AMINA Bank AG

AMINA Bank AG  AMINA UK

AMINA UK  AMINA Hong Kong

AMINA Hong Kong  AMINA EU

AMINA EU Abstract

Low growth, low inflation, low interest rates and low yields characterise the economic and financial environment we have faced in the past decade. According to the latest IMF forecasts, this situation is unlikely to change.

While the global outlook is benign, we believe that the financial outlook is fragile. The wealth of nations has increased more rapidly than economic activity, suggesting that asset price inflation has dominated the creation of wealth. The very low interest rate level is key in this context. Credit has also increased in the wake of the favourable monetary conditions, so that even in the case of no recession, interest rates and yields are likely to remain low.

Against this background, it is worth spending some time imagining what the future of crypto-currencies could be.

We show among other things that bitcoin and ether formed the basisofmany developments last year. These developments take the form of layer 2 solutions to increase transaction speed for bitcoin and to offer new services for ether. As far as ether is concerned, the rapid growth of decentralised finance in particular shows the upward trend in interest and usage of these services.

Finally, we take a shot at making 12 predictions on the future of cryptoverse.

Economic outlook

Fears of a recession have declined substantially in the past few months. According to the New York Fed’s recession index, the probability of a recession in the US in the next 12 months has declined significantly from 38% in August last year to 23% today. Economic forecasts for 2020 and beyond are broadly positive even though economic growth and inflation are losing momentum. In the World Economic Outlook update published a few days ago, the IMF slightly revised downwards its global growth forecast to 3.3% this year and 3.4% next year.

Another important variable for the economic picture is inflation which is expected to average 1.8% and 1.9% in 2020 and 2021 respectively in the advanced economies. In other words, price inflation is expected to be close to but below 2%, and very much in line with the definition of price stability of central banks in the advanced economies.

Broadly speaking, the world economic outlook is benign. The world financial outlook is however not as reassuring. According to the Credit Suisse Global Wealth Report, global wealth has increased by about 85% to almost USD 361 trillion while nominal GDP worldwide increased by 31% to close to USD 87 trillion in the past decade.

It is undoubtedly good news that the wealth of nations has increased. But the proportion of wealth to activity is alarming. The ratio has grown from 2.9% in 2010 to 4.2% at the end of last year, suggesting that the increase comes more from asset price inflation than activity. This is a consequence of the loose monetary policy and fiscal policy in the past decades that saw central bank balance sheets and government debt ballooning.

Even if you do not have any sympathy for this mix of policies, it is fair to say they have been effective. The world economy has escaped the worst financial crisis with a great recession and not a great depression. The 2010s is the only decade on record1 without a recession according to the US recession statistics. In addition, the current expansion phase is the longest in the past 170 years.

Now, the question to ask is how much longer can this situation continue, or put differently, what could destabilise this delicate balance?

Debt, like all other assets, depends directly on the level of interest rates. Firstly, its value is inversely correlated to the level of interest rates. With zero or negative interest rate policies and asset purchases (quantitative easing), central banks have mechanically increased the price of all existing assets. Secondly, with low interest rates, the cost of debt has declined massively, encouraging debt financing for households, corporations and governments.

Under the current conditions of high debt, low growth, low inflation and low yield, the fragile financial equilibrium is made possible. As leverage has increased, movements in interest rates have become more sensitive. Total credit to the non-financial sector2 is as high as USD 187 trillion according to the Bank of International Settlement, meaning that an increase in interest rate of one percentage point is worth an additional payment of USD 1.87 trillion, or 2.2% of the global nominal GDP. Such a rise would clearly put some illiquid sectors in a difficult situation, making interest rate hikes difficult to materialize in the current conditions.

Predictions are more art than science, and this is why the analysis of the current situation is important. The current economic outlook does not support a rise in interest rates as growth and inflation are moderate and expected to remain so, and the financial outlook does not allow it as the level of debt is high.

Real life examples of this situation are observed in the eurozone. Italy’s government debt is 133% of GDP and activity growth is expected to be the weakest of the four biggest economies of the region (Germany, France, Italy and Spain) in 2020 at +0.5%. In a such a situation, it is impossible for the European Central Bank (ECB) to increase the interest rate and for government yields to rise as it would lead to a new eurozone crisis.

As central banks are likely to keep monetary conditions loose for an extended period of time even in the case of no recession and investors’ search for yield will continue, we expect yields to remain under pressure. To push this logic to the limit, yields should all ultimately converge to zero and asset prices continue to rise.

Zero yield is unlikely to materialise for all assets as there always exists a risk premium against which any wise investor would ask for a positive return. It shows nonetheless that the current financial outlook is fragile and it is a good time to look at investment differently. In this context, crypto-currencies may be an interesting investment.

Current state of the crypto market

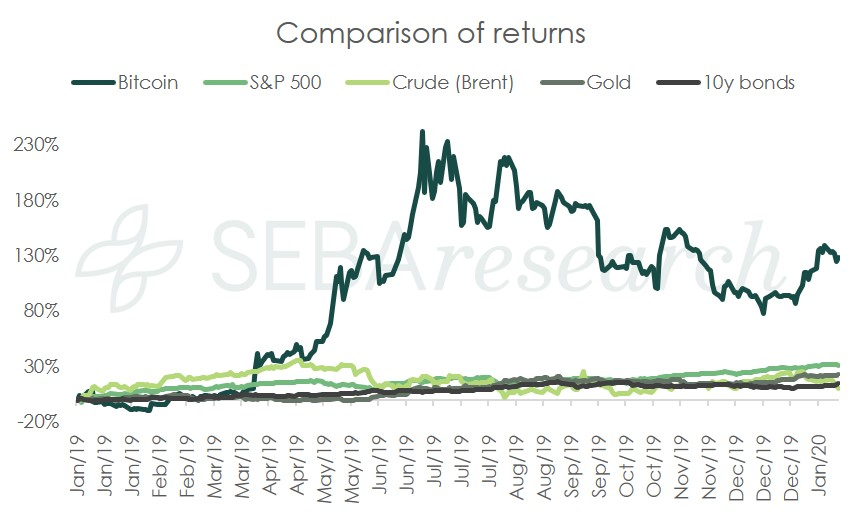

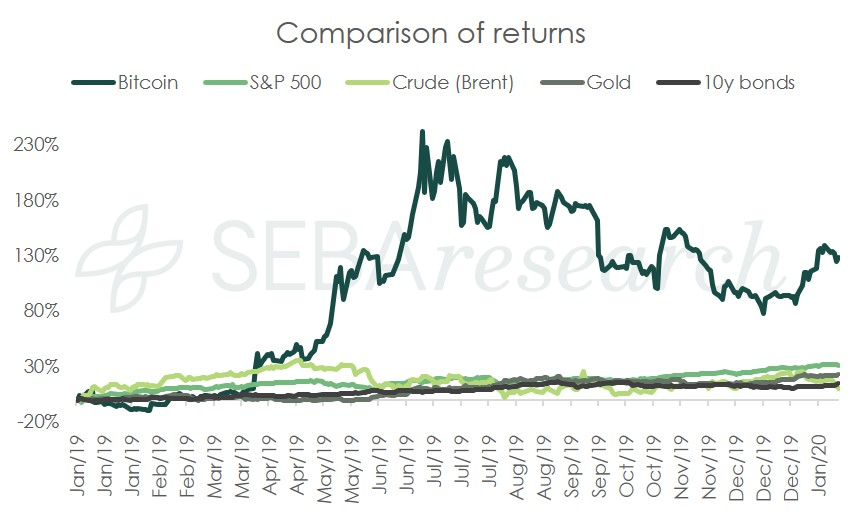

A short retrospective of asset class returns in 2019 shows that bitcoin was the best performing asset. Its price increased by close to 90%. It is followed by the S&P 500 which soared by 29% (figure 1).

FIGURE 1: Comparison of returns of different asset classes

Bitcoin

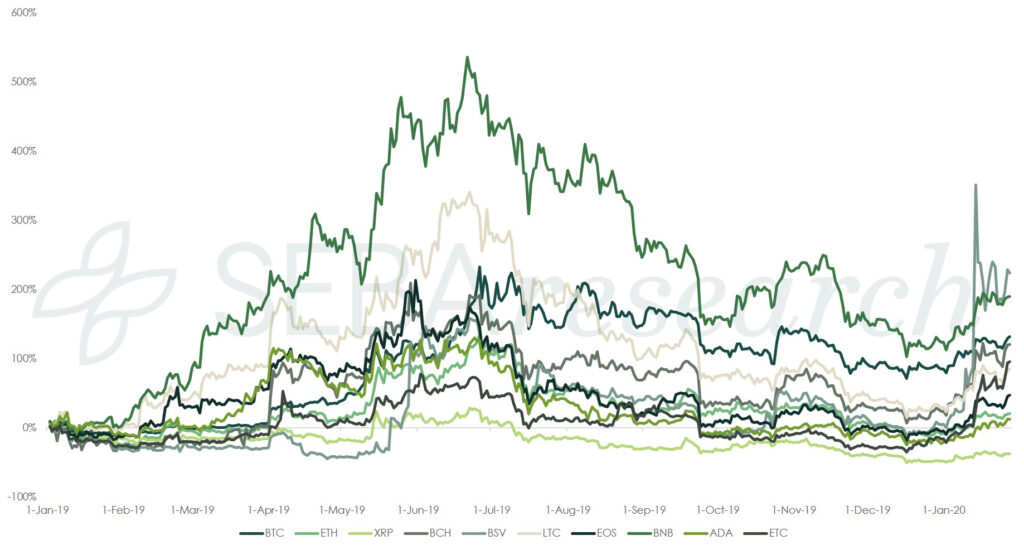

In the cryptoverse, bitcoin was also one of the top performers. However, other smaller coins such as ChainLink and Binance outperformed all. Overall, the major digital assets by market capitalisation had a good year, as figure 2 shows.

FIGURE 2: Performance of major digital assets

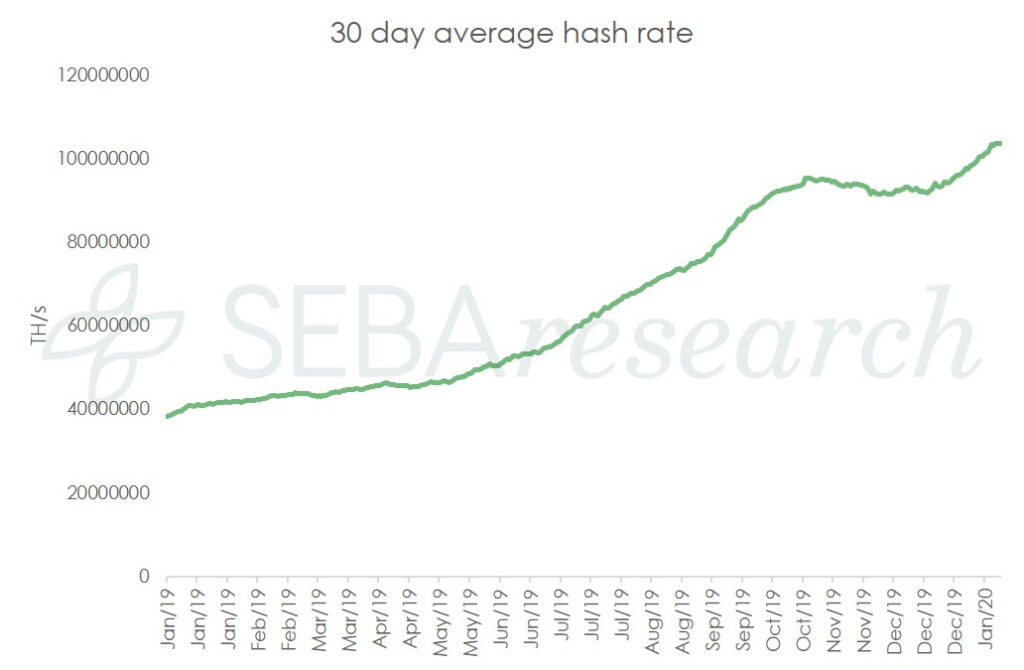

Bitcoin (BTC) is and remains by far the most important crypto-asset based on many metrics. Bitcoin dominance measured in terms of market capitalisation remained steady at between 60% and 70%. Fundamentals have strengthened continuously throughout the year. For example, the hash rate (figure 3), a measure of mining activity, more than doubled last year, indicating the strong commitment of the mining community.

3: Bitcoin hash rate shows strength of the network

The number of users and number of addresses with more than 1 BTC and 0.1 BTC has increased as well. In addition, the number of average daily on-chain transactions was about 300,000 last year in comparison to 5,000 in 2011, signalling how usage has increased in the past few years.

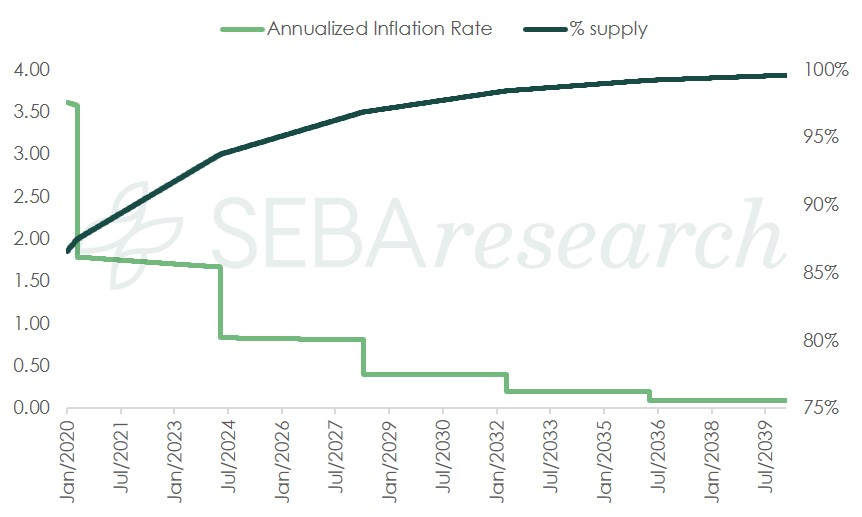

In May 2020, bitcoin’s block reward is set to halve (figure 4). In the history of bitcoin, halving episodes have always been followed by a price rally. More on this topic in our latest Digital Investor – Bitcoin halving, buy in May and go away?

FIGURE 4: Annualised inflation rate and supply percentage of bitcoin

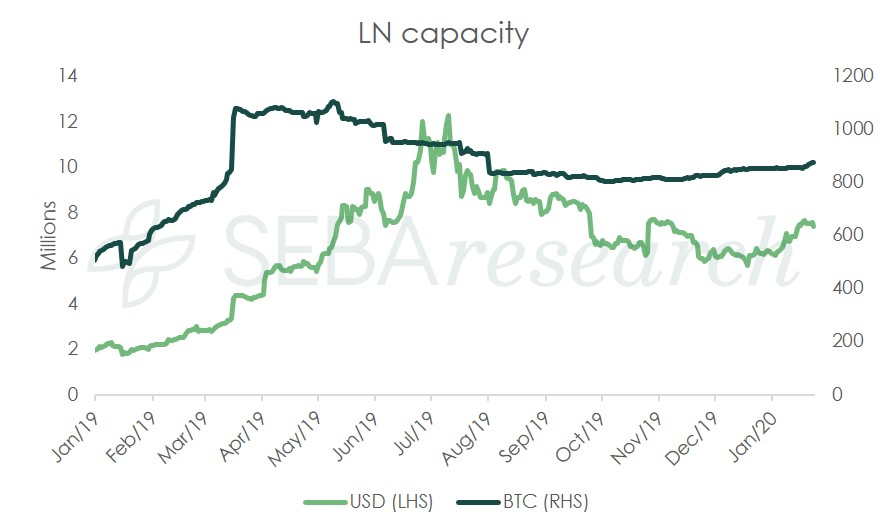

Lightning Network

Lightning Network is a layer two scaling solution for bitcoin. It is aimed at increasing the number of transactions per second. In the first half of 2019, Lightning Network’s capacity3 increased substantially and stabilised at about USD 10 million thereafter (figure 5).

FIGURE 5: Lightning Network Capacity

Jack Dorsey, Twitter CEO, recently announced that Square Crypto will be working on Lightning Network. It is developing a Lightning development kit (LDK) to add Lightning capabilities to existing wallets and to allow single wallet to be accessed through multiple devices and applications.

All these developments are very encouraging and should help make the use of bitcoin even more widespread.

Ethereum

Ether (ETH), Ethereum’s native crypto-currency, had an uneventful year as far as its price is concerned. Its value in USD declined by 9% last year to finish at around USD 130 at the end of the year.

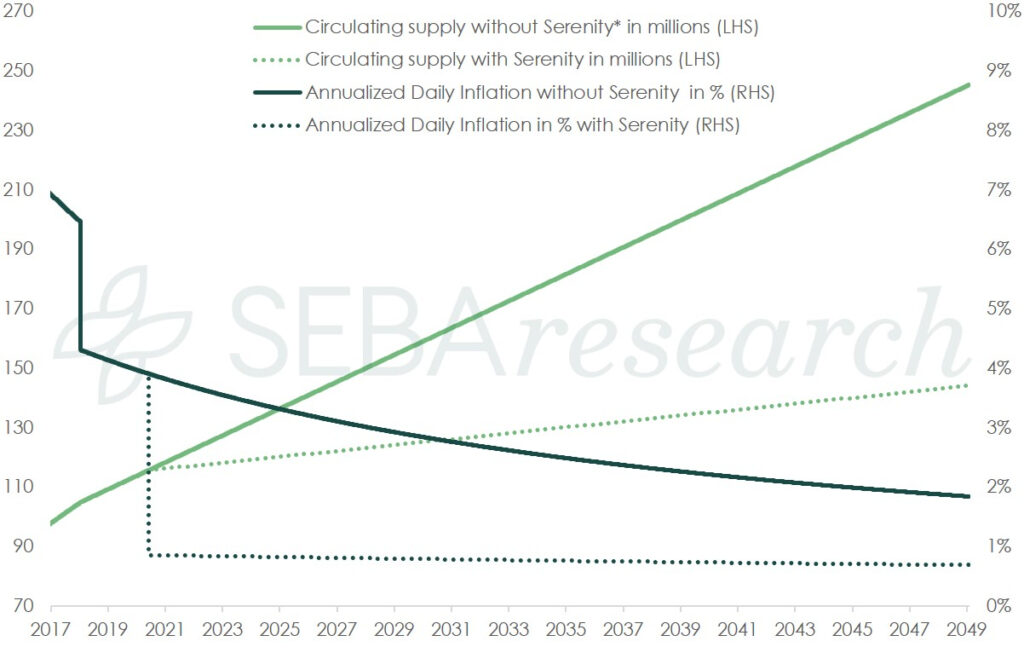

Ethereum’s ecosystem, however, has experienced a few noteworthy developments in the past couple of years. After Constantinople fork, Ethereum block reward came down from 3ETH/block to 2ETH/block, heavily impacting the annualised inflation rate (figure 6). The next big upgrade in Ethereum is Serenity, during which Ethereum will move from proof of work consensus to proof of stake.

FIGURE 6: Ethereum supply and annual inflation

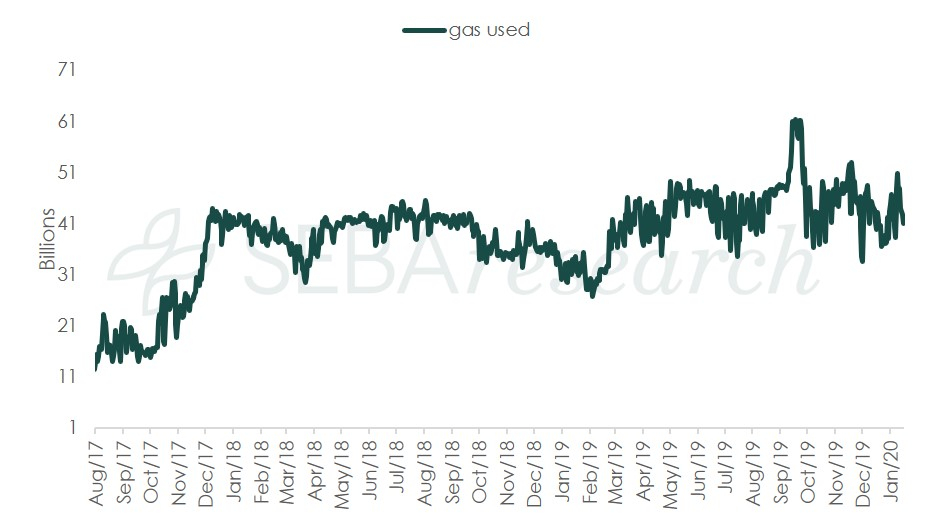

In order to use the Ethereum network, users need to pay “gas” in ether. Gas spent daily was constant last year, suggesting a stable and healthy use of this network (figure 7).

FIGURE 7: Gas used by the network daily

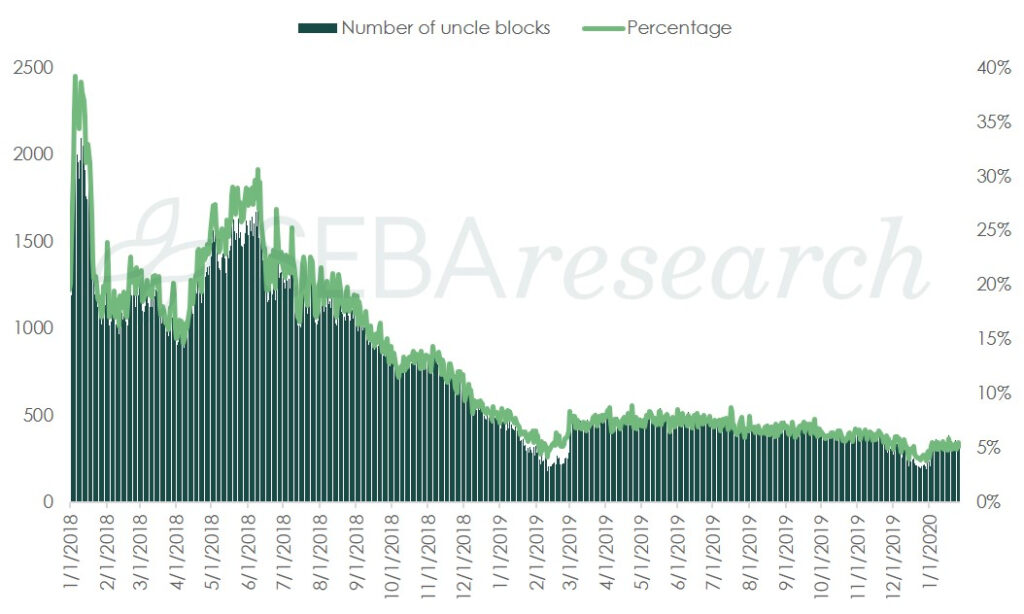

Client optimisations ensured that block limit increased without a corresponding increase in uncle blocks4 and rewards. This development ensures that the number of valid blocks which are not used to build further on is reduced. And as uncle blocks are also rewarded, if the number of uncle blocks is reduced, the reward that goes towards blocks which are of no use further gets reduced; thereby reducing the waste (figure 8).

FIGURE 8: Number and percentage of uncle blocks

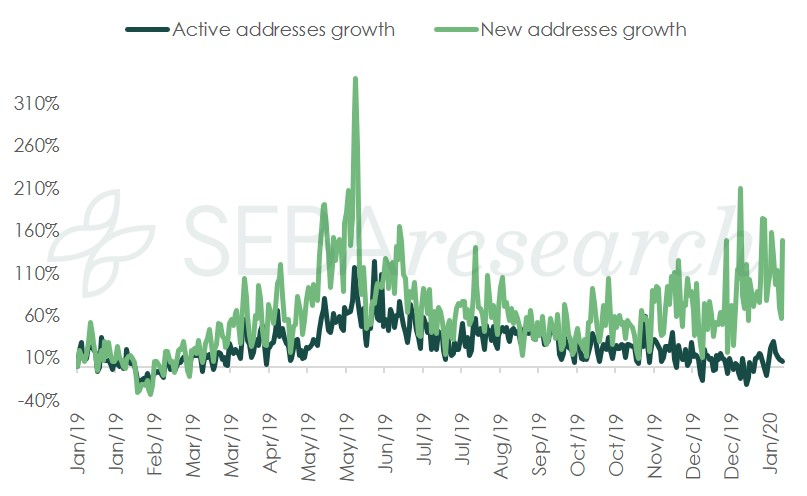

The number of new addresses grew significantly last year, signalling that new users are joining the network, while the number of existing active addresses remained constant, suggesting that experienced users continuing to use it (figure 9).

FIGURE 9: Growth of new and active addresses

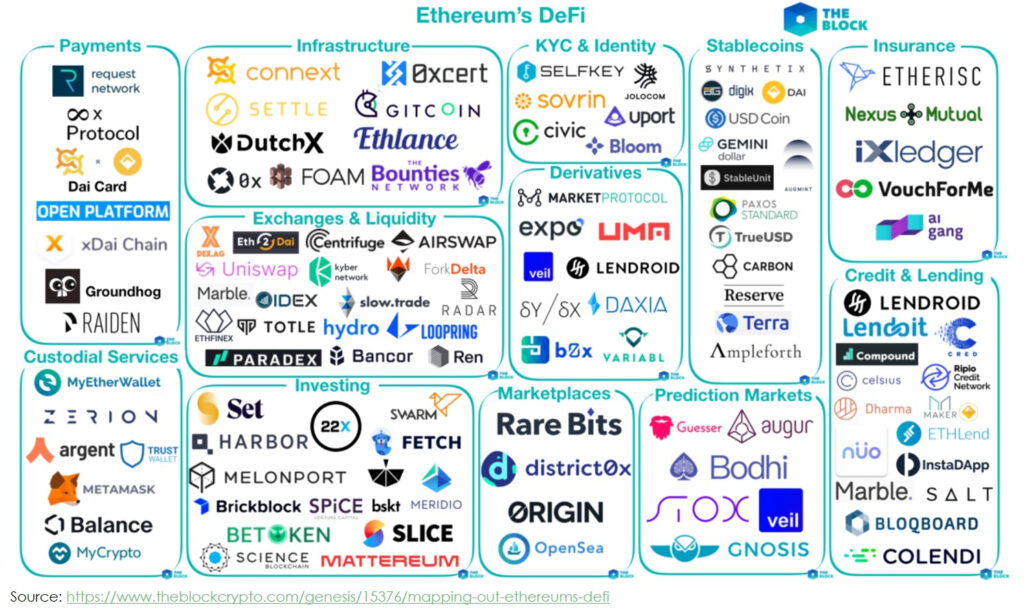

The Ethereum network is a smart contract platform on the top of which decentralised applications (dapps) run, similar to the way apps run on operating systems. Among the dapps, 2019 has seen a broad creation of decentralised finance (DeFi) applications. The more dapps that exist, the more attractive the platform becomes.

DeFi (decentralised finance)

Decentralised finance or open finance, commonly known as DeFi in the crypto landscape, is a utopian movement to make finance more accessible. The idea is to create open finance protocols and make the existing economy much more accessible to everyone, i.e. to unbanked people. Someof theDeFi built on the Ethereum platform (figure 9) include many use cases, such as:

- Credit and lending: allowing borrowers and lenders to meet and to transfer capita 2.Exchange and liquidity: increasing liquidity by providing trading opportunities.

- Custodial services: allow users to store their ether and other tokens on top of Ethereum.

- Investing: allows users to invest using the tokenisation model.

- Prediction markets: users can create events and bet on them using prediction markets such as Augur.

FIGURE 10: The DeFi landscape

Last year was undoubtedly the year of DeFi. Layer 2 scaling solutions which are aimed at increasing the throughput of the base layer blockchains failed to impress, while the value of ETH locked in DeFi contracts increased phenomenally in 2019, confirming the increasing use of these applications.

Since January 2019, the value locked in DeFi has almost tripled from USD 275 million to USD 795 million with Maker – a DeFi aimed at growing a stablecoin through decentralised governance, and the most significant contributor.

Of the total value locked in DeFi, around 57% is through Maker. Its dominance nonetheless shrunk from 90% at the beginning of 2019 as other protocols such as dYdX5 and Compound6 have grown in importance. These three DeFi together have raised a cumulative USD 1 billion since their inception, and the majority of the fund transfers occurred last year.

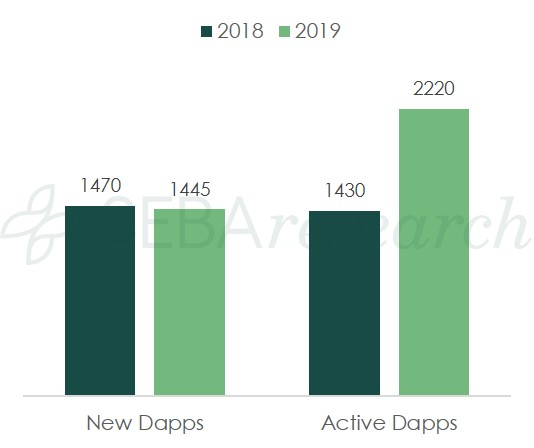

Decentralised applications (dapps)

Though the number of new dapps has been the same in 2018 and 2019 (figure 11), the number of active dapps increased significantly in 2019, showing increased usage. Again, this means that usage has increased because the demand is there and increasing (figure 11).

FIGURE 11a: Decentralised applications showing moderate growth

FIGURE 11b: Decentralised applications showing moderate growth

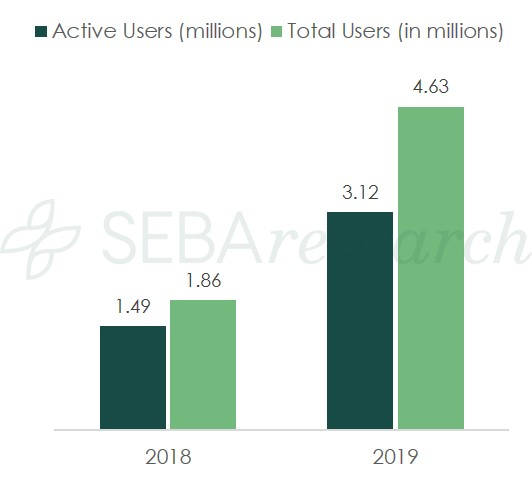

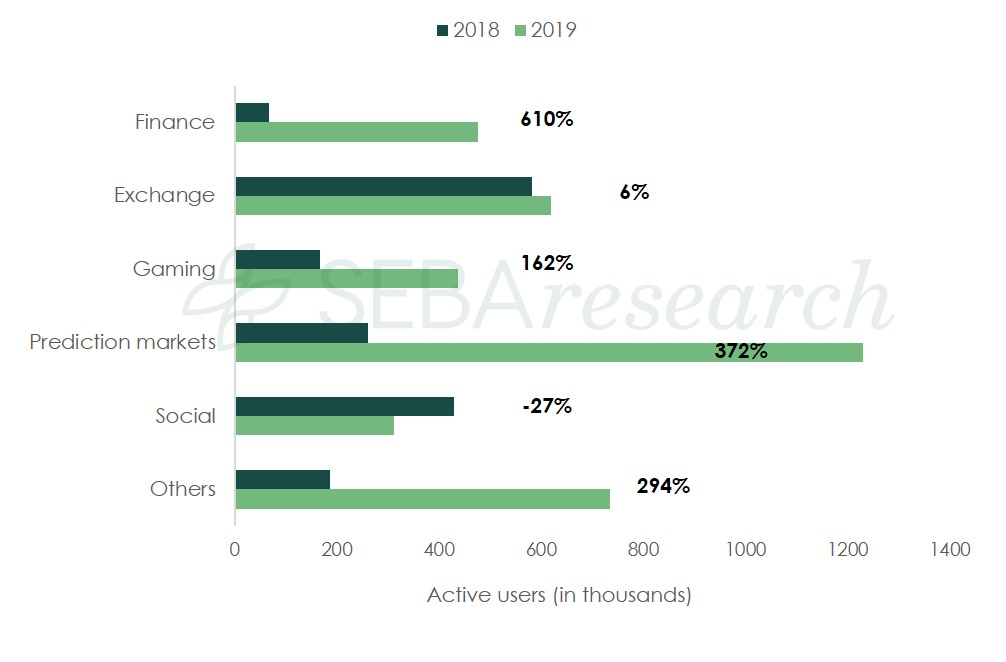

The most active user growth was brought about by prediction markets category, followed by finance and gaming (figure 12)

FIGURE 12: Active users by different categories

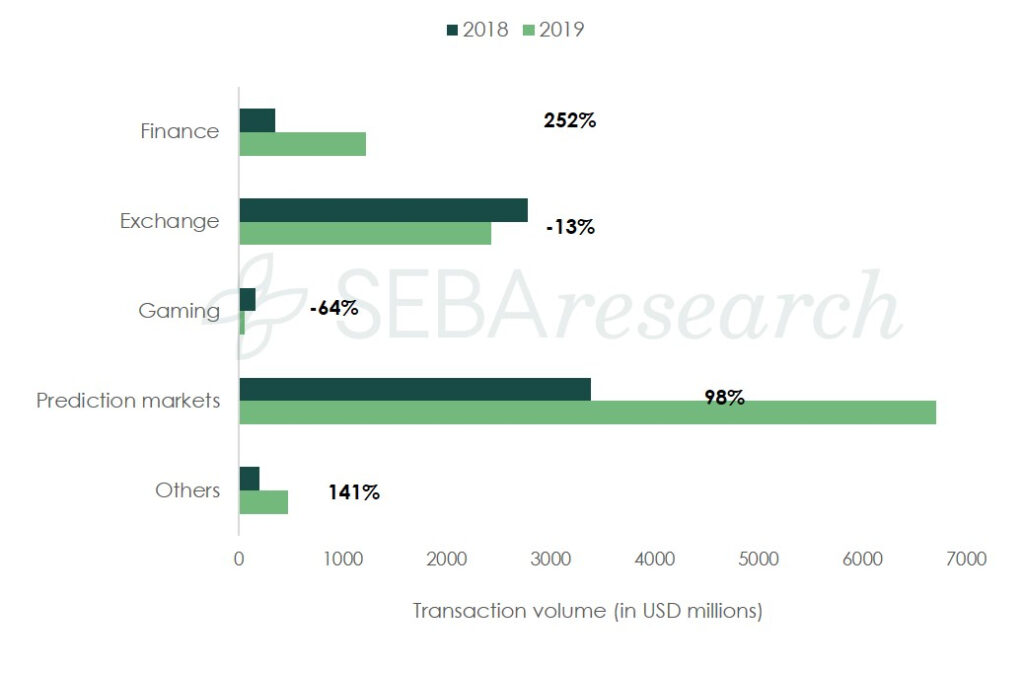

Prediction markets also attracted the lion’s share of transacted value (figure 13).

FIGURE 13: Transaction volume by different categories

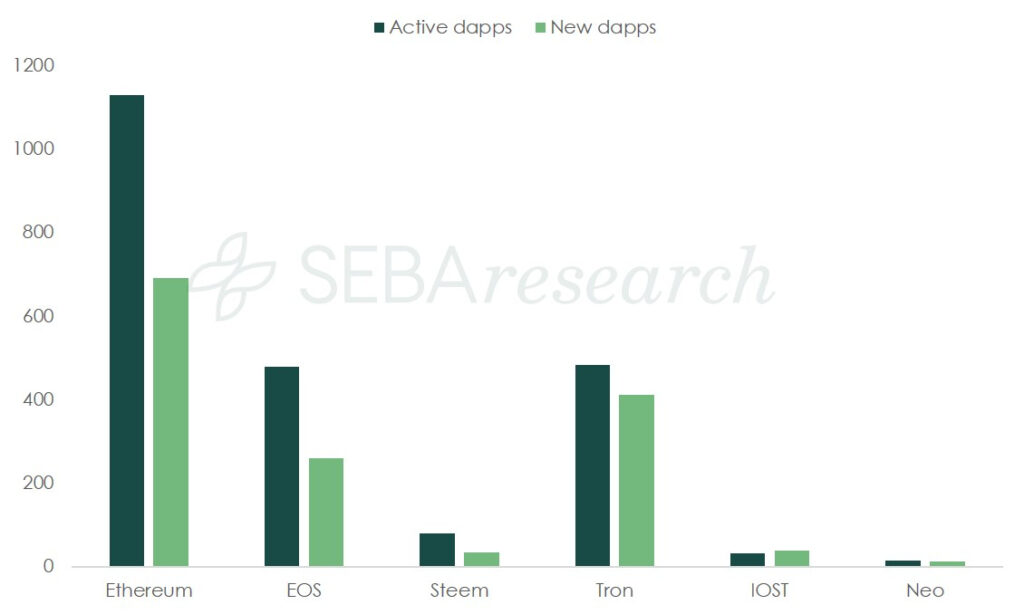

Platform wars: Ethereum seems to be emerging as a clear winner

Ethereum remained the preferred choice for developers building applications. Ethereum blockchain also managed to host the greatest number of active dapps, while Neo remained the least attractive platform (figure 14) for developers from among Ethereum, EOS, Tron, Steen IOST, and Neo.

FIGURE 14: Comparison of new and active dapps

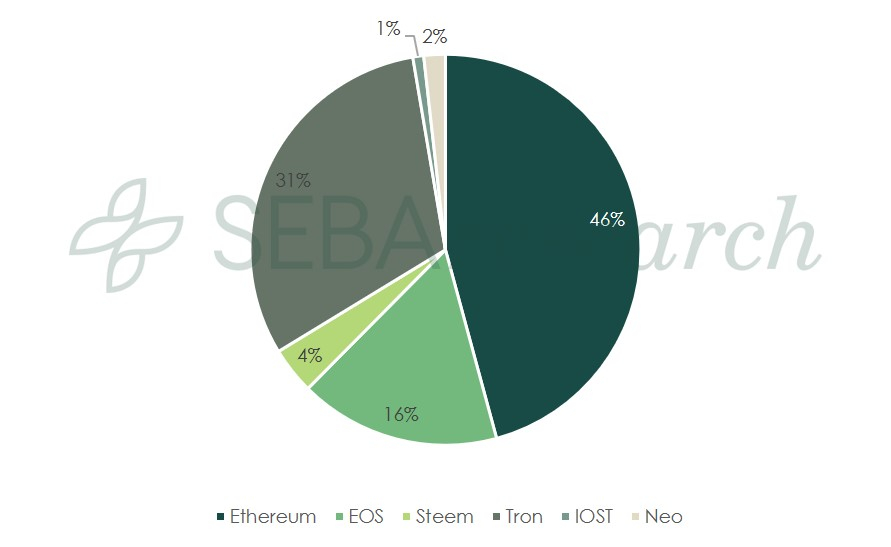

Among these blockchains, Ethereum also attracted the most number of users (figure 15).

FIGURE 15: Active users on different blockchains

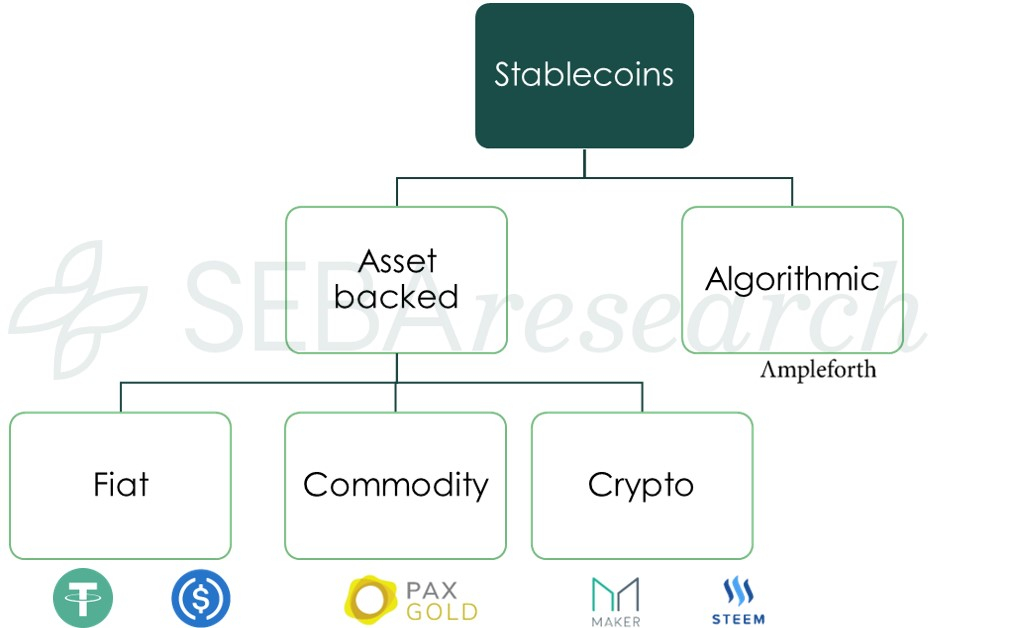

Stablecoins

Stablecoins came to prominence in 2018 and continued to grow strongly in 2019. We categorise them in two buckets: asset backed and algorithmic (figure 16). The vast majority (95%) of stablecoins are asset backed7. Asset backed can further be categorised based on the assets used to maintain the peg. Three broad categories are: fiat backed, crypto backed, and commodity backed.

FIGURE 16: Classification of stablecoins

Stable coins are forms of money designed for the Internet. They can be used for remittances, e-commerce, trading, payments, cash management, etc.

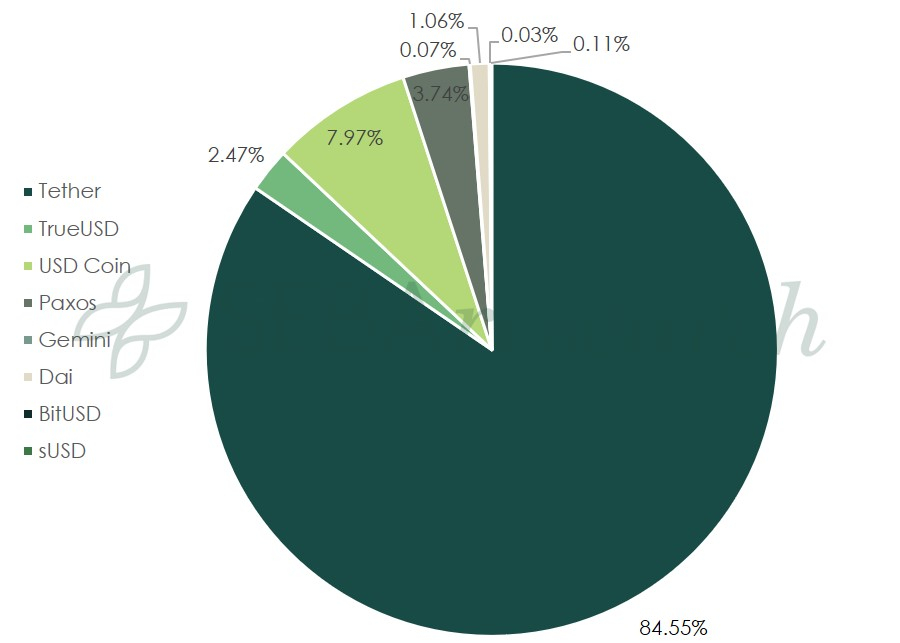

Stablecoin performance

Tether continued to dominate the stablecoin space despite allegations of not being fully backed and of market manipulation. With around USD 4.5 billion, Tether commands 84% dominance among stablecoins.

FIGURE 17: Stablecoin market

Tether was originally built on bitcoin blockchain. However, in 2019, it started to move towards Ethereum blockchain. Possible reasons for this could be low fees on Ethereum, lower block times, and active development.

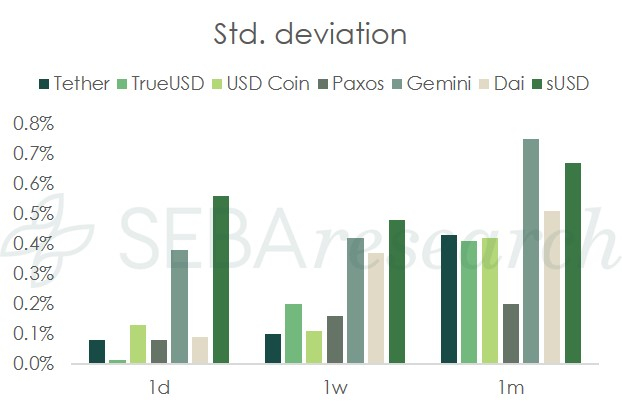

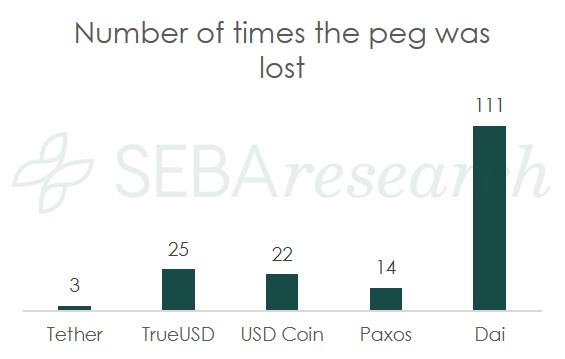

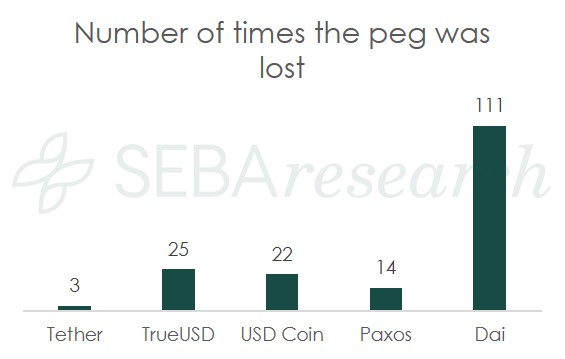

As stablecoins are supposed to have a stable value, the number of times they lost the peg8 along with the standard deviation are good ways to measure their performance in our view. Considering these two parameters, Tether and Paxos performed well in 2019. There is also a correlation between liquidity and stablecoin’s ability to maintain the peg.

FIGURE 18a: Performance of stablecoins

FIGURE 18b: Performance of stablecoins

Initial exchange offerings (IEOs)

In the wake of the initial coins offering (ICO) and security token offering (STO), initial exchange offering (IEO) was another way projects started to raise funds. The number of IEOs last year was limited and few of them performed well. Binance led the way in terms of the returns delivered by the projects launched from different platforms.

FIGURE 19: Average return of different IEO platforms

The way forward for IEOs

After taking a firm stance against ICOs, the Securities and Exchange Commission (SEC) has also warned against new forms of funding such as IEOs. We expect that in 2020 the SEC will take actions against even more IEOs that have securities-like characteristics.

IEOs will have to be vigilant about designing tokens in a manner that it does not represent any characteristics of a security. On the flip side, if the token is designed in a manner that does not capture the upside of the business in any meaningful manner, there is little reason for investors to invest.

A peek into the future…

- Bitcoin halving is expected to have a positive impact on the price of bitcoin as the ecosystem is supported by strong fundamentals

We argued in our bitcoin halving analysis that halving only does not always lead to a higher price. However, the combination of halving and strong fundamentals support coin prices. As this is the case for bitcoin, we believe halving will be supportive in that respect.

- Bitcoin/digital assets become a part of more institutions’ portfolios

The narrative of a new safe-haven asset uncorrelated with traditional asset classes is gaining traction. This property would be very attractive for institutional investors. In our Digital Investor, Are crypto-assets suitable for institutional investors?, we have identified different institutional adoption parameters and all the parameters seem to show positive developments . We believe that pieces of institutional adoption are aligning together, and we will see more institutions allocating capital to digital assets.

- Bitcoin options will gain prominence in 2020

Though CME and Bakkt launched options, Deribit is by far the biggest player in Bitcoin options. We expect this to change in the coming years as more institutions start trading bitcoin options.

- Bitcoin volatility decreases

As more and more derivatives products are launched, inefficiencies will be ironed out and the price discovery mechanism will become smoother, thereby reducing volatility.

- Lightning Network sees significant growth in BTC locked in channels

With Square crypto announcing the Lightning Development Toolkit, it will be easier for the developers to integrate Lightning nodes into wallets. It will usher in more Lightning adoption for payments.

- Tokenisation will pick up pace

Just dematerialisation of stocks brought the revolution in equity trading, the ability to tokenise assets will make assets liquid. We expect that this decade will bring most of the non-bankable assets under bankable assets through tokenisation.

- SEC tightens screws around IEOs and more regulatory clarity around the globe

The SEC has been busy sending notices to various IEOs for conducting the sale of unauthorised securities. The moral of the story is that IEOs will not be spared just because they are vetted by exchanges.

- The value locked in DeFi grows to USD 4 billion

If there was one success story in 2018-19, it was DeFi. From under USD 50 million to around USD 800 million of value locked, DeFi has outperformed all expectations. With multiple projects offering different products and a better user experience, we believe value locked in DeFi could grow significantly from here.

- Bitcoin and Ethereum see development up the stack

The very nature of open source protocols means that, technically, they are easy to copy. What one cannot copy about them is the social scalability and network effects. What we are hinting at is that new layer 1 protocols that challenge Bitcoin and Ethereum will have difficulties in achieving the network effects of the two. Therefore, it is in favour of developers to develop on top of bitcoin and Ethereum instead of challenging their authority as base layer protocols.

- Ethereum Serenity phase 0 will not launch in 2020

We believe that given the conservative development approach coupled with Istanbul being implemented in two phases, the phase 0 of Serenity (also known as beacon chain) will not launch in 2020.

- Bitcoin includes Taproot and Schnorr signatures

Taproot and Schnorr signature are now officially proposed in bitcoin improvement proposals (BIPs) 340, 341, 342. These proposals will improve the privacy, efficiency, and flexibility of bitcoin’s scripting language by minimising the information needed to be disclosed and verifying whether a transaction output is valid or not. We expect these BIPs to be implemented by Q2 2021.

- Libra will not launch in its current form

As the number of institutions leaving the Libra association due to a regulatory backlash keeps increasing, it is almost certain that Libra will not launch in its current form. The best case scenario, at the moment, seems to be that Libra may become a stablecoin pegged to the US dollar.

Conclusion

With the ever-expanding quantitative easing and negative interest rates in most of the developed world, the global economy is in unchartered waters. At such times, crypto-assets offer an uncorrelated asset class to traditional investors. Different institutional grade products are being built in the crypto space which will help institutional adoption in a meaningful manner. We think that entrepreneurs will increasingly build on top of the established protocols to leverage their network effects instead of taking them head-on and building the network themselves.

1The National Bureau of Economic Research (NBER) dates the US economic cycle as far as back to the 1850s. ↵

2Households, non-financial corporations and general governments. ↵

3Lightning Network Capacity implies the number of bitcoins held in Lightning channels. ↵

4Uncle blocks are valid blocks but the further chain is not built on top of them, thus amounting to waste. It is preferable to have a lower percentage of uncle blocks. Uncle blocks typically receive 2/3rd of the original block reward. ↵

5dYdX is an open trading platform built on Ethereum. ↵

6Compound is a lending platform built on Ethereum ↵

7Source: Blockdata. ↵

8The peg is considered to be lost if the price change is more than 1% of the desired value. ↵