AMINA Bank AG

AMINA Bank AG  AMINA UK

AMINA UK  AMINA Hong Kong

AMINA Hong Kong  AMINA EU

AMINA EU The universe of investable crypto assets today, while small, is expanding. Imagine that in a near future this universe becomes reasonably large and liquid, or in other words, it becomes as mature as other alternative asset classes such as commodities and hedge funds. How would this world look like?

To shed some light on this scenario, we imagine a world similar to the one we are living in today and question how asset allocation would be affected and what would be the implications for policymakers.

Today

We are living in a world where most of the key financial and economic variables are running “low”. As far as the main economic variables are concerned, we find low rates of growth, low productivity, low inflation and even low unemployment. Within financial variables, we have low interest rates, low yields, low risk premiums and consequently low expected returns on investment.

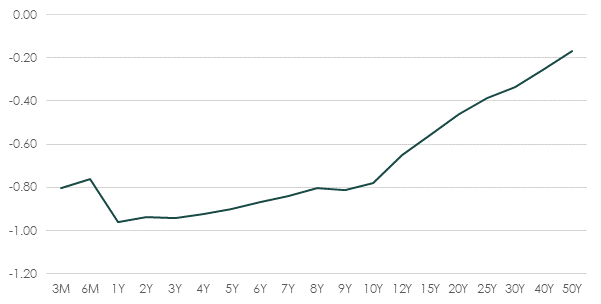

In some countries, financial variables have even become negative. Major central banks such as the European Central Bank and the Swiss National Bank have implemented Negative Interest Rate Policies (NIRP). In combination with other policies, NIRP has weighed on the entire yield curve. For example, yields in Switzerland (up to 50 years), are negative (Exhibit 1)

Exhibit 1: Swiss government bonds yielding curve

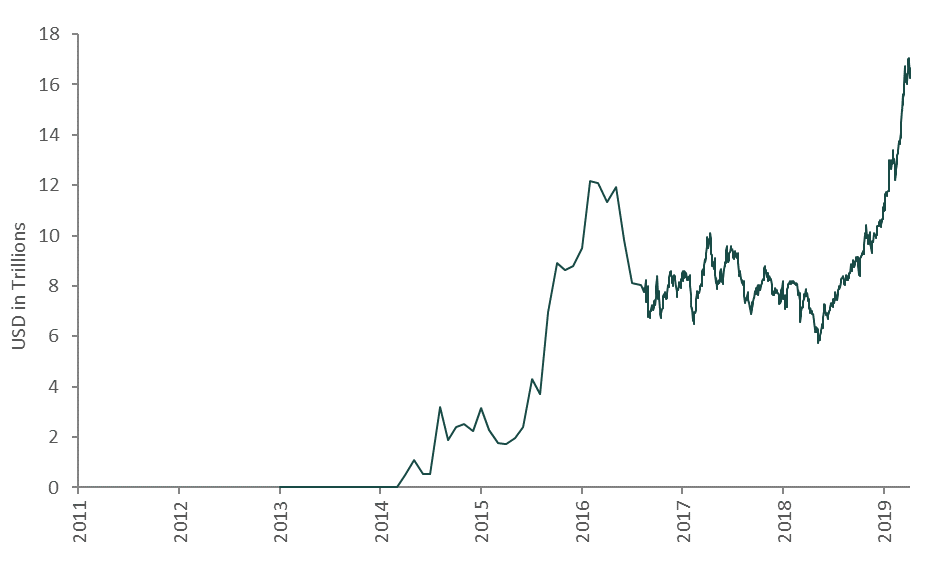

Globally, there are currently USD 15.5tn negative-yielding government bonds outstanding (Exhibit 2). To put this figure into perspective, we first note that most negative-yielding bonds have a good rating (rated A or higher according to Standard and Poor’s as well as Fitch). Further, among the universe of government bonds rated A or better, negative-yielding bonds represent about 41%. This is not an anomaly anymore; it is a significant amount.

Exhibit 2: Global govt. debt outstanding with negative yielding

It is worth spending some time understanding why some investors hold these bonds. Indeed, to pay for losing money is not a good starting point for investing. That said, there are many valid reasons for investors to hold negative-yielding government bonds.

- Firstly, as mentioned above, they are high-quality bonds and bear very little risk: they are thus considered low risk. They are also highly liquid. Modern portfolio theory says that it is crucial to allocate some money into a low-risk asset to reduce the overall portfolio risk.

- Secondly, highly rated government bonds are safe assets, they increase in value when risky assets sell-off. If investors are pessimistic, it may be rational for them to invest in negative-yielding bonds as the expected risk-adjusted return is superior versus equities, for instance.

- Thirdly, some investors may also judge that the world economy is set to experience a period of deflation. As deflation is a decline in the general level of price, if price declines by 2%, a negative-yielding bond which offers -0.5% will deliver a positive return of 1.5%. This is nothing but improved purchasing power from an investor’s point of view.

- Finally, several large investors may have no choice but to invest in these bonds. Commercial banks and pension funds are forced to hold high-quality liquid assets in line with their investment policies.

As listed above, there are many valid reasons to hold these financial instruments, but the central question of why to pay for losing money, at first sight, remains nonetheless unanswered. Cash is a safe, liquid, and non-interest bearing financial asset, which is a superior alternative. The key question is, therefore, why do investors not move to cash to avoid negative-yielding bonds?

Let's be in cash

The answer to this question is that we are not all equal against cash. In today’s world, most of the existing cash is not physical, it is electronic. A deposit at a commercial bank is not backed by physical banknotes in a vault, it is simply a line item in the bank ledger. If needed, the bank client can go to the ATM and transform this electronic cash in physical cash – banknotes. Electronic cash is a promise to pay physical cash on demand.

Institutional investors such as commercial banks, asset managers, pension funds only hold electronic cash as holding physical cash is cumbersome. First, transaction processing times increase substantially whenever cash is involved, and second, it is costly to insure for transportation and storage. More importantly, this cash is not liquid anymore, as it cannot be wired instantly.

Given these issues, institutional investors prefer parking their cash in commercial banks, a significant portion of which is subsequently deposited in the central bank’s deposit account that charges negative interest rate (NIRP). Therefore, in the world of today: cash is not a genuine alternative to negative-yielding bonds. The world of tomorrow may well be very different, and this is because of cryptocurrencies.

Today in a near future

In addition to the traditional physical and electronic cash, cryptocurrencies offer two new forms of cash. In the first category, we find stable coins that are backed by and pegged to fiat currencies (e.g. tether, TrueUSD, Gemini dollar etc.), and in the second we find native cryptocurrencies (e.g. bitcoin, litecoin, ripple). Both these forms of currencies are zero-interest bearing and are reasonably liquid. In a near future, they may become highly demanded and will have large implications on monetary and fiscal policies.

A stable coin is a crypto token issued by an entity that holds cash either in physical or electronic form. A token backed by electronic cash will not be any better than electronic cash itself as NIRP will apply. However, if the token is backed by physical cash, NIRP no longer applies. There are surely costs associated with the transportation and storage of banknotes, but more importantly, this crypto token is liquid compared to physical cash. It can be traded 24/7 at virtually no cost. If this market develops rapidly, NIRP and other such negative-yield strategies may come under threat unless governments decide to forbid stable coins.

Finally, native cryptocurrencies may well become mainstream, and their market liquidity may increase. In comparison to stable coins, cryptocurrencies are volatile. However, volatility is not an antonym of a risk-free asset. Gold is often perceived as a safe-haven asset, but its price is volatile. In the same way, cryptocurrencies may be both volatile and diversifying. It is difficult to attach negative interest rates to cryptocurrencies, and it is extremely difficult to completely forbid their use. As the market of cryptocurrency is growing and is 24/7 in nature, the liquidity potential is elevated. This is a genuine alternative to cash and obviously to negative-yielding government debts.

According to our scenario, the developments of other forms of cash assets may enable investors, in particular, institutional investors, to avoid negative-yielding government bond investments. As a result, the lower bound for interest rates in the future could well become zero.

Impact on Monetary and fiscal policy

If the world we just depicted above materialises in the next few years, central banks in Europe (Switzerland included) and Japan may have to go from NIRP to ZIRP, form a negative to a zero interest rate policy. Government bonds may no longer be priced at a negative yield. Both of these implications restrict monetary and government policies. In our scenario, NIRP will not be an option again, and the government will have to pay something to issue bonds, limiting their ability to get indebted.

It is therefore not improbable that the proliferation of cryptocurrencies could materially discipline central banks and governments. This is, in our view, one of the reasons these institutions are reluctant to let the cryptocurrency market develop

Conclusion

From an investor’s point of view, the addition of cryptocurrency is undoubtedly good as it potentially allows, among other things, to avoid negative-yielding bonds. For central banks and governments, it is not good news as it removes some policy tools from already depleted toolboxes. For society as a whole, the question is open. If you believe that NIRP has been effective and contributes to foster growth and inflation, cryptocurrencies are bad. On the other hand, if you believe that NIRP is ineffective or dangerous as it distorts prices, cryptocurrencies are good. Meanwhile, cryptocurrencies are here to stay, they are growing in importance, and will potentially change the way money is invested and managed.