AMINA Bank AG

AMINA Bank AG  AMINA UK

AMINA UK  AMINA Hong Kong

AMINA Hong Kong  AMINA EU

AMINA EU Executive Summary

- We remain cautious in our approach, preferring Bitcoin and Ethereum over alternative smart contract platforms and decentralised finance or metaverse tokens. High cost-push inflation figures and slow growth due to supply chain challenges continue to create an uncertain macroeconomic scenario which can turn into a recession.

- In terms of monthly performance, June 2022 has been one of the worst months in over a decade for Bitcoin, as the apex digital asset corrected by 35% within 30 days.

- Entities having significant exposure to the Terra Luna ecosystem have been at the origin of the current liquidity crisis. One of the major crypto hedge funds – Three Arrows Capital – is insolvent, and multiple crypto lending services have stopped the withdrawal of funds and are fighting for their survival.

- Contrary to CeFi lending/borrowing platforms, DeFi applications have been running smoothly, showing the viability of open, permissionless finance and the potential for future growth and adoption.

- Solana and Avalanche have lost more than 80% of their value this year. But they continue the development, as Avalanche launched a bitcoin native bridge called Core, and Solana, despite multiple network downtimes, has announced their blockchain smartphone and mobile platform.

Outlook

June 2022 has been one of the most devastating months in the history of crypto markets. The total market capitalisation dropped by approximately USD 500 billion after the massive fall in May, and it is now less than USD 1 trillion. The last time the crypto market capitalisation was below USD 1 trillion was in February 2021, more than 15 months ago. This correction can be attributed to several specific crypto events that we will discuss further in this article. It is essential to note that deteriorating macroeconomic data, tighter financial conditions, and the ongoing war in Ukraine paint an unattractive investment landscape. All traditional asset classes have been affected by rising inflation, slower than expected growth numbers, and the tense geopolitical situation.

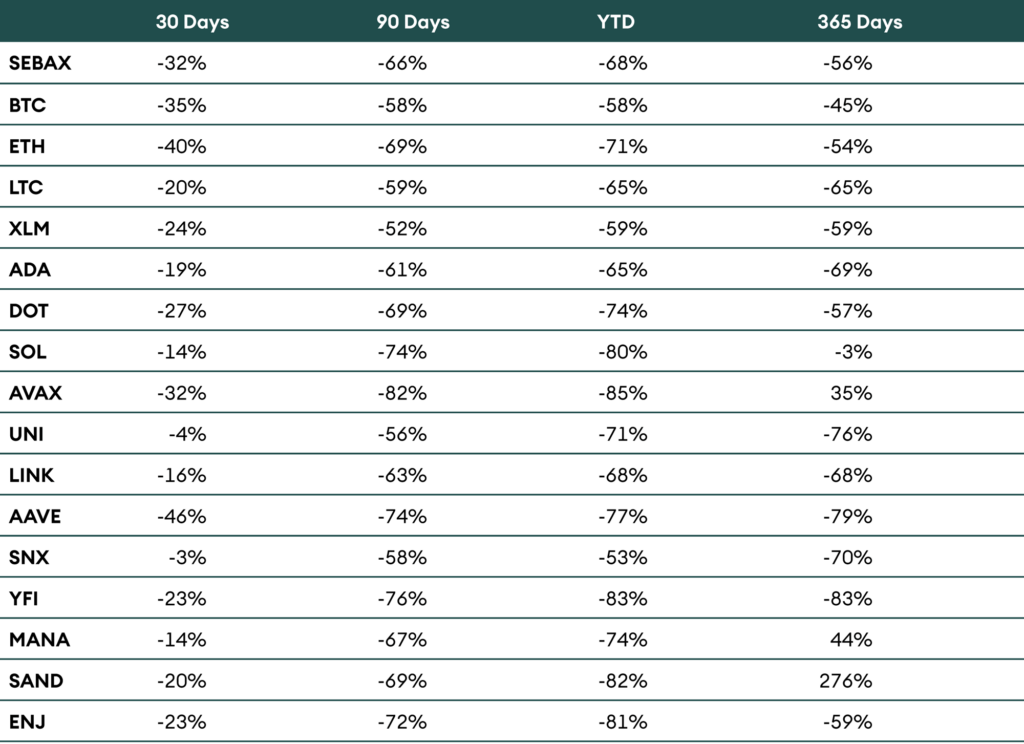

The performance of the AMINAX® Index, a selection of blue-chip cryptocurrencies, quantified the extent of the capitulation: it corrected by 32% in the last 30 days. Over the same period, Bitcoin (BTC) and Ethereum (ETH) corrected by 35% and 40%, respectively. AAVE, a decentralised borrowing and lending platform, has been particularly impacted as its price dropped by 46%. The other coins we cover (see Table 1) have done relatively better, but all record a negative performance. On a year-to-date (YTD) basis, bitcoin has been more resilient (-58%) than the overall crypto market as multiple other digital asset prices have fallen more, with Ethereum down by 71%. Last year outperformers such as platform chains Solana (SOL) and Avalanche (AVAX) recorded significant price corrections of more than 80%. We have started covering metaverse tokens, Decentraland (MANA), The Sandbox (SAND), and Enjin Coin (ENJ) in our monthly analysis in a limited capacity. The market capitalisation weighted AMINA Metaverse Index (SMETA) includes these three coins and provides a good overview of price development in this sector.

Table 1: Performance of AMINAX® and AMINA universe coins as of 3 July 2022

The consequences of the Terra Luna (LUNA and UST) fiasco are still being felt in the market. Multiple entities with significant exposure to these assets suffered a major liquidity crisis in June. It became public with Celsius, a centralised crypto lending platform, stopping the withdrawal of user funds on 13 June 2022. This event set panic in the market, and depositors started moving their funds from similar platforms, like BlockFi, Nexo, Babel Finance, Vauld, and many more.

A major crypto hedge fund, Three Arrows Capital (3AC), borrowed from some of these centralised lending services and had exposure to the Terra Luna ecosystem. In the following weeks, 3AC failed to fulfil its debt obligations, causing centralised finance (CeFi) entities to lose billions of dollars. In the last week of June 2022, the British Virgin Islands ordered the liquidation of 3AC. We talked about the state of these entities in one of our last month’s Crypto Market Monitors; click here to read more.

Given these market conditions, negative sentiment among investors continues to dominate, and it seems the full extent of this liquidity crisis is not over yet. On the 4 July, one more CeFi entity called Vauld stopped activity for all users citing financial challenges. They witnessed outflows of approx. USD 200 million since 12 June, and they also laid off 30% of their employees last month. One of the most prominent players in this ecosystem, BlockFi, suffered heavy losses due to their exposure to 3AC and thus they are in talks to be acquired by FTX, a leading crypto exchange.

In our last month’s digital investor, we asked the question if we are in crypto winter, and its answer is more evident than ever. We have been cautiously navigating the crypto markets for the past couple of months and continue the same outlook this month. Like the previous month, we are constructive on the leading digital assets BTC and ETH and cautious regarding alternative layer 1 platforms, DeFi, and metaverse tokens.

Considering last month’s performance, this positioning did not produce the expected performance. Still, we believe it was a unique occurrence as these are the critical assets that act as collateral in lending protocols and last month’s massive liquidations caused unwanted returns. We have deployed additional cash to better equip ourselves for any opportunities that may present themselves in the coming month.

Bitcoin

Bitcoin price dropped by 35% in the last 30 days, more than most other cryptocurrencies except for ETH and AAVE. The price-performance can be attributed to liquidations of massive collateral used by multiple CeFi entities and high selling pressure caused by reduced miner revenue.

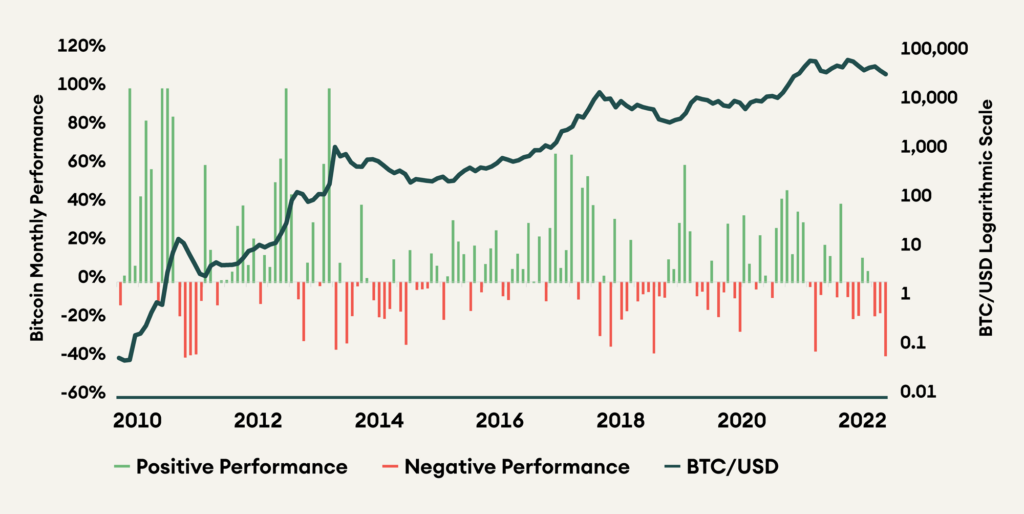

June 2022 was the worst performance month for Bitcoin in more than a decade. The last time BTC witnessed a similar performance was in 2011. With concerns of rising inflation figures, and a potential recession in the coming months, on-chain activity for the Bitcoin network has slowed, and there is an increase in accumulation trend score, indicating that long-term holders are gradually increasing their portfolio size.

Figure 1: Monthly performance of Bitcoin since 2010

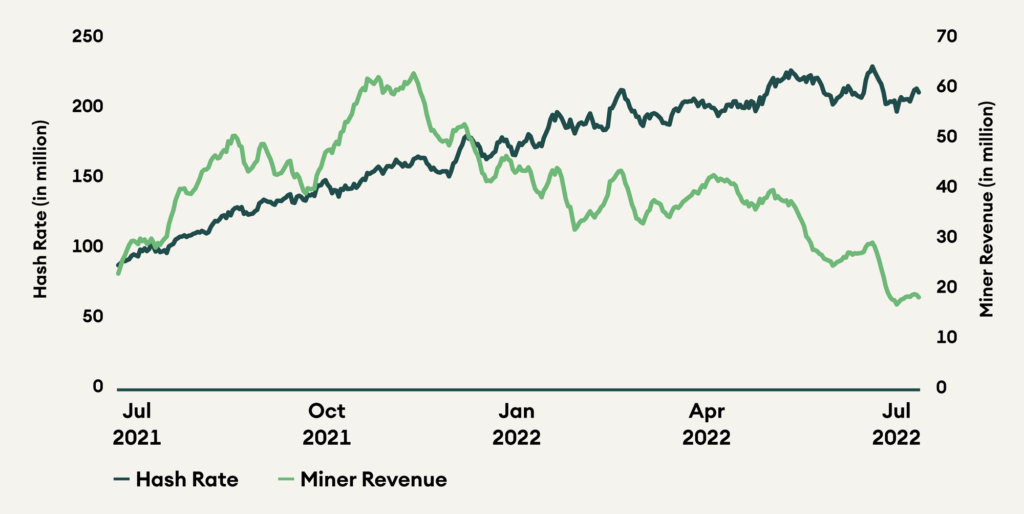

After China banned crypto mining, the Bitcoin hash rate recovered vigorously in the second half of 2021, to reach an all-time high in June 2022. The higher the hash rate, the more difficult it is to mine a block and get rewards. In other words, the cost of mining has increased while the price of bitcoin started falling in November 2021, leading to a decline in miners’ profitability. The recent fall in the hash rate indicates that the decrease in miner profitability has caused miners to disconnect some of their newly added capacity.

Further, publicly listed Bitcoin mining companies act as a proxy for investors who do not want to hold the asset directly but still want to gain exposure. Leveraging this philosophy, these mining companies started to accumulate Bitcoin that they generated through block rewards and transaction fees, increasing their reserves and hence investor confidence. They paid for mining operations through capital raised by offering equity or taking on company debt. But the recent decrease in miner revenue has caused some of these entities to sell their Bitcoin to cover costs. Sometimes, they sold more coins than they generated in a month. We discussed this in more detail in one of our Crypto Market Monitors last month; read it here.

Figure 2: Bitcoin hash rate and miner revenue for the last year

Ethereum

Ethereum has been going through a tough time in terms of price performance, and it is down 71% this year and 40% in the last month alone. The current fiasco of CeFi lenders laying off employees and restricting access to user funds started with an Ethereum synthetic asset called stETH.

As the Ethereum blockchain is moving to a proof-of-stake (PoS) consensus mechanism, validators required to keep the network secured must deposit 32 ETH to qualify as a validator. But these assets, once deposited, are locked in for more than a year or until after the Merge is successful. To provide liquidity for users who want to stake their ETH to secure the network but also want liquidity, Lido Finance had (LDO) the solution. In exchange for one ETH, one stETH was issued, which is a synthetic asset that accrues staking yield and can be redeemed for equivalent amount of ETH after the Merge. But as the value of one stETH started detaching from one ETH, the panic was set in the market, and users rushed to swap their stETH for ETH, creating a liquidity crisis for entities with massive exposure to stETH, like Celsius. Read more about this in one of last month’s Crypto Market Monitor.

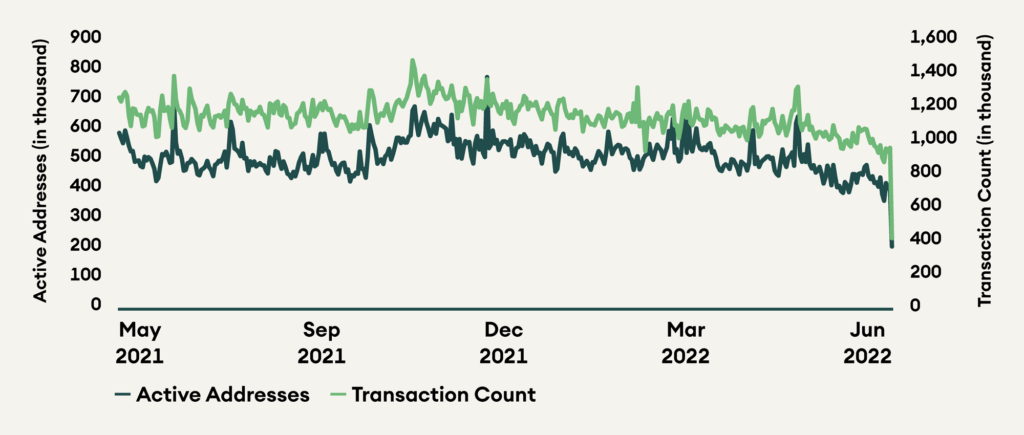

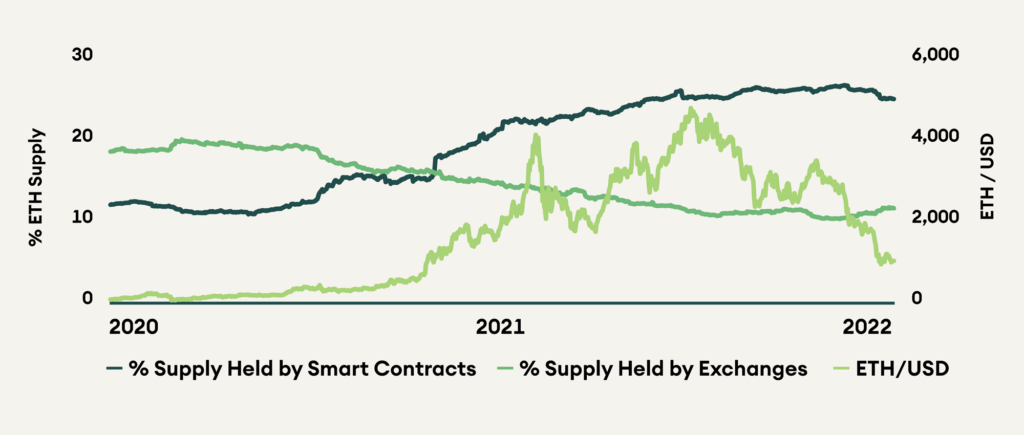

Figure 3: Ethereum transaction count and active addresses

These events reduced investor confidence in stETH and ETH for the short term, and Ethereum active addresses and transaction count kept decreasing. It touched very low levels not seen in more than a year (figure 3). The uncertainty around holding ETH is also caused by the highly expected Merge of the Beacon chain, completing the transition of Ethereum, and thus ushering in a new era. However, concerns regarding efficient scaling of Ethereum are increasing as one of the critical protocols dYdX recently decided to part ways with Ethereum and chose to build its own chain in the Cosmos ecosystem.

Further, the supply of Ethereum on smart contracts has reduced as the investor confidence in the decentralised finance (DeFi) ecosystem has been shaken, given the fall of Terra Luna (LUNA) and its stablecoin (UST), reduced activity on the network, drop in Total Value Locked (TVL) and many such reasons. Subsequently, the supply of ETH on exchanges has increased, indicating sell pressure.

Figure 4: Supply of Ethereum (ETH) on smart contracts vs. on exchanges

Alternative Blockchains

All the alternative blockchain assets we cover have performed better than the leading assets, Bitcoin (BTC) and Ethereum (ETH), but recorded negative performance. The smart contract platform Avalanche (AVAX) declined by 32%, followed by a 27% correction for the interoperability ecosystem Polkadot (DOT) and 24% for Stellar (XLM).

Litecoin (LTC) implemented one of the most anticipated upgrades to its network called MimbleWimble, a couple of months ago. It enhances the privacy of the transactions while reducing the data required to send transactions and thus enhancing the scalability of the network. But several centralised exchanges have delisted Litecoin, citing Anti-Money Laundering (AML) and Know Your Customer (KYC) laws.

Avalanche (AVAX) launched Bitcoin bridge through their browser extension web3 wallet, called Core. It enables native Bitcoin support on the Avalanche ecosystem, allowing Bitcoin holders to directly access extensive earning and yield opportunities on DeFi applications. Important to note that this native Bitcoin support is only available through Core browser extension and is not yet supported by Metamask or any other wallet.

Solana (SOL) blockchain continues to gain new users despite facing the massive challenge of multiple network outages in the past. Solana has the second biggest NFT ecosystem after Ethereum. Their leading NFT marketplace, Magic Eden, raised USD 130 million last month at a valuation of USD 1.6 billion, with plans to expand across multiple blockchains. Solana announced their new smartphone device and platform to bring blockchain applications natively to the device. It is expected to be available in second half of 2023.

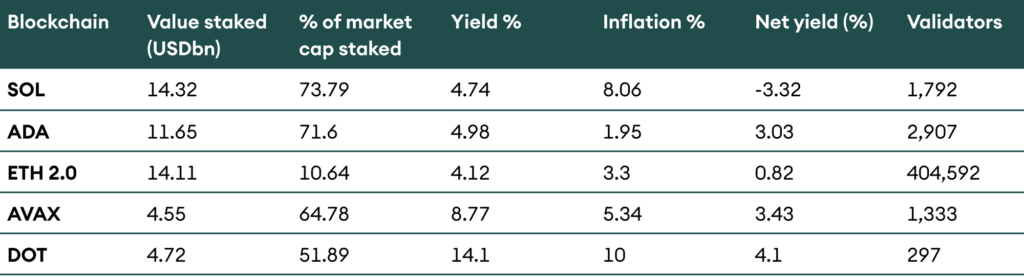

Table 2: Staking comparison of leading proof-of-stake platform blockchains (as of 26 June 2022)

Table 2 shows the comparison between different proof-of-stake blockchains. Solana has the highest percentage of market cap staked, followed by Cardano (ADA) and Avalanche. While Ethereum has the most significant number of validators even before it is transitioned to PoS. Polkadot offers the best yield, followed by Avalanche.

Decentralised Finance (DeFi)

Among the decentralised finance assets we cover, AAVE has performed the worst for the month, generating a negative return of 46%, followed by YFI, down by 23%, and LINK by 16%.

Following the incident of Celsius halting all user activities, MakerDAO voted to cut off lending platform Aave’s ability to generate DAI against derivative token stETH because 50% of the DAI borrowed on Aave was by Celsius and collateralised by stETH. This indicates the risk to DeFi apps as well, created by the current insufficient risk management practices of select CeFi entities. Further, Aave continues to build its social media protocol called Lens protocol with a community-centric approach.

Synthetix (SNX) recorded over USD 200 million in trading volumes on 20 June as its atomic swap product gained traction among traders. This was a significant increase compared to the average daily volume of USD 500k to USD 3 million. Synthetic ether (sETH) and synthetic dollar (sUSD) were the most active trading pair during this time. The token SNX was up more than 100% during the same day but has since corrected and is down 3% on a 30-day basis.

Uniswap (UNI) is down only 4% for the month, as it overtook Ethereum in the amount of gas fees paid. Further, Uniswap acquired NFT aggregator platform Genie to integrate NFT trading along with ERC-20 trading. Uniswap will also be doing an airdrop to anyone who has used genie before 15 April 2022, and its snapshot has already been taken.

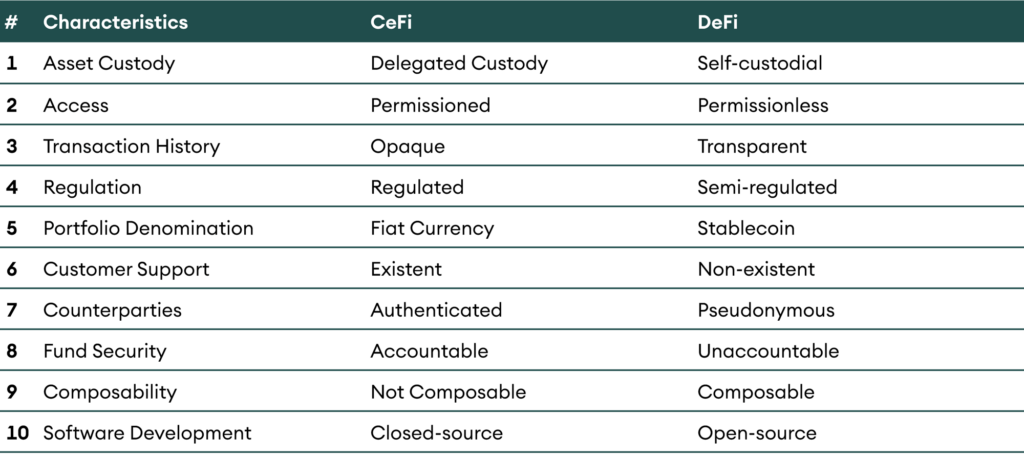

In the wake of the liquidity crisis felt by the entire crypto ecosystem over the last couple of months, it’s essential to understand the critical differences between centralised and decentralised finance platforms. The following table highlights several essential characteristics.

Table 3: Difference between CeFi and DeFi platforms

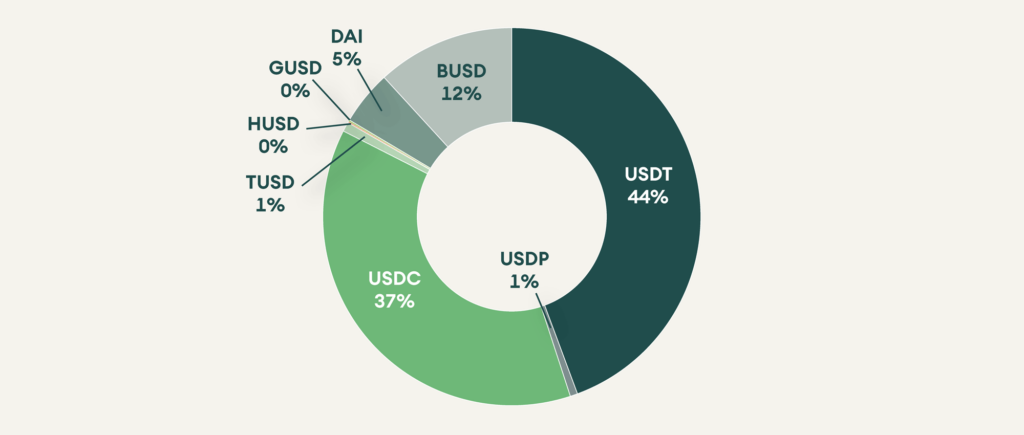

Since stablecoins are the backbone of the crypto economy now, the following is the market share distribution among different US dollar stablecoins operating in the market. USDC has become more popular over the last year, gaining market share from USDT.

Figure 5: Market share of USD stablecoins

Conclusion

The full extent of the current liquidity crisis is not entirely behind us, given that we are still witnessing multiple centralised platforms halting user withdrawals, laying off employees, and raising money for survival. Thus, it is safe to say that the negative sentiment prevails in the market, making it difficult to predict the direction in the short term. The uncertain geopolitical scenario continues to dominate the overall financial ecosystem, increasing the risk of further high inflation, slow growth, and a recession.

As mentioned at the beginning of this article, we continue to be cautious in our approach. We have nonetheless reduced our cash position to deploy capital as valuation is attractive. We are still constructive on leading assets, BTC and ETH, and are cautious on alternative platform coins, decentralised finance or metaverse tokens.

It’s important to note that even though the current market pain started with the fall of Terra Luna, a DeFi protocol, most of the liquidity crisis is being felt by centralised finance entities, mainly because of their non-efficient risk management practices. Most DeFi protocols are working as expected.