AMINA Bank AG

AMINA Bank AG  AMINA UK

AMINA UK  AMINA Hong Kong

AMINA Hong Kong  AMINA EU

AMINA EU

With the GENIUS Act enacted in the United States, community and regional banks are increasingly being asked by clients what their digital strategy looks like. Most don’t have a clear answer.

The instinct for many financial institutions is to build their offerings independently. But the numbers make that difficult to justify. Setting up the infrastructure to offer crypto services independently costs a community bank approximately $2 million in capital expenditure, before accounting for crypto’s 24/7 operational model, dealing with regulators, control frameworks, and the specialist talent required to build and run it.

In speaking directly with community and regional banks, Mike Foy, CFO of AMINA Bank, observes that small-to-mid sized banks either go down a rabbit hole chasing the wrong opportunities, or they feel they’ve missed the boat on digital assets. Neither position is where they need to be.

The answer, for most regional and community banks, is not to build. It is to partner and to focus on stablecoin capability on the areas where it solves problems that already exist, such as payments efficiency, treasury operations, and correspondent banking.

A payment stablecoin is a digital asset designed to maintain a stable value pegged to a fiat currency, most commonly the US dollar, and is used as a settlement mechanism on blockchain infrastructure. Its relevance for banks is tied to its ability to function as a programmable and continuously available transfer layer.

The Real Question: Where Stablecoins Create Value for Banks

Regional and community banks operate under tighter resource constraints than global institutions and usually cannot justify broad experimentation. A possible approach requires mapping specific client pain points that already exist within the bank’s operating model.

A bank serving exporters may observe delays in supplier payments that disrupt working capital cycles. A treasury team may be unable to move liquidity outside banking hours, forcing clients to hold balances elsewhere. Remittance clients may face persistently high fees in certain corridors, while digital asset businesses may require continuous settlement capability that traditional rails cannot always provide. These are the conditions in which stablecoins should be evaluated.

In this context, stablecoins should be treated as a payment rail rather than a balance sheet product. The distinction is important because it limits operational complexity while focusing on measurable improvements in client workflows.

Cross-Border Payments as the Primary Use Case

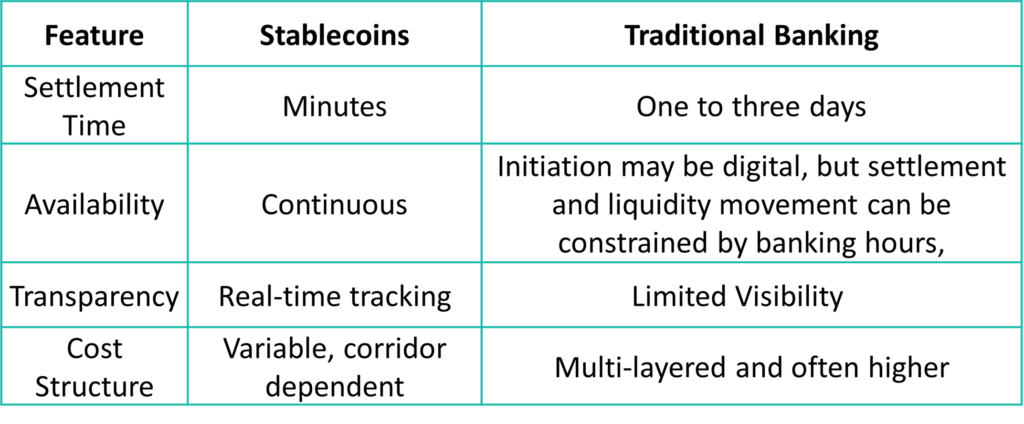

Cross-border payments present the most immediate and commercially relevant application of stablecoins in banking. In October 2025, the Financial Stability Board identified structural inefficiencies in cross-border payments, including higher costs, slower settlement, and insufficient transparency. These inefficiencies are reflected in the World Bank’s remittance data (September, 2025), which shows global average costs for cross-border remittances remaining well above policy targets.

Stablecoins address part of this problem by reducing the number of intermediaries involved in a transaction and enabling near real-time settlement. While total transaction cost still includes foreign exchange conversion, compliance checks, and access to on and off ramps, the underlying settlement layer becomes faster and more transparent.

Stablecoins are not without risk. They carry issuer, redemption, operational, regulatory, and liquidity risks that banks must assess carefully. However, for large, established stablecoins with a meaningful operating history, stronger transparency, and clearer regulatory treatment, these risks can be assessed, managed, and made acceptable within a controlled banking framework.

Figure 1: Stablecoins vs Traditional Banking Rails

Source: AMINA Bank

For a regional bank, this capability can be translated into practical services such as faster settlement for importers paying overseas suppliers or more efficient payout mechanisms for platforms operating across multiple jurisdictions. In both cases, the client does not engage with blockchain infrastructure directly. The value is experienced through improved speed and clarity of payments.

Treasury Movement and Continuous Liquidity

Stablecoins also address a structural limitation in treasury operations. Financial markets operate continuously, while traditional banking systems are constrained by defined operating hours. This creates friction for clients who need to move capital outside those windows.

By enabling continuous settlement, stablecoins allow treasury teams to transfer liquidity between counterparties, custodians, and platforms without interruption. This is particularly relevant for clients engaged in digital asset markets, but the same requirement is increasingly visible among global fintech platforms and corporates with distributed operations.

Institutions that cannot support this capability risk losing both transactional volume and client balances to alternative providers that offer continuous settlement infrastructure.

Platform Payouts and Global Settlement Workflows

Global platforms that distribute funds across multiple regions face operational complexity arising from fragmented payment systems, foreign exchange spreads, and reconciliation delays. Stablecoins simplify the movement of value across borders by providing a unified settlement layer.

In a typical implementation, a platform collects funds in a base currency, transfers value using a stablecoin, and converts it to local currency near the point of distribution through a regulated partner. This reduces reconciliation complexity and improves the predictability of payout timing.

The bank’s role in this model is to provide a controlled interface to the stablecoin rail while maintaining oversight of compliance, transaction monitoring, and client onboarding.

Remittances and Access to Digital Dollars

In remittance corridors and economies with volatile local currencies, stablecoins can provide access to dollar-denominated value and reduce transfer times. However, the effectiveness of this use case depends on the quality of the end-user experience.

If recipients cannot easily convert stablecoins into local currency or access funds through familiar financial channels, the underlying speed of settlement does not translate into practical value. Successful implementations therefore depend on reliable conversion infrastructure, clear disclosures, and appropriate safeguards against fraud.

This dynamic has been illustrated by financial platforms that embed stablecoin access within existing user interfaces rather than requiring users to interact directly with blockchain systems. The lesson for banks is that adoption depends more on distribution and usability than on the underlying technology (which may carry its own risks).

Serving Digital Asset Clients Within a Regulated Framework

Digital asset firms already rely on stablecoins as a core component of their operating model. They use them for settlement, collateral management, and liquidity movement. Banks that do not support stablecoin-based workflows may find it difficult to retain these clients.

At the same time, the ability to support such clients requires disciplined risk management. Differences in transparency, ownership structure, and counterparty exposure create materially different risk profiles across potential clients. A bank must therefore combine stablecoin capability with rigorous onboarding standards and continuous monitoring.

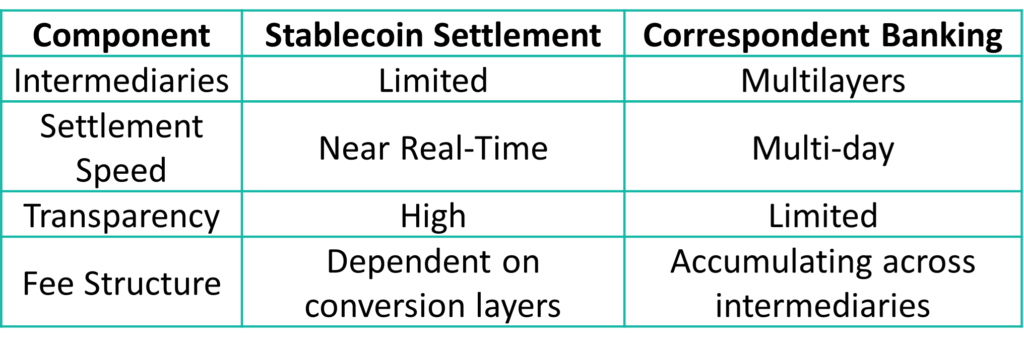

Comparison with Correspondent Banking Models

Figure 2: Stablecoin Settlement vs Correspondent Banking

Source: AMINA Bank

This comparison highlights that stablecoins are more effective in corridors where correspondent banking inefficiencies are most pronounced. They do not eliminate all costs, but they alter the structure of those costs and reduce delays associated with intermediary chains.

What Banks Should Avoid

Stablecoin adoption requires selectivity. Issuing a proprietary stablecoin introduces significant operational and regulatory obligations that are not justifiable for most regional institutions. Retail-facing wallet products require a level of user experience design and support infrastructure that may not align with current demand. Domestic payment systems that already function efficiently do not benefit materially from stablecoin integration.

Exposure to decentralized finance protocols introduces additional layers of risk that are not aligned with early-stage adoption strategies. Lending against stablecoin balances also requires a detailed understanding of issuer structure, redemption mechanisms, regulatory obligations, risks and liquidity dynamics.

A disciplined approach focuses on areas where stablecoins solve existing problems rather than creating new product lines without clear demand.

Implementation Through the Embedded Partner Model

The most practical implementation model to explore for regional and community banks is to integrate stablecoin capabilities through a regulated partner. In this structure, the bank retains control over client relationships, onboarding standards, and risk policies, while the partner provides the underlying infrastructure for custody, wallet management, and blockchain interaction.

This approach is likely to reduce the need for in-house technical development while allowing the bank to test stablecoin-enabled workflows in a controlled environment. Expansion should be based on measurable client adoption, risk appetite, and operational performance rather than strategic assumptions.

Regulatory Direction Across a Few Key Markets

In the United States, recent legislative developments have established a clearer framework for stablecoin issuers and brought them under existing financial compliance obligations. This reduces uncertainty but reinforces the responsibility of banks to manage third-party and transactional risk.

In Europe, the Markets in Crypto-Assets Regulation has introduced authorisation requirements for stablecoin issuers and defined operational standards for related services. This creates a more structured but also more demanding regulatory environment.

Across Asia, regulatory approaches vary by jurisdiction, with countries such as Singapore and Hong Kong establishing formal frameworks for stablecoin issuance and oversight. These markets are likely to see strong adoption due to existing cross-border trade flows and digital payment adoption.

Adoption Outlook

Adoption is already underway and the institutions moving earliest are those that have identified specific client pain points rather than pursue digital assets and stablecoins generally for innovation. Early movers are concentrated among businesses with cross-border exposure, fintech platforms managing global payouts, and clients requiring continuous liquidity movement.

The indicators of genuine demand include clients already visible in many institutions: clients using stablecoins outside the banking system, persistent complaints about payment delays, and the migration of balances to non-bank platforms. For community and regional banks, these are present conditions that warrant a response now.

When it comes to stablecoins, the questions for community and regional banks are how quickly clients expect them to bring these capabilities to market and whether institutions are positioned to meet these expectations.

Conclusion

Stablecoins represent an incremental improvement in settlement infrastructure rather than a transformation of the banking model. Their value lies in enabling faster, more transparent, and continuously available payment flows in areas where traditional systems remain constrained.

Regional and community banks that focus on specific client needs, implement controlled pilots, and scale based on observed outcomes can integrate stablecoins as a practical enhancement to their service offering. Those that approach the topic as a broad innovation initiative without clear use cases are unlikely to realize meaningful benefits.

The build cost is prohibitive for most institutions working independently. The regulatory path is being clarified increasingly. And client demand is already surfacing, whether it is in payment complaints, in balance migration, or in the questions arriving on relationship managers’ desks right now. For community and regional banks, the most practical next step is to work with a regulated partner who already has trusted infrastructure and frameworks in place.

Disclaimer – Research and Educational Content

This document has been prepared by AMINA Bank AG (“AMINA”). AMINA is a Swiss licensed bank and securities dealer with its head office and legal domicile in Switzerland. It is authorised and regulated by the Swiss Financial Market Supervisory Authority (“FINMA”).

This document is published solely for educational purposes; it is not an advertisement nor a solicitation or an offer to buy or sell any financial investment or to participate in any particular investment strategy. This document is for publication only on AMINA website, blog, and AMINA social media accounts as permitted by applicable law. It is not directed to, or intended for distribution to or use by, any person or entity who is a citizen or resident of or located in any locality, state, country or other jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation or would subject AMINA to any registration or licensing requirement within such jurisdiction.

Research will initiate, update and cease coverage solely at the discretion of AMINA. This document is based on various sources, incl. AMINA ones. In preparing this document, AMINA may have made limited use of artificial intelligence–enabled tools to assist with research, summarisation, and drafting, with all content subject to human review and validation.

No representation or warranty, either express or implied, is provided in relation to the accuracy, completeness or reliability of the information contained in this document, except with respect to information concerning AMINA. The information is not intended to be a complete statement or summary of the subjects alluded to in the document, whereas general information, financial investments, markets or developments. AMINA does not undertake to update or keep current information. Any statements contained in this document attributed to a third party represent AMINA’s interpretation of the data, information and/or opinions provided by that third party either publicly or through a subscription service, and such use and interpretation have not been reviewed by the third party.

Any formulas, equations, or prices stated in this document are for informational or explanatory purposes only and do not represent valuations for individual investments. There is no representation that any transaction can or could have been affected at those formulas, equations, or prices, and any formula(s), equation(s), or price(s) do not necessarily reflect AMINA’s internal books and records or theoretical model-based valuations and may be based on certain assumptions. Different assumptions by AMINA or any other source may yield substantially different results.

Nothing in this document constitutes a representation that any investment strategy or investment is suitable or appropriate to an investor’s individual circumstances or otherwise constitutes a personal recommendation. Investments involve risks, and investors should exercise prudence and their own judgment in making their investment decisions. Financial investments described in the document may not be eligible for sale in all jurisdictions or to certain categories of investors. Certain services and products are subject to legal restrictions and cannot be offered on an unrestricted basis to certain investors. Recipients are therefore asked to consult the restrictions relating to investments, products or services for further information. Furthermore, recipients may consult their legal/tax advisors should they require any clarifications.

At any time, investment decisions (including, among others, deposit, buy, sell or hold investments) made by AMINA and its employees may differ from or be contrary to the opinions expressed in AMINA research publications.

This document may not be reproduced, or copies circulated without prior authority of AMINA. Unless otherwise agreed in writing, AMINA expressly prohibits the distribution and transfer of this document to third parties for any reason. AMINA accepts no liability whatsoever for any claims or lawsuits from any third parties arising from the use or distribution of this document.

©2026 AMINA, Kolinplatz 15, 6300 Zug