general information, financial investments, markets or developments. AMINA does not undertake to update or keep current information. Any statements contained in this document attributed to a third party represent AMINA’s interpretation of the data, information and/or opinions provided by that third party either publicly or through a subscription service, and such use and interpretation have not been reviewed by the third party.

Any formulas, equations, or prices stated in this document are for informational or explanatory purposes only and do not represent valuations for individual investments. There is no representation that any transaction can or could have been affected at those formulas, equations, or prices, and any formula(s), equation(s), or price(s) do not necessarily reflect AMINA’s internal books and records or theoretical model-based valuations and may be based on certain assumptions. Different assumptions by AMINA or any other source may yield substantially different results.

Nothing in this document constitutes a representation that any investment strategy or investment is suitable or appropriate to an investor’s individual circumstances or otherwise constitutes a personal recommendation. Investments involve risks, and investors should exercise prudence and their own judgment in making their investment decisions. Financial investments described in the document may not be eligible for sale in all jurisdictions or to certain categories of investors. Certain services and products are subject to legal restrictions and cannot be offered on an unrestricted basis to certain investors. Recipients are therefore asked to consult the restrictions relating to investments, products or services for further information. Furthermore, recipients may consult their legal/tax advisors should they require any clarifications.

At any time, investment decisions (including, among others, deposit, buy, sell or hold investments) made by AMINA and its employees may differ from or be contrary to the opinions expressed in AMINA research publications.

This document may not be reproduced, or copies circulated without prior authority of AMINA. Unless otherwise agreed in writing, AMINA expressly prohibits the distribution and transfer of this document to third parties for any reason. AMINA accepts no liability whatsoever for any claims or lawsuits from any third parties arising from the use or distribution of this document.

©2026 AMINA, Kolinplatz 15, 6300 Zug