AMINA Bank AG

AMINA Bank AG  AMINA UK

AMINA UK  AMINA Hong Kong

AMINA Hong Kong  AMINA EU

AMINA EU Abstract

In this special edition of the Digital Investor, we update our bitcoin fair-value estimate. As institutional investors choose to hold bitcoin through custody solutions, one address cannot be considered as one user. Due to institutional investors’ growth in bitcoin, the user network’s size is not accurately measured with the number of addresses any more. A network of 50mio users seems plausible, implying a bitcoin fair-value of USD 50,000.

We also update our mining parity model. It shows that mining activities have moved in line with prices. We also show that mining activities for ETH and ETC decoupled from their prices when Ethereum 2.0 was launched on 1 December 2020.

Introduction

In July 2020, we published “A new fair-value model for bitcoin” in which we estimated a fair value of USD 10,670 when bitcoin traded at USD 9,100. This time seems far away as bitcoin price reached an all-time high of USD 42,000 on the first days of 2021. Is this price surge pure speculation, or does it have a basis in the fundamentals?

According to our Bitcoin valuation model, institutional adoption has led to a sharp increase in its fair-value. While it is difficult to quantify the impact of institutional adoption, we think it can justify a bitcoin fair-value of USD 50,000.

Besides bitcoin fair-value, our mining parity model shows that cryptocurrency mining activities in BTC, BCH and BSV have moved hand in hand with the prices. We also show that mining activities for ETH and ETC decoupled from their prices when Ethereum 2.0 was launched on 1 December 2020.

Institutional adoption

Since the publication of our first fair-value estimate seven months ago, the crypto market has developed rather quickly. When we published our report, bitcoin had recovered from the COVID crash after it had halved in a matter of days. Critical voices called it the end of bitcoin as it did not fulfil its promise of a safe-haven asset (see Bitcoin is dead, long live Bitcoin and Bitcoin, gold, and coronavirus).

However, bitcoin survived its first global crisis and emerged stronger. Its price surged to USD 42,000 on the first day of this year. At the time of writing, it trades close to USD 32,000.

We think the price rise is mainly attributed to acceleration in institutional adoption in the second half of 2020. In October, PayPal announced account holders could buy, hold, and sell bitcoins. In the same month, Square announced that it had invested USD 50 million in bitcoin. In November, Stanley Druckenmiller made his bitcoin investment public; a few months after another hedge fund legend, Paul Tudor Jones announced that he has almost 2% of assets in bitcoin. Later in the year, Ruffer Investment did the same. In the meantime, Microstrategy bought more than 70,000 bitcoin last year, and Grayscale holds more than 600,000.

The rise in the number of addresses holding more than 1,000 bitcoins (figure 1) indicates institutional investors’ rise. Since October 2020, this number has rapidly increased by 11% to 2,444. These addresses hold more than 8mio bitcoins cumulatively.

While institutional adoption is welcome, it poses a severe problem for our model. We think the value of cryptocurrencies depends on the network’s size, meaning the number of users/holders. Our model uses the number of addresses as a proxy for the same. With the rise of institutional investors and custody solutions, using the same address for multiple users hides the real number of small investors and users behind them. Using the number of addresses as a proxy for the network size significantly underestimates the reality.

Model reminder

As a reminder, the model we have developed to estimate bitcoin’s fair value is articulated around four terms that capture the essence of native cryptocurrency value: network, immutability, monetary policy, and currency type. The first two terms embody the network effect by capturing demand for the blockspace. The last two characterise the currency design, i.e., the supply of a specific type of currency. Only a combination of a robust blockchain and a well-designed currency wrapped in an appropriate set of rules (tokenomics) has value.

Expressed as an equation, our model is as follows.

where P(t) is the dollar price of the cryptocurrency, C(t) the number of units of a cryptocurrency in circulation, and P(t)C(t) the market capitalisation.

The first term is the network value. U(t) is the number of users measured in terms of addresses, and n is the network parameter that captures the positive externalities associated with the users. The second term is immutability value. H(d,t) is the calibrated network hash rate and i the immutability parameter that measures network security. The third term describes the monetary policy. C(t)/C is an index measuring the proportion of circulating supply C(t) to total supply C, and s is the scarcity parameter. Finally, the fourth term describes the currency type. The ratio C(t)/T(t) measures the proportion of transaction T(t) to the current supply C(t), and g is the Gresham’s law parameter. (For a detailed description of the model, readers are invited to read the “A new fair-value model for bitcoin“.

Fair-Value

To estimate bitcoin’s fair value, we measure the number of users with the number of addresses holding at least 0.001 bitcoin. Currently, there are close to 17 million of these addresses, 1.1 million more than at the time of our first estimate. This increase does not accurately reflect the real growth in the number of bitcoin users by any metric.

When PayPal offered bitcoin trading to its users, it counted 346 million users. Approximately 20% of them have used this new feature to trade bitcoin according to an article by Coindesk. Given the small size of the survey, the error margin is elevated. Imagine that only 10% did it, this would increase the bitcoin network’s size by 34.6 million to 51.6 million instead of the current 17 million.

Ceteris paribus, the tripling of the network size from 17 million to 51.6 million multiplies our bitcoin fair-value by four to USD 51,300.

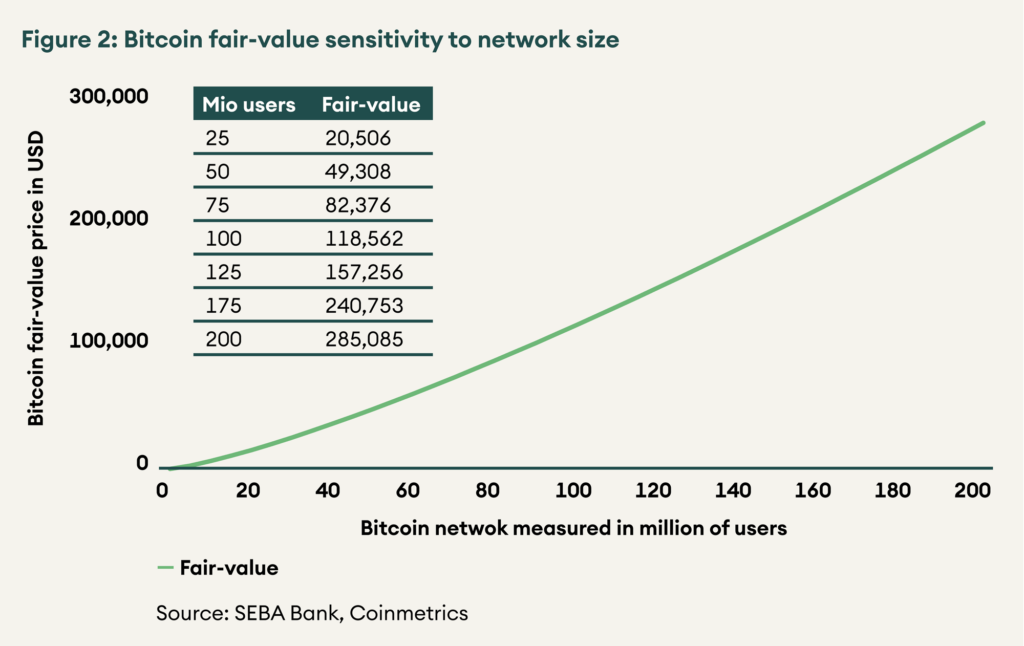

Figure 2 shows how bitcoin fair-value increases with the size of the network according to our model. We observe that network effects are non-linear, meaning the fair-value increases more rapidly than the increase in the network’s size, as illustrated in the table embedded in figure 2. For instance, a 50 million bitcoin network would lead to a BTC fair-value of USD 49,308 and a 100 million network to USD 118,562.

No one knows the Bitcoin network’s exact size, but everyone agrees that it is rapidly increasing. As we mentioned above, the arrival of PayPal and other institutions in the cryptospace has led to a massive increase in bitcoin users. All institutional investors provide convenient and user-friendly ways to enter the cryptospace and allow a myriad of smaller investors and users to hold bitcoin and other digital assets indirectly. As a result, a network of 50 million users seems plausible, making bitcoin’s fair-value approximately USD 50,000.

Besides the network, all the other variables of the model – immutability, monetary policy, and currency type – have continued to support the fair-value. Immutability, as measured by difficulty, has increased steadily. The monetary policy shows a predictable increase in scarcity as the current supply is growing by 6.25 bitcoin per block, currently standing at 18.6 million bitcoins out of a total of 21 million. Finally, the currency type variable indicates that bitcoin is increasingly perceived as “good money” as per Gresham’s law – the proportion of coins held in wallets relative to those used for transactions has increased.

Mining Parity

In the aforementioned Digital Investor edition, we also presented a second valuation model to answer a different question. Instead of estimating the dollar value of bitcoin, it estimates the fair value of bitcoin (BTC) vs bitcoin Satoshi Vision (BSV) and bitcoin cash (BCH). As these last two chains are forked from Bitcoin, they are similar in many respects, particularly for mining, and are thus easily comparable.

As mining any of these three cryptocurrencies is identical as the consensus algorithm is similar, miners should be indifferent mining any of them as long as the expected profit remains the same. This is the intuition behind the mining parity. A full description of the mining parity condition is described in the second part of A new fair-value model for bitcoin.

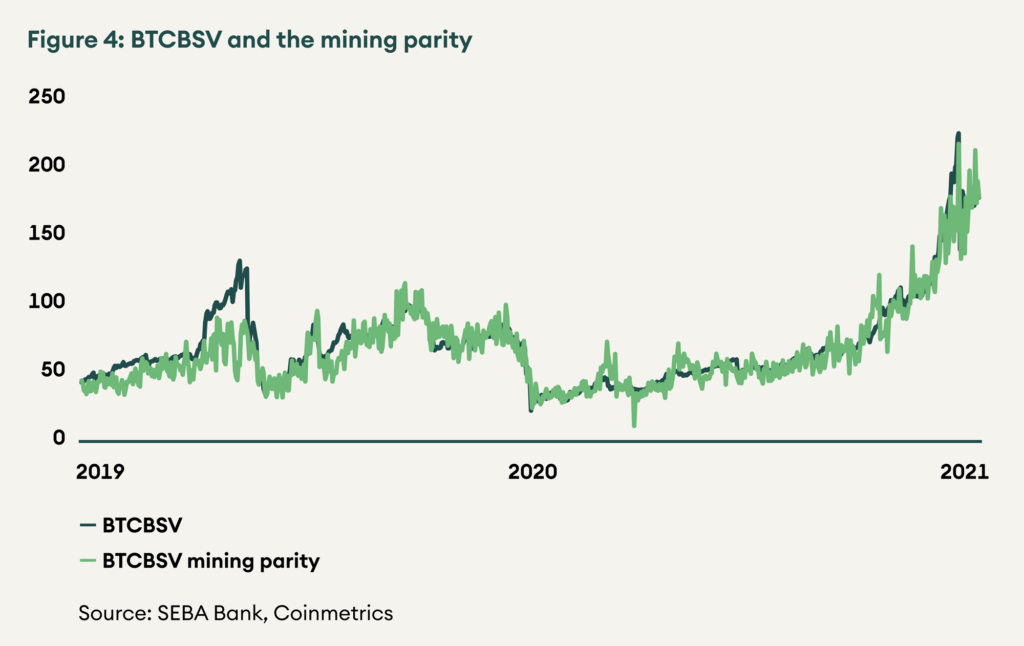

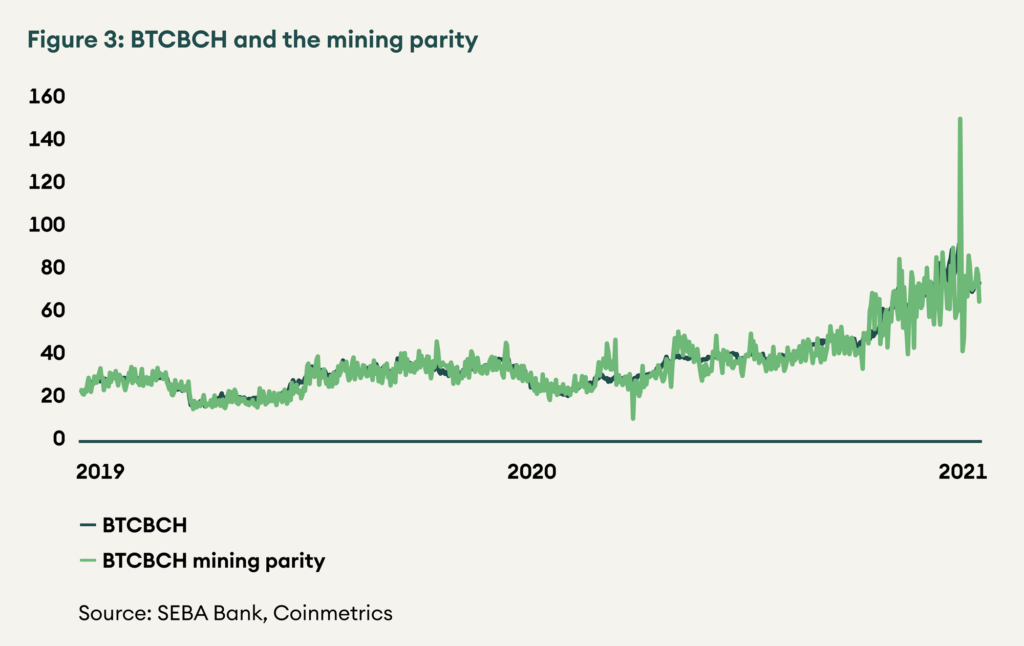

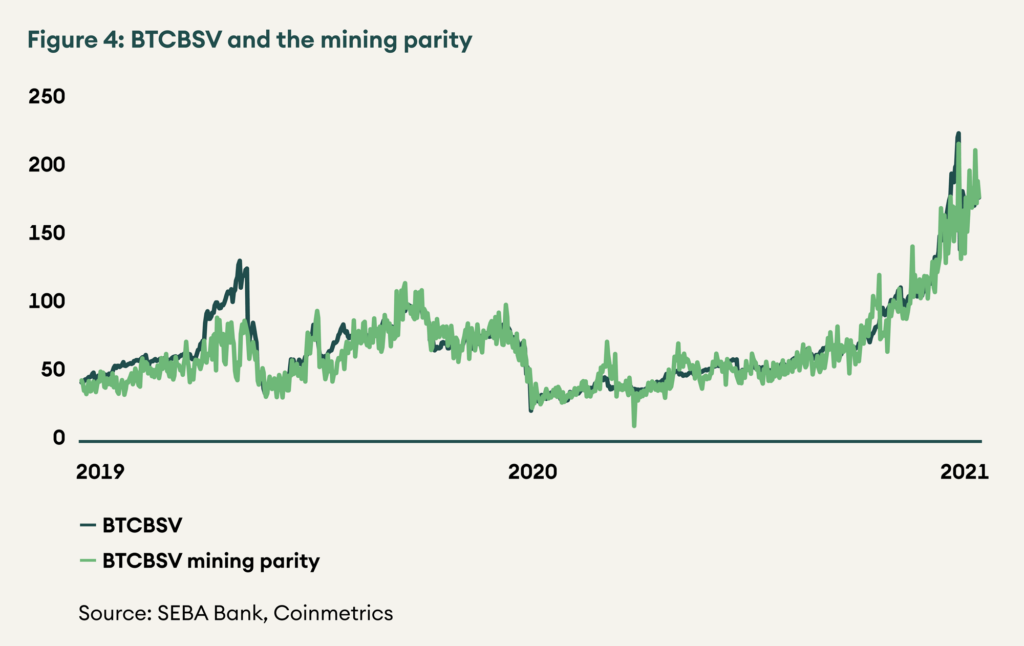

Figures 3 and 4 illustrate the mining parity for BTCBCH and BTCBSV, respectively. In both figures, the fit is excellent, meaning that miners act rationally and that within the cryptoverse, there is no dissonance between coins. Miners behaved rationally after BTC price increased sharply against BSV and BCH.

Mining parity also illustrates the central role played by miners in Proof-of-Work cryptocurrencies and their raison d’être. As they allocate hashing power according to the expected profit, a strong currency attracts miners, reinforces its security, adds more value to it, and attracts more users. This creates a virtuous cycle. On the contrary, a vicious cycle can also be triggered.

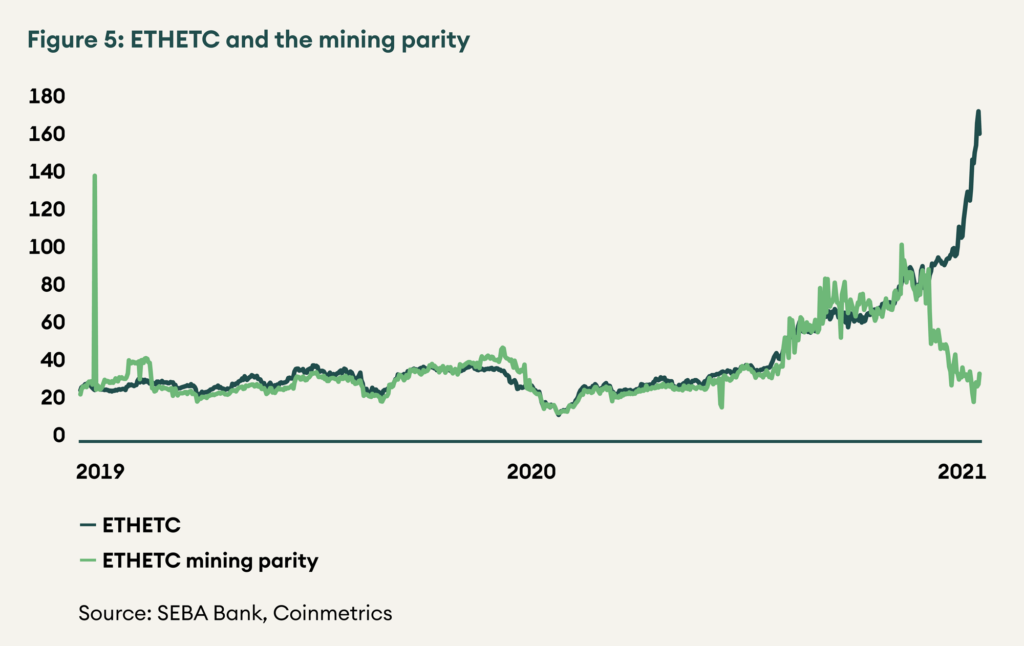

In this regard, the relation between ether (ETH) and ether classic (ETC) is very informative. As these two currencies are close cousins, we can use mining parity condition to compare them. In Figure 5, there are two events worth noting.

First, the three successive 51% attacks on ETC in August 2020 did not fundamentally challenge the mining parity condition. We observe an increase in the mining parity volatility, probably indicating an increasing nervousness in the mining community towards ETC, but the relation still holds.

Second, the disconnect between the two currencies occurred a few days before 1 December, the day Ethereum started its long transition towards Ethereum 2.0. When it became clear that Serenity will be launched, the ETH behaviour changed as it departed from the mining parity condition.

This sudden behaviour change is very informative. It tells us that the type of consensus algorithm used affects the valuation and behaviour of cryptocurrencies. It encourages us to explore the role of consensus on cryptocurrency and to develop a staking parity condition.

Conclusion

In this special edition of the Digital Investor, we have updated our bitcoin fair-value estimate. Due to institutional investors’ growing bitcoin adoption, the network’s size can no longer be measured accurately with the number addresses. A network of 50 million users seems plausible, implying a bitcoin fair value of USD 50,000.

Our mining parity model shows that mining activities have moved in line with prices. We also show that mining activities for ETH and ETC decoupled from their prices when Ethereum 2.0 was launched on 1 December 2020.