AMINA Bank AG

AMINA Bank AG  AMINA UK

AMINA UK  AMINA Hong Kong

AMINA Hong Kong  AMINA EU

AMINA EU Introduction

The month of October lived up to expectations, maintaining its “Up-tober” reputation. The total cryptocurrency market capitalisation increased over the month, ending 23% higher. In the ever-evolving landscape of cryptocurrencies, recent developments have sparked both enthusiasm and curiosity among investors and enthusiasts. Bitcoin’s notable price surge, briefly surpassing the USD 35K mark, has reignited discussions, primarily fueled by speculations about the potential approval of a Bitcoin exchange-traded fund (ETF). Meanwhile, in addition to ETF rumours, Ethereum’s eagerly anticipated upgrade, Dencun, promises to reshape its ecosystem by improving scalability.

In this edition of the Digital Investor, we delve into these topics and the perplexing performance dynamics between the relative price performances of Ethereum and Bitcoin throughout 2023. The article also explores factors that could be contributing to Tether’s enduring market dominance, as well as the shifting landscape for Circle’s USDC. The spotlight then turns to Solana, with a closer look at the driving forces behind its impressive resurgence in the recent few months. Beyond these narratives, we also navigate the intricacies of the layer-2 (L2) and decentralised finance (DeFi) markets and provide insights into Bitcoin’s onchain metrics, offering a comprehensive view of the multifaceted cryptocurrency landscape.

Macroeconomy

In recent macroeconomic developments, the US Federal Reserve has opted to maintain its benchmark interest rates at the range of 5.25% to 5.50%, potentially signalling that the rate hike cycle is behind us. Concurrently, China’s highest legislative body has granted approval for a substantial sovereign bond issuance, amounting to USD 137 billion, aimed at bolstering the nation’s economic resilience.

The rise in crude oil price to a 10-month high can be attributed to the concerted reduction in production by key players such as Saudi Arabia and Russia, coupled with a surge in demand for gasoline and aviation fuel in the wake of China’s economic resurgence. According to assessments by JP Morgan, the spare capacity among non-OPEC oil suppliers is dwindling, thereby introducing an associated risk premium. Recent geopolitical events, notably the ongoing conflict in the Middle East, have demonstrated the capacity of such risks to rapidly impact oil prices, despite an absence of immediate supply disruptions. As we look ahead, the energy sector could be poised to outperform broader equity markets, serving as a strategic hedge against the backdrop of rising inflation, interest rates, and geopolitical uncertainties.

In the realm of cryptocurrencies, Bitcoin’s weekly correlation with the NASDAQ index has reached its lowest point since August 2021, while its correlation with gold has jumped to its highest level since the banking crisis earlier this year.

Bitcoin

Bitcoin recently experienced a noteworthy price surge, briefly crossing the USD 35K threshold, a level not seen since May 2022. This surge was predominantly driven by mounting speculation surrounding the potential approval of a spot Bitcoin exchange-traded fund (ETF) by the U.S. Securities and Exchange Commission (SEC). Subsequently, the price retraced slightly, and at the time of writing, Bitcoin (BTC) is trading around USD 34.4K.

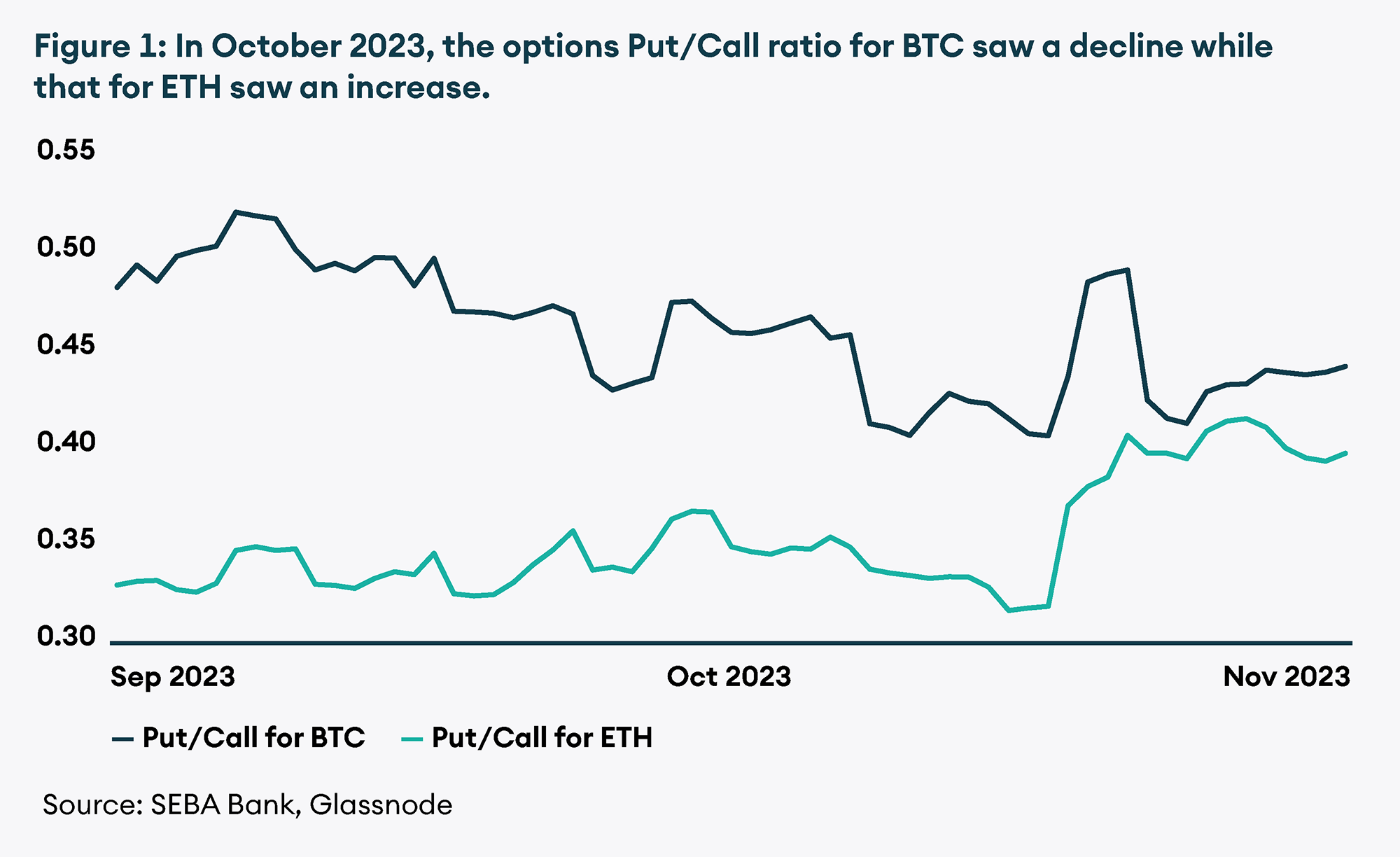

Amidst the buzz of ETF prospects, the open interest in CME Bitcoin futures surpassed 100K BTC for the first time on 24 October. The market share of CME Bitcoin derivative contracts concurrently reached an all-time high of 25%, rapidly approaching the 29% market share held by Binance. As open interest expanded, the 1-month annualised futures premium for BTC surged to 13%, notably higher than that of Ethereum (ETH). This upswing suggests the potential entry of traditional financial players into the Bitcoin market, possibly in anticipation of an imminent Bitcoin ETF approval. According to Glassnode data, the open interest-weighted mean Bitcoin futures perpetual funding rate across exchanges stands at 0.012% with traders paying the rate to hold their long positions on BTC. The 30-day average total futures open interest for BTC increased by over 44.9% in the month of October to reach USD 25.36 billion at the time of writing, while total options open interest is at USD 12.23 billion. The put/call ratio decreased from 0.48 to 0.43, indicating a significant shift in sentiment towards the positive side.

Shifting the focus to onchain metrics, the 10-year illiquid supply of Bitcoin has surpassed the amount held on exchanges. This is traditionally interpreted as an indicator of an impending bull market, signifying that a greater portion of Bitcoin is in the hands of long-term holders rather than being readily available on exchanges. Such a dynamic tends to drive up the asset’s price, as the available liquid supply may struggle to meet the rising demand. In addition, Bitcoin’s price surge in October has notably boosted mining profitability, with nearly a 20% month-over-month increase. With a positive outlook on the horizon, the value proposition of mining Bitcoin becomes increasingly apparent, allowing miners to accumulate Bitcoin at a lower production cost compared to purchasing it on the spot market.

Ethereum

Beyond the discussions surrounding ETF applications, the Ethereum ecosystem has been abuzz with anticipation for its forthcoming upgrade – Dencun. This upgrade has been eagerly awaited due to its objective of transforming Ethereum into a scalable settlement layer, promising faster transaction speeds and reduced fees. However, it was recently confirmed by Ethereum client developers that the Dencun upgrade will not be deployed through a network hard fork in 2023. Over the past two weeks, Ethereum has witnessed a remarkable 170% surge in transaction fees, and this figure could rise further if blockchain activity continues to escalate in response to positive ETF news. Consequently, the delay in the Dencun upgrade could subject Ethereum to network congestion amid the surge in blockchain activity. This would also lead to more ETH burn from base fees as this activity continues to rise, eventually pushing the price of ether upwards due to a reduction in supply.

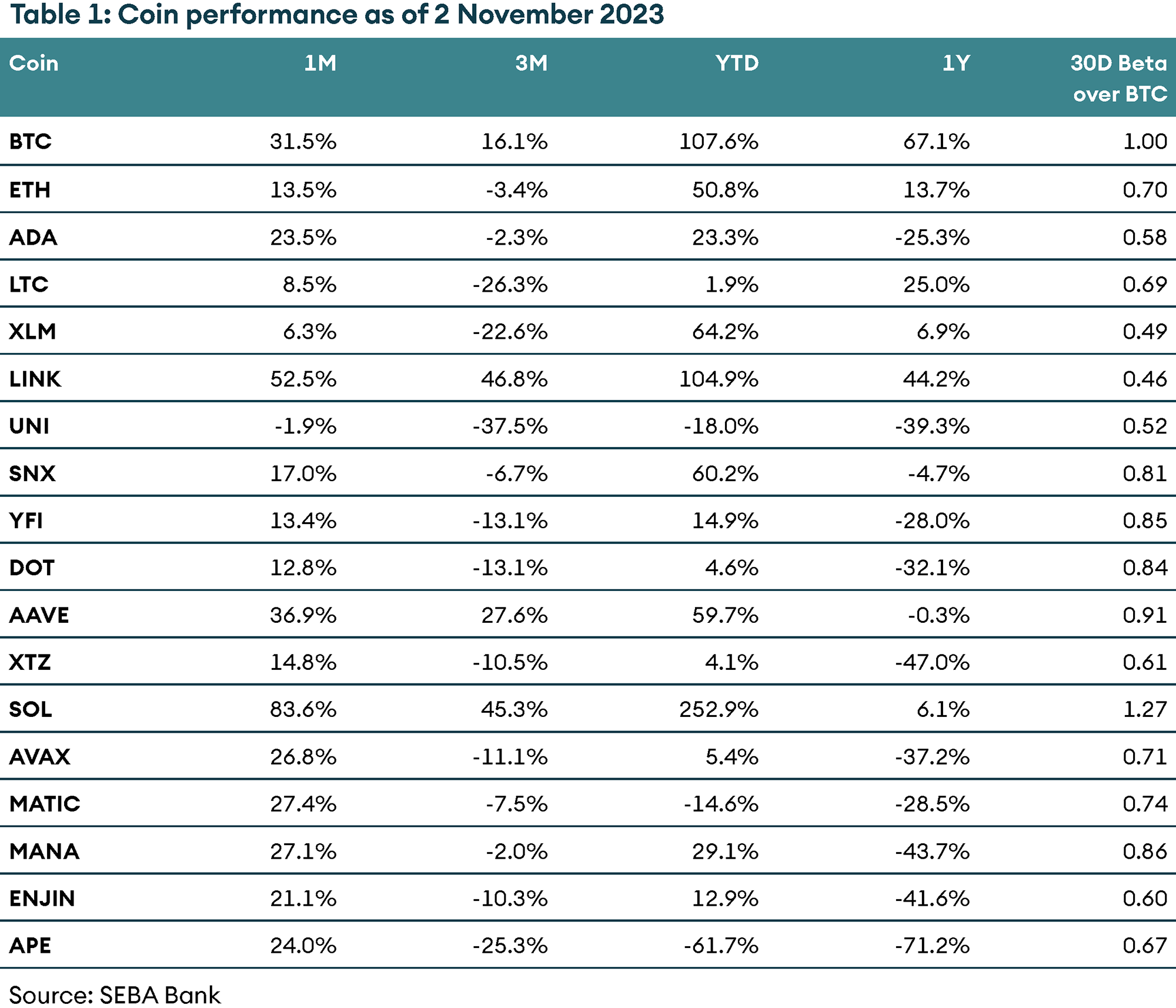

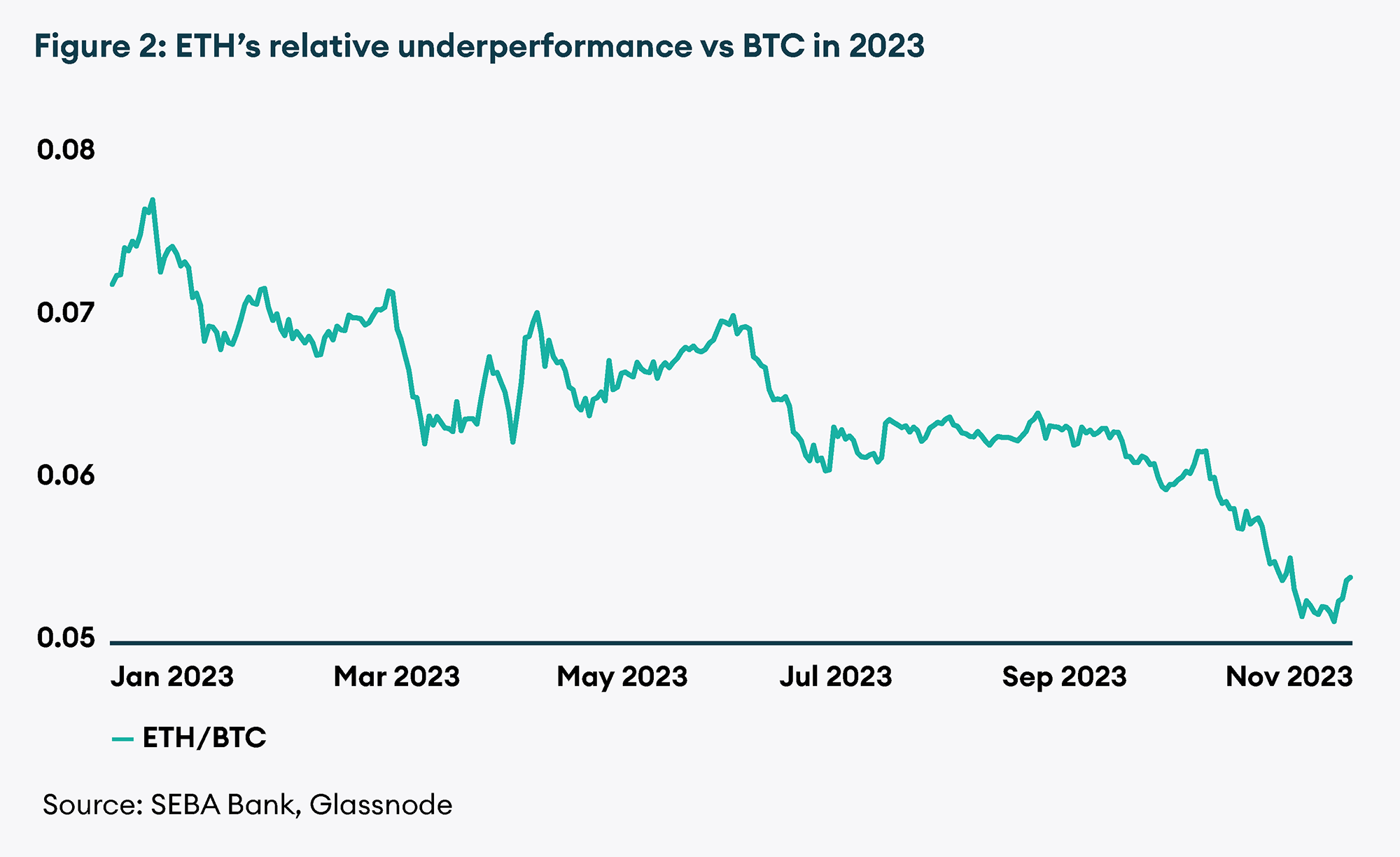

Reflecting on Ethereum’s performance in 2023, one may wonder why it significantly underperformed Bitcoin (BTC) this year. For context, Ethereum’s year-to-date returns are just over 58%, whereas Bitcoin’s have reached 110% at the time of this writing. The ETH/BTC ratio has declined by roughly 30% year-to-date. While this performance differential lacks a definitive explanation, several factors may have played a role.

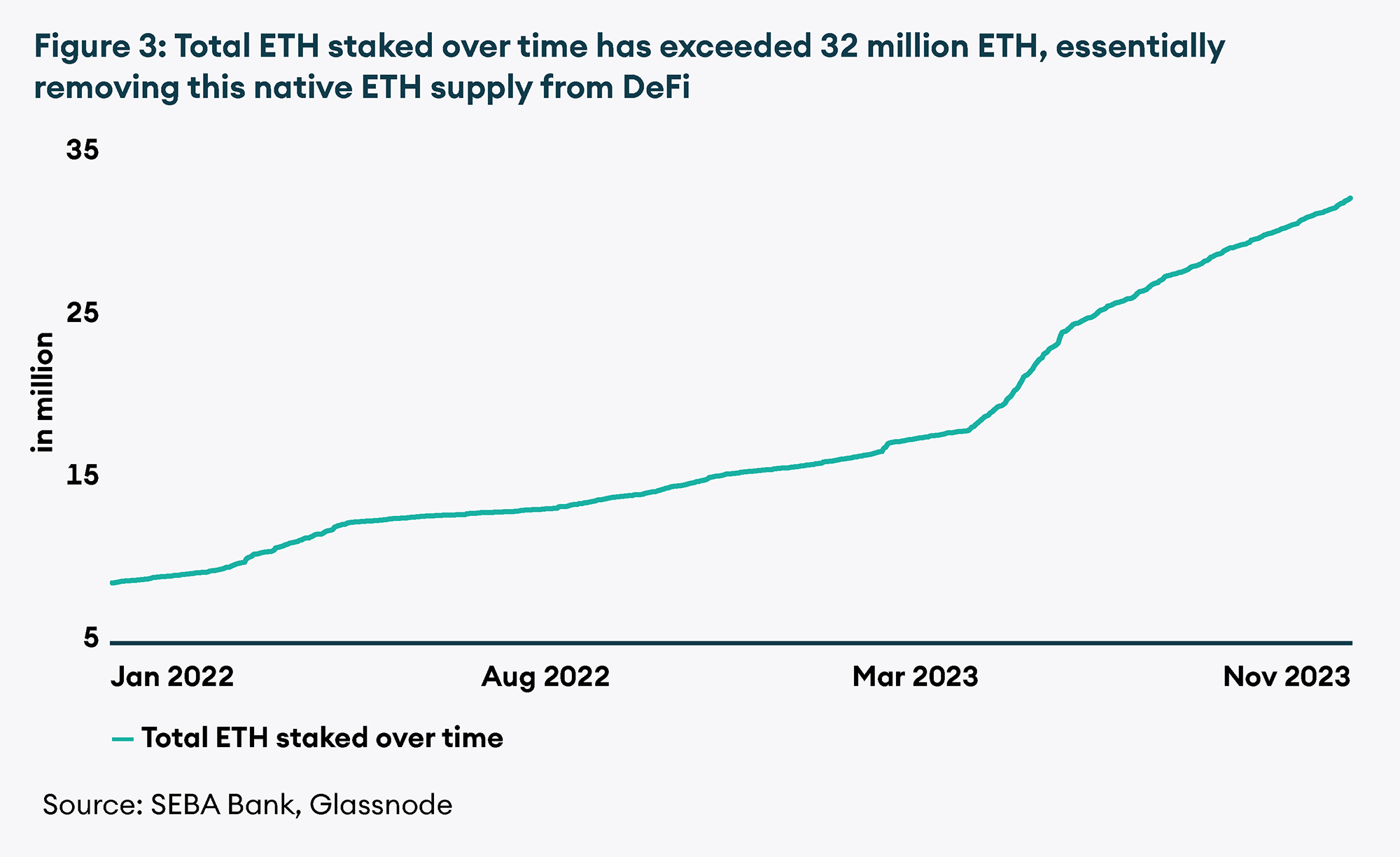

Firstly, ETH staking gained substantial momentum shortly after the Shapella upgrade earlier this year in April. The total value staked on Ethereum has surged to over 32 million ETH, marking a 78% increase since Shapella’s implementation. While this level of staking creates a robust price floor for the asset, this locked ETH supply is not actively participating in native DeFi activities, effectively slowing down the broader DeFi market, except for liquid staking solutions.

Furthermore, the NFT market has shown relatively limited demand, with the Total Value Locked (TVL) on NFT marketplaces and lending protocols, as reported by DeFi Llama, amounting to less than USD 300 million out of the total USD 43 billion in DeFi TVL at the time of writing. Due to this lack of activity on DeFi and in NFTs, the utility demand for ETH as a gas token dropped drastically. Perhaps the most influential factor appears to be the ascendancy of Ethereum layer-2 solutions (L2s). According to L2 Beat, TVL on L2s has soared by over 180%, increasing from USD 4.4 billion in January to approximately USD 12.7 billion at the time of writing. L2s offer significantly faster transactions at a fraction of the cost, prompting users to migrate from the Ethereum Mainnet to L2s. Worth noting is the implementation of EIP1559, which introduced (in August 2021) a burn mechanism for the base fee in ETH, potentially rendering ETH deflationary in the long run. Given that L2 fees are substantially lower than on the Mainnet, the leap in L2 adoption has resulted in a reduced burn of ETH and an effect more akin to disinflation than deflation, with ETH’s current inflation rate standing at 1.159%.

In the realm of derivatives, Ethereum’s metrics portray a somewhat less favorable short-term picture compared to Bitcoin. According to Glassnode, the open interest-weighted mean Ethereum futures perpetual funding rate across exchanges is at 0.008%, with traders bearing this cost to maintain their long positions in ETH. Ethereum’s 30-day average total futures open interest increased by 11.7% in October, reaching USD 5.098 billion at the time of writing, while total options open interest stands at USD 6.28 billion. The put/call ratio has shifted from 0.34 to 0.36, indicating a slight shift in sentiment.

Layer-2 Developments

The Ethereum layer 2 ecosystem has seen significant developments in October, with Arbitrum launching its mainnet for Orbit. Orbit allows developers to create their own layer-3 blockchains by permitting the execution of transactions on an external blockchain and settlement on Arbitrum. This move aligns with a broader trend among Ethereum layer-2 network developers, such as OP Labs (behind Optimism), Polygon, and Matter Labs (zkSync), who are opening their technologies for builders to replicate or modify according to their specific needs. Additionally, the Arbitrum Foundation has partnered with Celestia, a modular solution, to provide data availability for Orbit. Applications built on Orbit will have the option to publish their data to Celestia once the solution goes live.

Polygon Labs, a leader in Ethereum’s scaling space, has unveiled the POL token upgrade on Ethereum mainnet, marking a pivotal milestone in its Polygon 2.0 roadmap. The POL token now takes over as the primary currency within Polygon’s extensive ecosystem, which encompasses the primary Polygon POS blockchain, the Polygon zkEVM network, and various supernets. This transition began in September, coinciding with the release of three Polygon Improvement Proposals (PIPs). PIP-18, in particular, aims to establish a network of interconnected zero knowledge-powered L2 chains with the potential to scale Ethereum to the dimensions of the entire Internet.

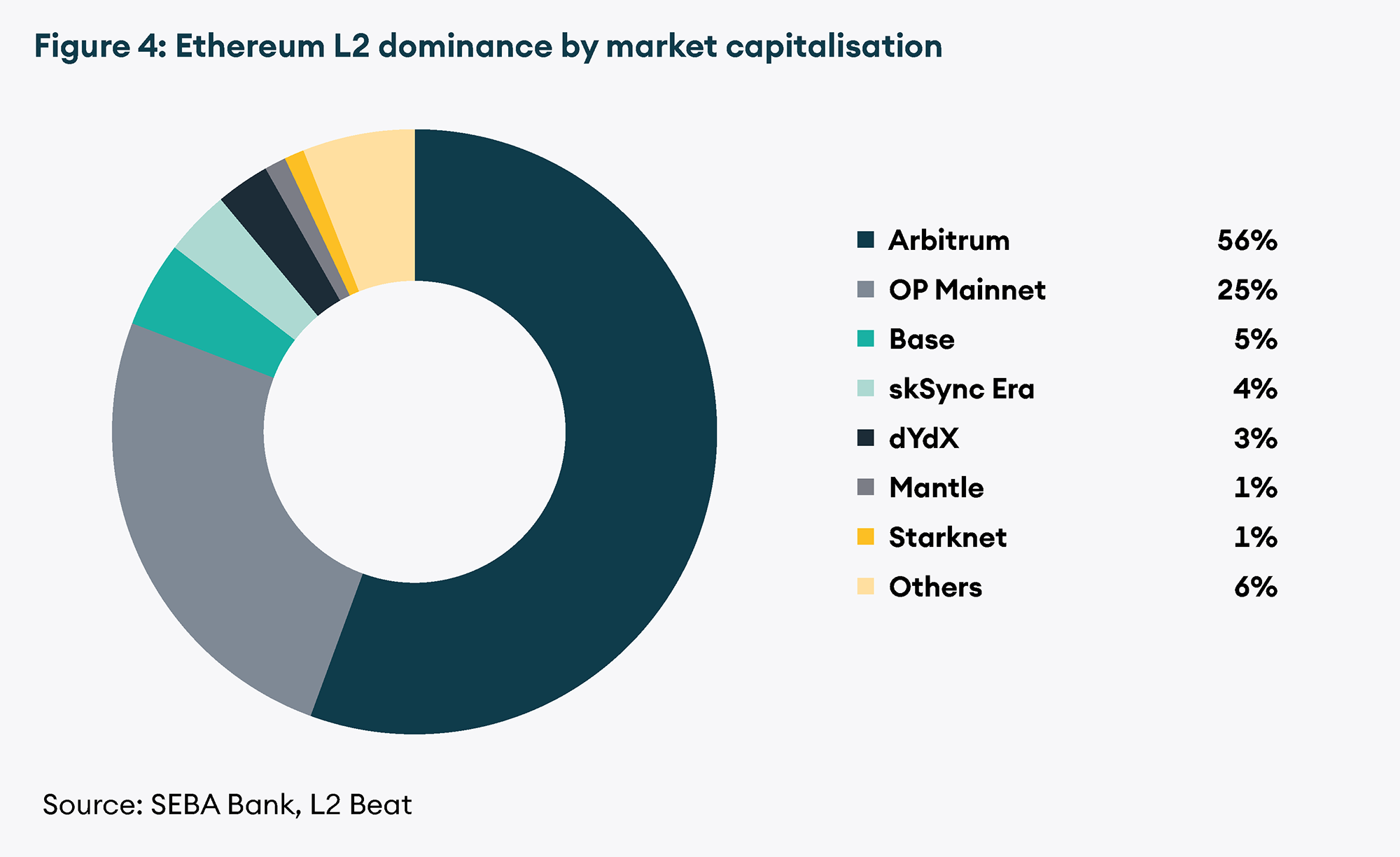

According to L2 Beat, Arbitrum maintains a substantial dominance in layer-2 TVL, commanding a 55% market share. OP Mainnet follows with a 25% share, and Coinbase’s Base rollup, built on the OP stack, holds a 4.5% share. For those interested in tracking the crypto Layer 2 market, this Flipside dashboard provides valuable insights and data.

Decentralised Finance (DeFi)

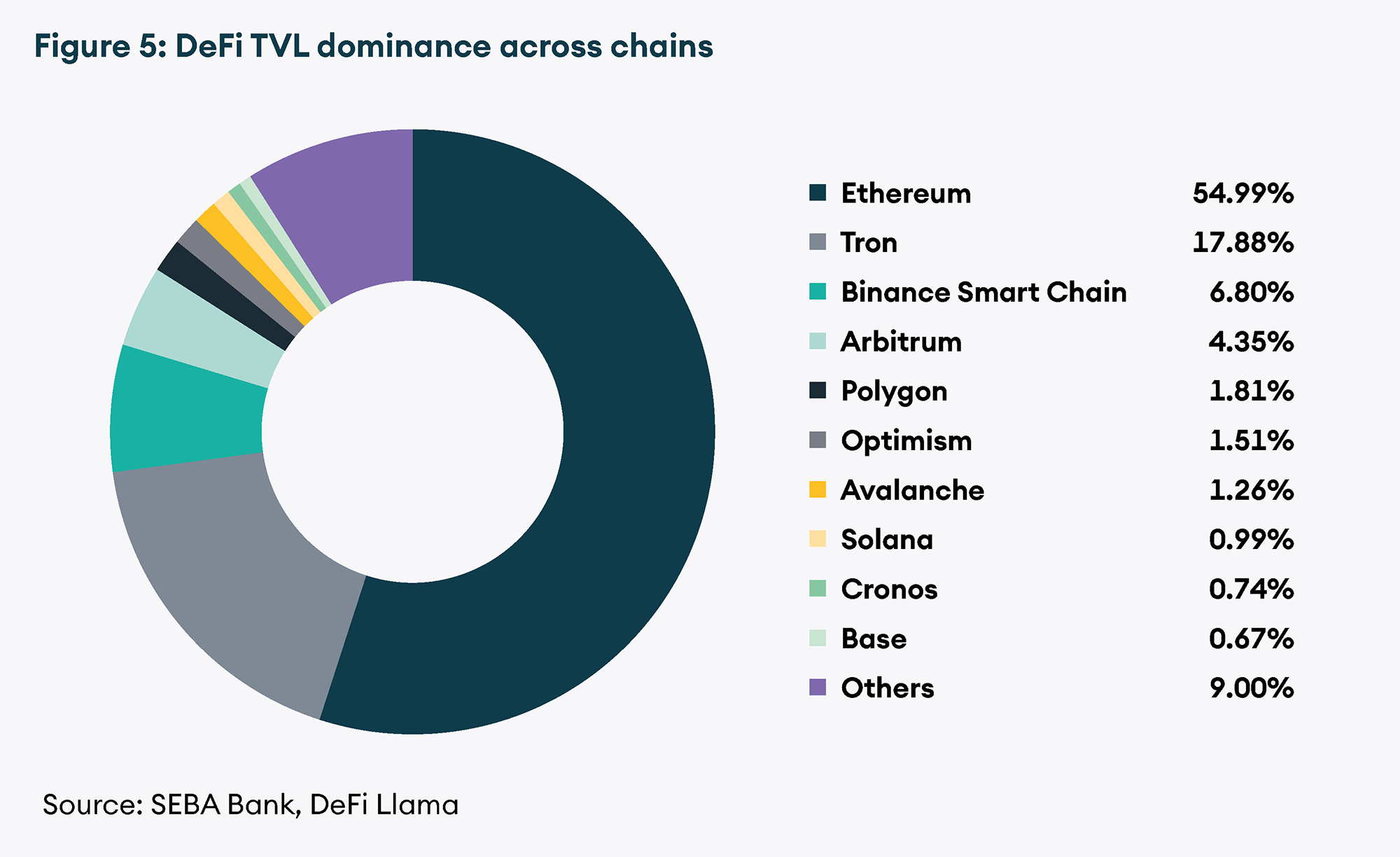

The DeFi landscape witnessed a substantial surge in total value locked (TVL) in October, climbing by nearly 30% from USD 38.16 billion to its current level of USD 43.69 billion. Leading the pack is Ethereum with a TVL of USD 23.88 billion, followed by Tron in the second position. Notably, Cardano recorded an impressive 42% TVL increase, while Solana saw a 35% rise over the one-month period. Cardano’s TVL boost can be attributed to activity on lending protocols such as Indigo, Lenfi, Optim Finance, and decentralised exchanges like Minswap and Muesli Swap, catalysed by a demand for stablecoins, driven in part by the COTI-developed Djed protocol. Solana’s TVL growth was bolstered by liquid staking solutions like Marinade Finance and Jito.

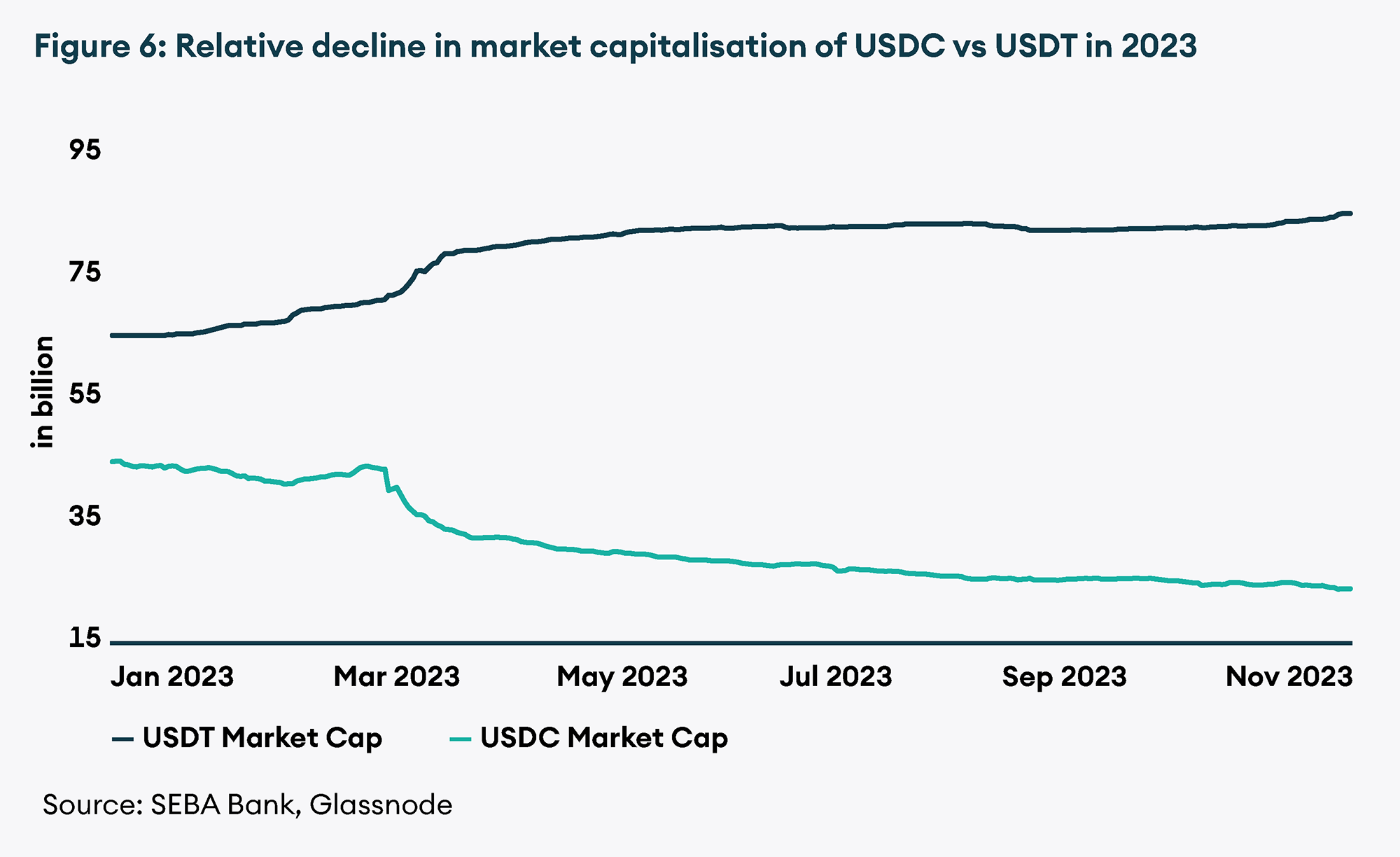

In the broader cryptocurrency stablecoin market, the total market capitalisation remained relatively stable, hovering around the USD 124 billion mark throughout the month. Ethereum retained its position as the highest stablecoin market capitalisation platform, with USD 65.13 billion, followed by Tron at USD 46.37 billion.

Tether (USDT) continued to maintain a dominant market capitalisation, accounting for over 68% at USD 85.4 billion. The race to be the top stablecoin has been primarily contested between Tether’s USDT and Circle’s USD Coin (USDC). However, the market capitalisation of USDC offering has dipped. A key contributing factor is the migration of USDC holders from stablecoins to high-yielding US Treasury bonds following the Federal Reserve’s interest rate hikes. In contrast, Tether’s popularity in Asia has propelled its market cap to over three and a half times that of USDC. In their recent attestation, Tether has reported USD 3.2 billion in excess reserves backing the value of its stablecoins. Out of its total reserves, USD 72.6 billion is exposed to U.S. Treasuries, including direct T-bill investments, repurchase agreements, and deposits in money market funds. The Tether team also plans to introduce a real-time reserve reporting system in 2024 to enhance transparency and address concerns within the crypto community regarding USDT backing. In contrast, USDC issuer Circle has announced discontinuation of support for consumer Circle Mint accounts and the phased-out support for legacy consumer accounts, meaning users who wish to mint Circle stablecoins will need to explore other platforms like Coinbase. Meanwhile, Tether continues to support individual consumer accounts with a minimum limit of USD 100K.

Spotlight on Solana

Solana’s remarkable performance and the resurgence of its native SOL token in recent months have garnered substantial attention in the crypto space. While it did experience a slight retreat in the past week, Solana nearly doubled in value over the preceding weeks.

One of the driving factors behind Solana’s success has been the substantial capital inflow into staking protocols within the Solana ecosystem. Notably, Lido Finance’s decision to cease SOL staking for new users created an opportunity for other staking protocols like Marinade Finance, Jito, and JPool, resulting in remarkable one-month Total Value Locked (TVL) surges of 176%, 299%, and 155%, respectively. This surge in staking activities has further spilled over into the DeFi lending space, with protocols like Solend and MarginFi experiencing robust user engagement.

An upgrade to the Solana network has contributed to its growing decentralisation by reducing validator hardware requirements and introducing confidential transactions using zero-knowledge (ZK) technology. The recent testnet launch of Firedancer, developed by Web3 firm Jump Crypto and announced by the Solana Foundation at the Breakpoint conference on October 31, represents an important step in enhancing the network’s validator infrastructure. Firedancer is set to become a new validator client for Solana, with its mainnet launch scheduled for the first half of 2024. Additionally, Solana has maintained a consistent liveness record over the last two-thirds of a year, providing a robust foundation for potential growth.

Solana’s exceptional resurgence, with SOL surging over 300% this year, has captured the attention of crypto market participants. This remarkable comeback is all the more striking considering that the SOL token was among the hardest-hit assets during the bear market, particularly after the collapse of Sam Bankman-Fried’s FTX exchange. The renewed interest from institutions and significant inflows from large investment funds have played a pivotal role in supporting the token’s price recovery. According to CoinShares, crypto funds holding SOL have seen inflows of nearly USD 100 million this year, making it the second-largest amount after Bitcoin (BTC).

SBF convicted on all counts

October also saw the conviction of Sam Bankman-Fried, the founder of the now defunct FTX crypto exchange and trading firm Alameda Research. SBF has been found guilty on all seven criminal counts levied against him and now faces a potential maximum prison sentence of 115 years.

Conclusion

From the Fed halting interest rate hikes to the ETF-approval rumours, Bitcoin’s dominant price performance throughout 2023, the growing adoption of Ethereum layer-2s and the macroeconomic backdrop all seem to be lining up perfectly for Bitcoin’s upcoming halving in 2024. Historically, Bitcoin’s halvings have been bullish catalysts. The conviction of SBF also signals a pivotal moment for crypto – of the market putting its past behind and looking ahead in anticipation of the ushering of a new phase. In addition, Solana’s remarkable resurgence from a bear market underscores the crypto space’s dynamism, while the ongoing battle between stablecoin giants Tether and Circle provides an engrossing narrative to watch. Looking ahead, promising opportunities beckon, with the horizon holding promise for those who adeptly navigate this ever-shifting terrain.